Cross-border payment infrastructure access is the ability to connect your business to international payment systems that enable multi-currency transfers, foreign exchange settlement, and compliant cross-border transactions. For international businesses, this access determines how fast you get paid, how much you lose to fees, and whether your payments clear at all. The 2026 ISO 20022 migration deadline set by SWIFT, the rise of network-of-networks models like Nexus Global Payments, and API-based interoperability projects like Project Aperta have fundamentally changed what efficient access looks like. This guide breaks down the infrastructure types, compliance requirements, and practical steps you need to operate globally without disruption.

What are the main types of cross-border payment infrastructures?

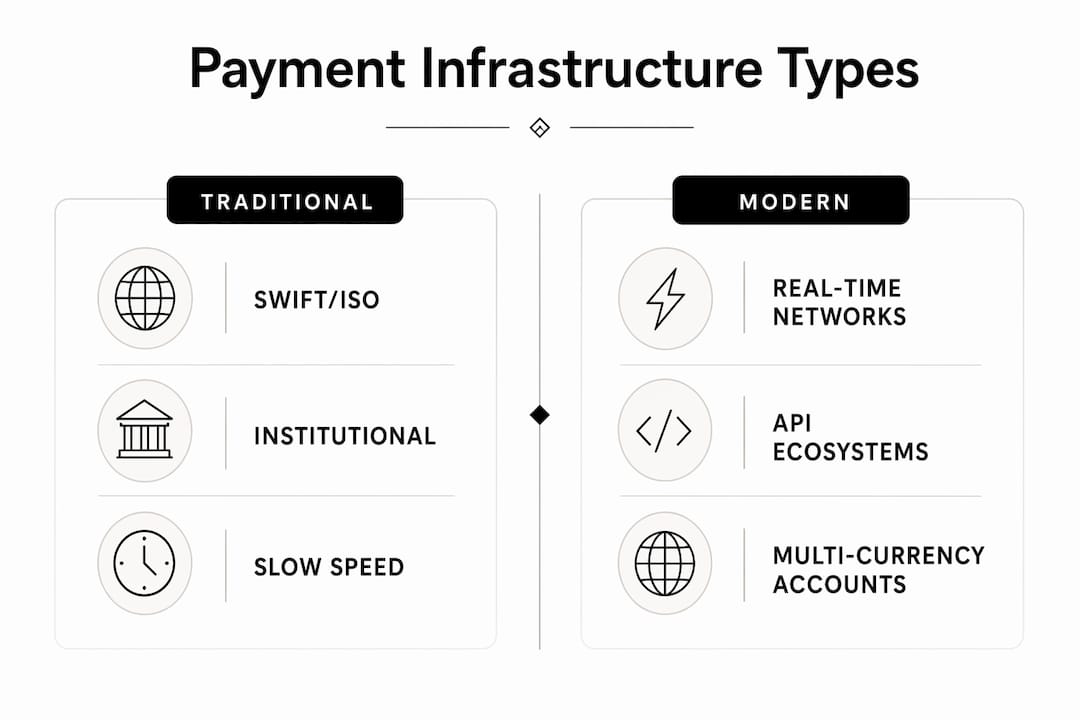

Cross-border payment infrastructure falls into four distinct categories, each with different cost structures, speed profiles, and compliance requirements. Understanding the differences is the first step toward choosing the right global payment solution for your business.

SWIFT and ISO 20022 messaging form the backbone of institutional cross-border transfers. SWIFT connects over 11,000 financial institutions and has been migrating to ISO 20022 structured messaging to replace legacy MT formats. ISO 20022 structured messaging reduces friction in cross-border payments by enabling richer data for straight-through processing and improved compliance. The practical benefit is fewer manual interventions, lower reconciliation costs, and better fraud detection across correspondent banking chains.

Real-time payment networks represent the fastest-growing category. Project Nexus targets a 2027 go-live connecting domestic instant payment systems across six countries to 1.7 billion people. This matters because Nexus uses a hub-and-spoke architecture, meaning each country connects once to gain access to all member networks. That single-connection model replaces the traditional bilateral approach where each payment corridor requires a separate technical and legal agreement.

