A multi-currency account is a single business account that holds, sends, and receives funds in multiple foreign currencies without triggering a conversion at every transaction. For importers paying suppliers in euros, yuan, or dollars while operating in a different home currency, this structure directly cuts the cost and complexity of every cross-border payment. The question of why importers need multi-currency accounts comes down to three compounding advantages: lower FX fees, faster settlements, and sharper financial control. This article breaks down each advantage with specific examples and the tools that deliver them.

Why importers need multi-currency accounts to cut costs

Every time a traditional bank converts currency on your behalf, it takes a spread. That spread is rarely disclosed as a flat fee. It is buried in the exchange rate itself, and it compounds across every supplier invoice you pay. Digital banking platforms reduce conversion fees to as low as 0.2% for high-volume traders, compared to the 2% to 4% spreads common at retail banking desks. For an importer moving $2 million annually through supplier payments, that difference is $36,000 to $76,000 per year.

The savings go beyond the conversion rate itself. Routing through fewer intermediaries improves settlement predictability and reduces the correspondent bank fees that accumulate when a payment hops through three or four institutions before reaching a supplier. Multi-currency accounts with consolidated infrastructure bypass much of that chain by holding the destination currency already. A payment from a EUR balance to a European supplier travels a shorter path and arrives faster.

Paying suppliers in their local currency also removes the conversion surcharges that supplier banks impose when they receive a foreign-currency wire. Those charges are often deducted from the payment itself, leaving your supplier short and creating reconciliation disputes. Holding EUR, GBP, and USD in a single account eliminates that friction entirely.

- Avoid double-conversion costs when your bank converts to USD and the supplier's bank converts back to EUR

- Reduce correspondent bank fees by using platforms with direct settlement rails

- Eliminate supplier-side deduction disputes by paying in the invoice currency

- Consolidate multiple supplier currencies into one account rather than maintaining separate banking relationships

Pro Tip: Look for platforms that support SEPA payments alongside SWIFT. SEPA-enabled accounts allow instant euro transfers across Europe, which is a practical advantage if you source from multiple European suppliers and need same-day settlement.

How multi-currency accounts improve financial visibility

Financial visibility is where multi-currency accounts deliver value that most importers underestimate. The problem with traditional cross-border payments is not just cost. It is the reporting chaos that follows. Each conversion creates a separate transaction record, a separate FX rate, and a separate reconciliation entry. Finance teams spend hours matching payments to invoices when the amounts differ because of mid-transaction conversions.

Standardized IBAN structures improve payment formatting and traceability, reducing duplicated workflows and delays. When every incoming and outgoing payment carries a consistent account identifier, your finance team gains a clean audit trail without manual correction work. This matters particularly at month-end, when reconciling supplier payments against purchase orders and goods receipts.

The table below compares financial visibility under traditional conversion-based banking versus a multi-currency account structure.

| Visibility factor | Traditional conversion banking | Multi-currency account |

|---|---|---|

| Transaction traceability | Multiple records per payment due to conversion steps | Single record per payment with currency preserved |

| Reconciliation effort | High. Manual matching of converted amounts to invoices | Low. Invoice currency matches payment currency |

| FX rate transparency | Rate embedded in conversion, often undisclosed | Rate applied only at chosen conversion point |

| Audit trail quality | Fragmented across intermediary banks | Consolidated under one account with IBAN reference |

| Month-end close speed | Slow due to variance corrections | Faster with automated reconciliation integration |

Integration with accounting platforms amplifies these gains. Systems like NetSuite, when configured for FX revaluation, automatically track realized and unrealized FX gains and losses at period end. This is a requirement under IAS 21/IFRS 21 for any business reporting in a functional currency different from its transaction currencies. Without proper configuration, those variances accumulate as errors that distort your profit and loss statement.

Pro Tip: When connecting a multi-currency account to your ERP, designate separate ledger accounts for FX revaluation and realized variance from the start. Retrofitting this setup after six months of transactions is significantly more labor-intensive than building it correctly at implementation.

How do multi-currency accounts help importers manage currency risk?

Currency risk for importers is asymmetric. When you quote a landed cost to a domestic buyer, you lock in a price. If the supplier's currency strengthens before you pay the invoice, your margin shrinks. Multi-currency accounts address this by giving you the ability to time FX conversions strategically, holding foreign currency balances when rates are favorable and converting when they are not.

