A multi-currency liquidity solution is a centralized platform that consolidates a company's cash positions across multiple currencies into a single management system, delivering real-time visibility and efficient cash utilization globally. For business owners and finance professionals managing cross-border payments, understanding currency liquidity is no longer optional. The cost of fragmented cash management compounds fast: idle balances in one currency, expensive overdrafts in another, and treasury teams buried in manual reconciliation. This guide explains what a multi-currency liquidity solution does, how it works, and why the right implementation changes how you manage international cash flows.

What is a multi-currency liquidity solution and how does it work?

A multi-currency liquidity solution operates by pulling all currency balances into one visible, manageable structure. Instead of logging into separate bank portals for euros, dollars, and pounds, your treasury team sees every position in one place. Platforms built for this purpose consolidate global cash, reducing reliance on manual treasury spreadsheets by a significant margin. That reduction matters because manual processes introduce errors, delay decisions, and obscure the true cash picture.

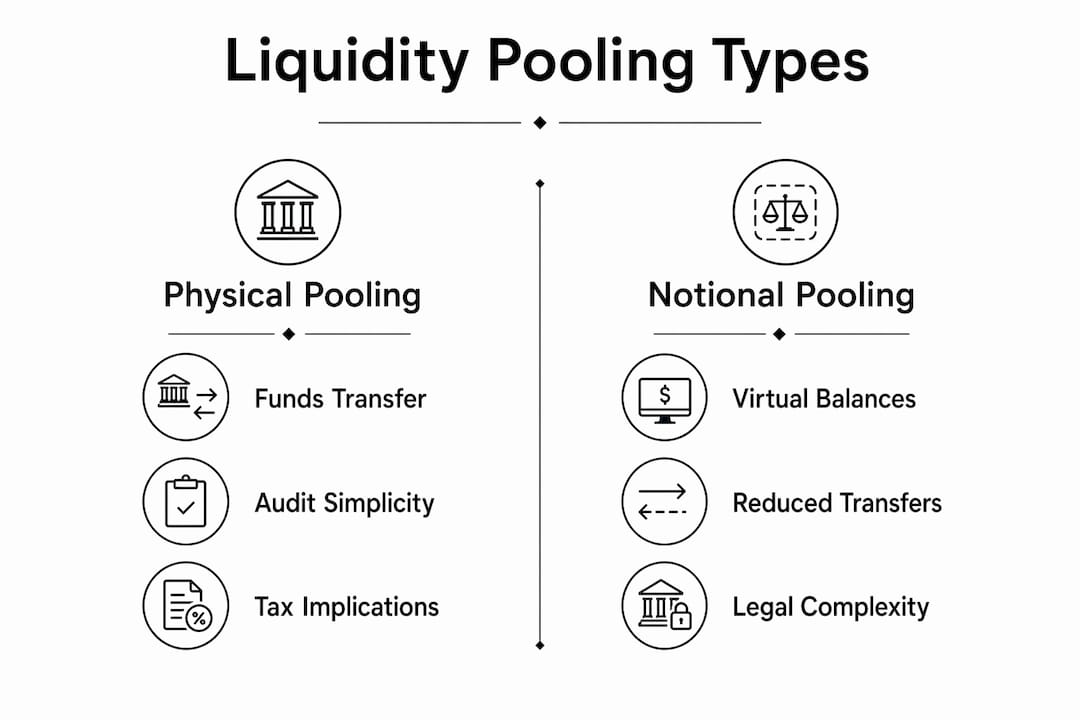

Physical pooling vs. notional pooling

The two primary structures behind these platforms are physical pooling and notional pooling. Physical pooling transfers actual cash into a master account, giving the parent entity direct control over funds. Notional pooling, by contrast, virtually offsets debit and credit balances across accounts for interest calculation purposes without physically moving money. Each structure serves different regulatory environments and corporate treasury preferences.

The practical difference matters for tax and legal reasons. Physical pooling is simpler to audit but triggers intercompany loan rules in some jurisdictions. Notional pooling avoids fund movement but requires banks that support the structure, and not all do. Companies using structured pooling reduce external borrowing costs by cutting the need to draw on credit lines when internal surpluses exist elsewhere.