API-based open finance ecosystems are the newest access layer. Project Aperta demonstrates cross-border interoperability via a neutral API layer connecting open finance ecosystems across multiple jurisdictions. This approach lets businesses plug into multiple payment rails through one technical interface rather than maintaining separate integrations per market.

Multi-currency account services sit closest to the end user. Clear Junction expanded its SWIFT service in 2026 to provide two-way SWIFT connectivity across 11 currencies with named client accounts and integrated FX. This consolidates international funding and domestic payouts into a single infrastructure, which is exactly what treasury teams managing multiple payment corridors need.

| Infrastructure type | Speed | Best for | Key limitation |

|---|---|---|---|

| SWIFT / ISO 20022 | 1-2 business days | Institutional and high-value transfers | Compliance overhead, correspondent fees |

| Nexus instant payment network | Under 60 seconds | Consumer and SME cross-border payments | 2027 go-live, limited initial coverage |

| API open finance (Project Aperta) | Variable | Multi-jurisdiction open banking access | Governance and legal complexity |

| Multi-currency accounts (e.g., Clear Junction) | Same day to next day | Treasury management, FX consolidation | Eligibility and KYB requirements |

How to prepare your business for ISO 20022 migration and 2026 standards

The November 2026 deadline is not a soft target. SWIFT will reject cross-border ISO 20022 payment messages with fully unstructured postal addresses from that date onward. Businesses that have not updated their address data capture systems will face rejected payments with no fallback option. The SR2026 enforcement carries no contingencies.

Here is the migration sequence every international business should follow:

-

Audit your current address data. Map every system that captures creditor and debtor postal addresses, including ERP platforms, CRM tools, and payment initiation software. Identify which fields currently store addresses as free-text strings rather than structured components (street, city, postal code, country).

-

Update data capture at origination. Businesses must capture postal address data in structured or hybrid format at the point of payment creation. Fixing data downstream at the bank level is not a reliable workaround once SWIFT enforcement begins.

-

Engage your banking partners now. ISO 20022 enforcement deadlines like SR2026 make early partner engagement essential to prevent payment failures. Your bank or payment service provider needs to confirm their systems accept and pass structured address fields end-to-end.

-

Test with live payment flows. Run structured-format test transactions through your full payment chain before the deadline. Identify truncation points where intermediaries strip or reformat address data.

-

Update client onboarding forms. Any form that collects counterparty details needs to enforce structured address input. This is an operational change, not just a technical one.

The operational upside of this migration goes beyond compliance. ISO 20022 readiness drives reconciliation and governance improvements that reduce ongoing maintenance costs. Structured data means your finance team spends less time manually matching payments to invoices.

Pro Tip: Start client address data collection updates at least six months before November 2026. Late engagement with banking partners is the single most common cause of last-minute payment disruptions during major messaging standard transitions.

What are practical ways to gain access to multi-currency and global payment corridors?

Accessing multi-currency payment infrastructure requires more than opening a foreign currency account. The architecture behind your account determines which corridors you can reach, how fast settlements clear, and what FX rates you actually pay.

Named client accounts with integrated FX represent the most operationally efficient model for businesses managing multiple currencies. Unlike pooled accounts where your funds sit alongside other clients' money, named accounts give you a dedicated IBAN per currency, which simplifies reconciliation and satisfies counterparty due diligence requirements in markets like the EU and UK. Importers and exporters benefit most from this structure, as explained in detail for multi-currency account needs.

Single API platforms that combine cross-border and domestic rails reduce the integration overhead significantly. Instead of connecting to SEPA, Faster Payments, ACH, and SWIFT separately, a single API endpoint routes payments to the appropriate rail based on destination and currency. This is the same architectural principle behind Nexus, where each country connects once to gain access to all member networks rather than building bilateral links per corridor.

Before applying for multi-currency account access, review these eligibility factors:

- Business registration and jurisdiction. Most providers require incorporation in a recognized jurisdiction with verifiable company registration documents.