This is not speculation. It is cash flow matching. If you receive payment from a domestic customer in USD and your Chinese supplier invoices in USD, holding a USD balance means you never need to convert at all. The payment flows directly from your USD receivable to your USD payable. Your margin is protected by structure, not by luck.

Multi-currency accounts also work alongside formal hedging instruments. Forward contracts, for example, lock in an exchange rate for a future payment date. But forwards require you to actually deliver the currency at settlement. Holding the target currency in a multi-currency account means you can fulfill that obligation without a last-minute spot conversion at whatever rate the market offers that day.

- Match invoice currencies to supplier payment currencies to eliminate conversion exposure entirely

- Hold EUR or GBP balances accumulated from European sales to fund European supplier payments

- Use forward contracts to lock rates on large future purchases, then settle from your held currency balance

- Monitor real-time currency balances to identify conversion windows when rates move in your favor

Predictable landed cost calculation depends on knowing your payment cost before the goods arrive. When you hold the supplier's currency, that cost is fixed the moment you fund the balance. Importers who rely on spot conversions at payment date are essentially repricing every purchase order twice: once when they quote it and once when they pay it.

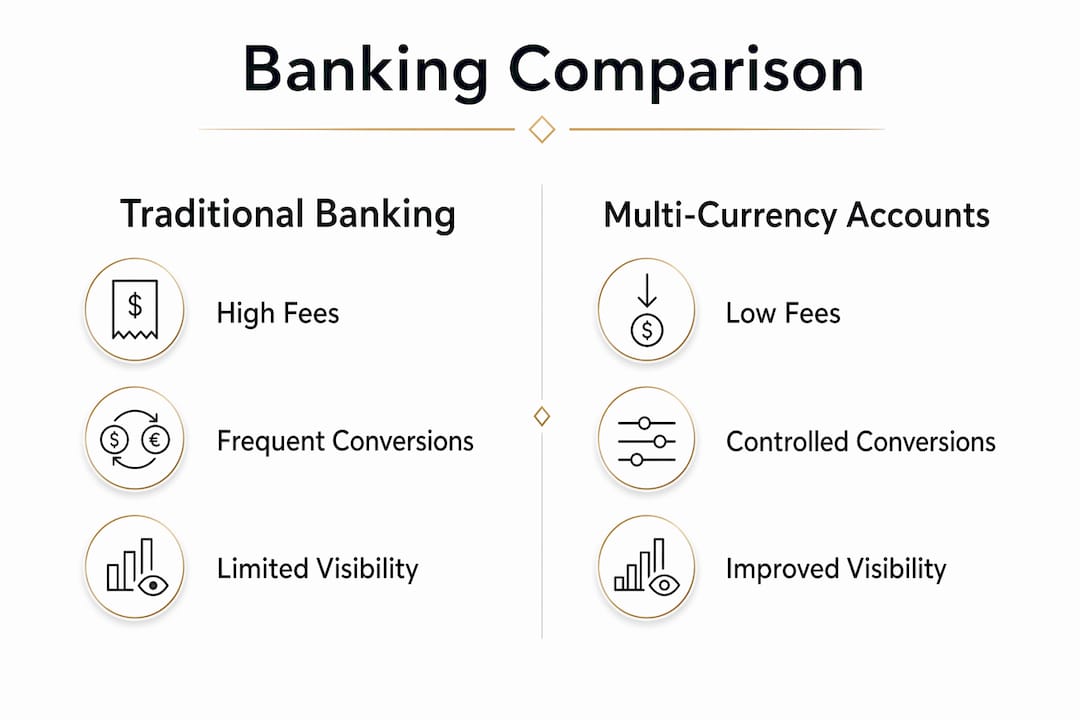

Multi-currency accounts vs. traditional conversion methods

The practical difference between multi-currency accounts and traditional conversion-based banking becomes clearest when you map a single supplier payment end to end.

Under traditional banking, an importer in the UK paying a German supplier in EUR initiates a GBP wire. The UK bank converts GBP to EUR at its retail rate, charges a wire fee, sends the payment through one or two correspondent banks, each of which may deduct a handling fee, and the German supplier receives an amount that may differ from the invoice total. The importer's accounting team then reconciles the GBP amount paid against the EUR invoice, calculates the FX variance, and posts a correction entry.