Automated currency conversions and interest optimization

Beyond pooling, these platforms automate cross-currency cash flows. When a subsidiary in Germany holds excess euros and a subsidiary in Singapore needs dollars, the platform identifies the imbalance and triggers a conversion or intercompany transfer. Multi-currency notional pools offset debit and credit balances in real time, maximizing interest optimization without requiring physical fund transfers. That means you earn more on surpluses and pay less on deficits, without a treasury analyst manually calculating each position.

Pro Tip: Set automated sweep thresholds by currency so the platform moves funds only when a balance crosses a defined floor or ceiling. This prevents unnecessary conversions while keeping each currency account adequately funded.

Key benefits of multi-currency liquidity solutions for global businesses

The financial case for adopting a multi-currency liquidity platform is direct. By managing income and expenses directly in multiple currencies, companies avoid unnecessary foreign exchange conversions and the fees attached to each one. A business billing clients in euros and paying suppliers in yen does not need to convert everything to dollars first. Keeping funds in their earned currency eliminates a conversion layer and its associated cost.

The operational benefits extend well beyond fee savings:

- Reduced external borrowing. When internal surpluses offset deficits across subsidiaries, you borrow less from banks. The interest savings compound across a full fiscal year.

- Faster supplier payments. Paying suppliers in their local currency, without routing through a correspondent bank, cuts settlement time and removes intermediary fees.

- Improved cash forecasting. Real-time position data replaces end-of-day batch reports, giving treasury teams accurate numbers for forecasting models.

- Early warning on liquidity gaps. Liquidity management systems provide a first alert to crunches weeks before a payment failure or supply disruption occurs. That lead time lets you act before a problem becomes a crisis.

- Operational continuity. Platforms that support payments in the currency earned smooth supplier payments and payroll cycles, reducing the friction that comes from currency mismatches.

The strategic benefit goes beyond cost. Financial advisors note that the real value of liquidity solutions is risk mitigation through visibility, not just cost savings. A business that can see its full cash picture across 12 currencies makes better decisions than one piecing together data from six different bank portals.

For import/export companies specifically, a multi-currency account paired with a liquidity management layer removes the double cost of converting purchase currency and sale currency separately.

Integration and technology considerations

The technology layer determines whether a multi-currency liquidity solution delivers its full value or becomes another data silo. Integration failure occurs when platforms lack automated API or SWIFT connections to your ERP or Treasury Management System. Without that connection, finance teams re-enter data manually, which defeats the purpose of real-time visibility.

Direct API integration means your ERP, such as SAP or Oracle, pushes transaction data to the liquidity platform automatically. SWIFT messaging serves the same function for bank-to-bank communication. When selecting a platform, verify that it supports both channels. A platform that requires CSV uploads or manual data entry will not give you the real-time cash position data that makes these solutions worth adopting.

Automation also tightens internal controls. Automated solutions require real-time fund movement approvals, which reduces the risk of unauthorized transactions. That approval layer is a compliance benefit, not just an operational one. Regulators and auditors look favorably on documented, automated approval chains over manual sign-off processes.

Pro Tip: Before signing with any platform, request a technical integration spec sheet. Confirm it lists your ERP version and your bank's SWIFT BIC as supported. A platform that requires custom development to connect to your existing systems will cost more and take longer than the vendor's sales team suggests.

Selecting technology with cross-border payment infrastructure built in reduces implementation time and avoids the need to build custom middleware. Fintech experts note that these tools are not a set-and-forget solution. They require active governance and advanced approval controls to function as intended.

Practical applications in cross-border payment management

Multi-currency liquidity platforms solve specific, recurring problems in international business operations. The following use cases represent the most common scenarios where these platforms generate measurable value.

-

Supplier payments in local currencies. A manufacturing company sourcing components from suppliers in Vietnam, Mexico, and Germany can hold Vietnamese dong, Mexican pesos, and euros in separate sub-accounts. Payments go out in each supplier's local currency without an intermediate conversion to dollars. This removes one conversion fee per transaction and reduces settlement delays caused by correspondent banking chains.

-

International payroll management. A consulting firm with employees in the UK, Canada, and Australia can fund payroll in pounds, Canadian dollars, and Australian dollars from a single platform. The treasury team sets funding rules by currency and the platform executes transfers on payroll dates. Real-time monitoring identifies currency shortages before payroll runs, preventing failed payments.