- KYB documentation. Know Your Business checks typically require beneficial ownership disclosure, audited financials or bank statements, and proof of business activity.

- Transaction volume and purpose. Providers assess whether your expected payment volumes and corridors match your stated business model.

- Compliance history. Prior sanctions hits, adverse media, or regulatory actions will disqualify most applicants at the onboarding stage.

The 2026 eligibility requirements for multi-currency accounts have tightened alongside ISO 20022 enforcement, so preparation before applying saves significant time.

Pro Tip: Consolidating your payment flows under one provider that handles both SWIFT connectivity and domestic rail access gives your treasury team a single reconciliation point. Fragmented providers mean fragmented data, which multiplies your month-end workload.

How to integrate and manage cross-border payment infrastructure effectively

Integration is where most businesses underestimate the complexity. The technical connection is often the simpler part. Data quality, compliance architecture, and counterparty onboarding create the real friction.

Address data quality is the most immediate operational risk in 2026. Businesses with unstructured address data risk payment rejections downstream even when their own internal systems pass validation. The problem occurs at intermediary banks that apply SWIFT's structured address rules to forwarded messages. Your payment can originate correctly and still fail mid-chain.

Maintaining structured data end-to-end is equally critical for reconciliation. Preserving structured remittance fields across all intermediaries maximizes ISO 20022 benefits. The biggest losses come from truncation at correspondent banks that strip purpose codes or remittance references when converting between message formats. Select providers that explicitly commit to end-to-end structured data preservation.

Real-time compliance checks add another layer of operational complexity. Cross-border instant payments under 60 seconds require real-time sanctions screening embedded in infrastructure gateways. This means your payment initiation system must be able to receive and act on compliance holds within seconds, not minutes. Build that response logic into your payment operations workflow before going live on instant payment rails.

For businesses evaluating infrastructure providers, follow this selection sequence:

- Confirm the provider's ISO 20022 compliance status and SR2026 readiness documentation.

- Verify their sanctions screening methodology and response time commitments.

- Assess whether they use a hub model or bilateral connections for your target corridors.

- Review their data flow architecture to confirm structured data is preserved across the full payment chain.

- Request a sandbox environment to test structured address formats and remittance data before going live.

Cross-border interoperability is as much a governance and legal challenge as a technical one. Successful integration requires addressing both in parallel, not sequentially.

What are common troubleshooting issues and how to avoid payment failures?

Payment failures in cross-border transactions cluster around a predictable set of causes. Knowing them in advance lets you build preventive controls rather than reactive fixes.

The most urgent risk in 2026 is unstructured postal address usage. After November 2026, any payment message routed through SWIFT with a free-text address block will be rejected. This affects not just your outbound payments but also inbound payments from counterparties who have not completed their own migration.

Other common failure points include:

- Message truncation at correspondent banks. When intermediaries convert ISO 20022 messages to legacy formats, structured fields get dropped. This breaks automated reconciliation and can trigger compliance flags.

- Bilateral linkage delays. Payment corridors built on bilateral agreements between two institutions require multi-party approvals for exceptions. A single compliance hold can delay settlement by days.

- Mismatched beneficiary data. Name and account number mismatches between your records and the receiving bank's records trigger manual review queues, adding hours or days to settlement.

- Incomplete KYB on counterparties. Sending payments to counterparties who have not completed onboarding at the receiving institution causes holds that neither party can resolve quickly.

Compliance readiness warning: Businesses that have not completed ISO 20022 structured address migration by November 2026 face automatic payment rejection with no manual override available. This is not a soft deadline. Test your full payment chain with structured data formats before Q3 2026 to identify and fix failure points while you still have time.

Periodic payment flow testing is the most underused risk management tool in cross-border operations. Run end-to-end test transactions through every active corridor at least quarterly. Identify which intermediaries are stripping data fields and address those relationships before they cause live payment failures.