Under a multi-currency account structure, the same importer holds a EUR balance funded at a time of their choosing. They initiate a EUR payment directly to the German supplier. No conversion occurs at payment time. The supplier receives the exact invoice amount. The accounting system records a single EUR transaction against the EUR invoice. Reconciliation takes seconds.

| Factor | Traditional conversion banking | Multi-currency account |

|---|---|---|

| Conversion frequency | Every payment | Only when funding the balance |

| Typical FX cost | 2% to 4% spread | As low as 0.2% for high-volume users |

| Intermediary banks | 2 to 4 per payment | Often 1 or none |

| Settlement speed | 2 to 5 business days | Same day to next day for major currencies |

| Accounting complexity | High. Multiple entries per payment | Low. Single currency transaction |

| Supplier payment accuracy | Subject to deductions | Exact invoice amount delivered |

The trade-off worth acknowledging is that multi-currency accounts require active balance management. You need to fund each currency balance at the right time, which means monitoring exchange rates and maintaining adequate liquidity across currencies. For importers with predictable payment schedules, this is straightforward. For those with irregular purchase volumes, it requires more attention.

Key takeaways

Multi-currency accounts give importers direct control over when and how currency conversions happen, which is the single most effective way to reduce FX costs and protect margins in international trade.

| Point | Details |

|---|---|

| Cost reduction | Conversion fees drop to as low as 0.2% versus 2% to 4% at traditional banks. |

| Supplier payment accuracy | Paying in invoice currency eliminates deductions and reconciliation disputes. |

| Financial visibility | IBAN-based accounts create clean audit trails and faster month-end close. |

| Currency risk management | Holding foreign balances lets you time conversions and match cash flows precisely. |

| Accounting integration | ERP systems like NetSuite require proper FX revaluation setup to report accurately. |

What I've learned about multi-currency accounts after years in international payments

Most importers I speak with come to multi-currency accounts because of a specific pain point: a supplier dispute over a short payment, a surprise FX loss at year-end, or a month-end close that took three weeks instead of one. They adopt the account to solve that one problem and then realize the structural advantage runs much deeper.

The mistake I see most often is treating a multi-currency account as a payment tool rather than a financial control layer. Businesses that get the most value from these accounts are the ones that integrate them directly into their ERP, configure proper FX revaluation accounts from day one, and build a currency funding schedule that aligns with their supplier payment calendar. That combination turns a payment account into a genuine risk management asset.

The other underrated factor is provider infrastructure. Not all multi-currency accounts are equal. Some platforms support SEPA and SWIFT but lack direct settlement rails for Asian currencies. Others offer broad currency coverage but no accounting integration. The right choice depends on where your suppliers are located and what your finance team needs to close the books efficiently.

My honest recommendation: before you select a provider, map your top five supplier currencies, your average payment frequency, and your accounting system. Then test whether the platform handles all three without manual workarounds. If it does, you have found a foundation worth building on.

— Ahmed

How Sigmaplatinum supports importers with multi-currency payment access

Sigmaplatinum connects eligible importers with business payment account solutions that support GBP, EUR, and USD workflows through regulated partners. If your business needs to hold multiple currencies, pay international suppliers in their local currency, and reconcile transactions without the overhead of traditional banking, Sigmaplatinum can help you access the right infrastructure. The platform is designed for companies that operate across borders and need payment accounts that match the complexity of their supply chains. All applications go through KYB review and partner approval to confirm eligibility. Reach out to Sigmaplatinum to find out which account solutions fit your import operation.

FAQ

What is a multi-currency account for importers?

A multi-currency account lets an importer hold, send, and receive funds in multiple foreign currencies within a single account. It removes the need for a currency conversion at every supplier payment, reducing fees and simplifying reconciliation.

How much can importers save with a multi-currency account?

Digital banking platforms reduce FX conversion fees to as low as 0.2% for high-volume traders, compared to the 2% to 4% spreads typical at retail banks. On $2 million in annual supplier payments, that gap represents tens of thousands of dollars in savings.

Do multi-currency accounts help with currency risk?

Yes. Holding foreign currency balances lets importers time conversions strategically and match supplier payment currencies to receivable currencies, which eliminates conversion exposure on matched flows entirely.

What accounting setup do multi-currency accounts require?

ERP systems like NetSuite must be configured for FX revaluation and realized variance tracking to report accurately under IAS 21/IFRS 21 standards. Without this setup, FX gains and losses accumulate as unrecorded errors in your financial statements.

Can multi-currency accounts support European supplier payments?

Yes. Accounts with SEPA payment capability enable instant euro transfers across Europe, which is particularly useful for importers managing multiple European suppliers who require same-day or next-day settlement.