-

Intercompany fund transfers. A parent company with subsidiaries in five countries can move surplus cash from a subsidiary with excess liquidity to one facing a short-term deficit. The platform handles the FX conversion and transfer in one step, replacing a process that previously required multiple bank instructions and days of settlement time. Digital agencies managing multi-currency client payments use the same mechanism to fund project accounts in client currencies without converting every receipt.

-

Notional pooling for internal cash offsetting. A holding company with subsidiaries across Europe can use a notional pool to offset a euro deficit in France against a euro surplus in the Netherlands. No funds move, but the interest calculation treats the combined position as a net balance. This reduces the interest cost on the French deficit without triggering an intercompany loan.

Key Takeaways

A multi-currency liquidity solution reduces borrowing costs, eliminates unnecessary FX conversions, and gives treasury teams real-time visibility across all currency positions.

| Point | Details |

|---|---|

| Core definition | A centralized platform consolidates all currency balances for real-time visibility and cash control. |

| Pooling structures | Physical pooling moves funds; notional pooling offsets balances virtually for interest optimization. |

| Integration is critical | Direct API or SWIFT connections to your ERP prevent manual data entry and preserve real-time accuracy. |

| Risk mitigation value | Early liquidity alerts flag cash shortages weeks before payment failures occur. |

| Practical cost savings | Paying suppliers and employees in local currencies removes unnecessary FX conversion fees per transaction. |

Why treasury teams underestimate the governance requirement

Most finance professionals I speak with focus on the cost savings when they first evaluate these platforms. That framing is understandable. The fee reduction from eliminating unnecessary FX conversions is visible and easy to quantify. What gets underestimated is the governance work required to make the platform function correctly over time.

A multi-currency liquidity solution is not a passive tool. It requires someone to own the approval workflows, review the automated sweep rules quarterly, and update currency thresholds when business volumes shift. I have seen companies implement these platforms and then leave the configuration unchanged for two years, by which point the sweep thresholds no longer reflect actual cash flow patterns and the platform is moving money inefficiently.

The automation layer also changes the risk profile of treasury operations. When fund movements happen automatically, the consequences of a misconfigured rule are larger than a single manual error. That is why the approval controls matter as much as the automation itself. A well-governed platform with clear approval chains and regular rule reviews delivers the full benefit. A poorly governed one creates a new category of operational risk.

My advice: assign a named treasury owner for the platform configuration, schedule quarterly rule reviews, and treat the governance documentation as seriously as the implementation project. The technology is the easy part.

— Ahmed

How Sigmaplatinum supports multi-currency payment management

Sigmaplatinum is built for international businesses that need efficient, compliant payment workflows across multiple currencies. The platform gives companies access to multi-currency business accounts through regulated partners, with rigorous KYB checks built into onboarding.

Digital agencies, consulting firms, and import/export companies use Sigmaplatinum to manage FX workflows and corporate payment tools without the complexity of traditional banking. The no-code model means your team gets access to the payment infrastructure it needs without a lengthy technical implementation. For businesses ready to move beyond fragmented banking relationships, Sigmaplatinum provides the payment account foundation that makes currency liquidity management practical.

FAQ

What is a multi-currency liquidity solution in simple terms?

A multi-currency liquidity solution is a platform that consolidates a company's cash across multiple currencies into one system, providing real-time visibility and automated fund management. It replaces the need for separate bank accounts and manual reporting in each currency.

What is the difference between physical and notional pooling?

Physical pooling transfers actual funds into a master account, while notional pooling offsets balances virtually for interest calculation without moving money. The right choice depends on your regulatory environment and banking relationships.

How do these solutions reduce foreign exchange costs?

By holding funds in the currency they were earned and paying expenses in the recipient's local currency, businesses avoid converting money unnecessarily. Each avoided conversion removes a transaction fee and eliminates exchange rate exposure on that amount.

What integration does a multi-currency liquidity platform require?

The platform needs direct API or SWIFT connections to your ERP or Treasury Management System to deliver real-time data. Without automated integration, finance teams re-enter data manually, which removes the real-time visibility benefit.

Are multi-currency liquidity solutions suitable for mid-sized businesses?

Mid-sized businesses with suppliers, clients, or employees in multiple countries benefit from these platforms, particularly for reducing FX fees and improving cash forecasting. The key requirement is sufficient transaction volume across currencies to justify the implementation and governance investment.