Key takeaways

Efficient cross-border payment infrastructure access in 2026 requires structured ISO 20022 data compliance, a hub-based network model, and multi-currency account architecture that consolidates FX and settlement into one provider.

| Point | Details |

|---|---|

| ISO 20022 deadline is firm | SWIFT rejects unstructured address messages from November 2026 with no fallback option. |

| Hub models outperform bilateral links | Nexus-style single-connection architecture reduces corridor integration time and cost significantly. |

| Named accounts improve reconciliation | Dedicated IBANs per currency simplify counterparty due diligence and month-end matching. |

| Data quality drives automation | Preserving structured remittance fields end-to-end maximizes straight-through processing and reduces manual work. |

| Early provider engagement is non-negotiable | Selecting ISO 20022-ready partners before Q3 2026 prevents last-minute payment disruptions. |

Why the ISO 20022 transition is bigger than most businesses realize

Most of the conversation around ISO 20022 focuses on the technical messaging change. That framing undersells what is actually happening. This transition is forcing businesses to rethink how they capture, store, and transmit financial data at every point in the payment lifecycle.

I have seen businesses treat this as a bank problem. They assume their payment service provider will handle the migration and nothing will change on their end. That assumption is wrong, and it will cost them rejected payments in Q4 2026. The structured address requirement starts at origination, which means your ERP, your invoicing software, and your client onboarding forms all need to change.

The network-of-networks model is the more exciting long-term shift. Bilateral payment corridors have always been the bottleneck in global payment solutions. Every new market required a new agreement, a new technical integration, and a new compliance review. The Nexus model breaks that constraint. A single connection gives you access to every member network. That is a structural change in how international payment systems scale, and businesses that position themselves on compliant, hub-connected infrastructure now will have a meaningful speed advantage when new corridors go live.

My honest recommendation: treat your payments infrastructure roadmap as a compliance and FX strategy document, not just a technology project. The businesses that integrate those three workstreams will spend less, settle faster, and onboard new markets without starting from scratch each time.

— Ahmed

How Sigmaplatinum supports your global payment operations

Sigmaplatinum is built specifically for international businesses that need structured, compliant access to cross-border payment infrastructure without the complexity of managing multiple banking relationships.

Through Sigmaplatinum's business payment account platform, international companies access multi-currency accounts, SWIFT connectivity, and integrated FX workflows through a single, compliance-focused onboarding process. The platform's KYB-first model means you connect to regulated infrastructure that meets 2026 ISO 20022 standards from day one. Digital agencies, import/export companies, and consulting firms use Sigmaplatinum to consolidate payment flows, reduce FX costs, and manage cross-border transactions without building internal treasury infrastructure. If your business is preparing for the November 2026 SWIFT deadline or expanding into new payment corridors, Sigmaplatinum's no-code access model gets you operational faster than traditional banking routes.

FAQ

What is cross-border payment infrastructure access?

Cross-border payment infrastructure access is the ability to connect to international payment systems, including SWIFT, real-time payment networks, and API-based open finance platforms, to send and receive multi-currency transfers across borders. Businesses access this infrastructure directly through banks, payment service providers, or specialized fintech platforms like Sigmaplatinum.

What changes with ISO 20022 in November 2026?

SWIFT will reject cross-border payment messages that contain fully unstructured postal addresses from November 2026 onward. Businesses must update their payment origination systems to capture creditor and debtor addresses in structured or hybrid format before that deadline.

How does the Nexus hub model differ from bilateral payment links?

The Nexus model requires each country to connect once to the network to gain access to all member payment systems, while bilateral models require a separate connection per corridor. This single-connection architecture reduces integration complexity and speeds up the addition of new payment corridors.

What documents do businesses need for multi-currency account access?

Most providers require company registration documents, beneficial ownership disclosure, proof of business activity, and recent financial statements. Compliance history and expected transaction volumes are also assessed during the KYB onboarding process.

How do I prevent payment failures caused by data truncation?

Select payment infrastructure providers that explicitly preserve structured ISO 20022 remittance and address fields across all intermediaries. Test your full payment chain with structured data formats before going live, and review your data integration workflows to identify where field stripping occurs.