A multi-currency account for consultants is a single business payment account that lets you receive, hold, convert, and send funds in multiple currencies without opening separate bank accounts in each country. The industry standard term for this tool is a "foreign currency business account," though "multi-currency account" is the phrase most consultants search for and most providers use. Platforms like Airwallex, Wise, and Sigmaplatinum offer these accounts specifically for international business workflows. If you invoice clients in euros, pay contractors in British pounds, and operate from the United States, this type of account replaces a tangle of wire transfers with one dashboard.

What is a multi-currency account for consultants?

A multi-currency account gives consultants one platform to manage every currency they touch. Instead of routing a euro payment through a U.S. dollar account and absorbing two conversion fees, you receive the euros directly into a euro sub-account. You hold the balance, convert when the rate suits you, and send funds to vendors or your local bank on your own schedule.

The core functions are straightforward: local receiving details in currencies like USD, EUR, and GBP; the ability to hold balances in each currency; FX conversion at interbank-adjacent rates; and outbound payments to international recipients. Providers like Airwallex and Wise publish their fee structures openly, which is a meaningful contrast to traditional bank wire pricing.

Traditional bank wires for international transactions typically carry fees of 3% to 5%, including hidden markups on the exchange rate itself. That margin comes directly out of your invoice value every time a client pays you from abroad.

What are the main advantages of multi-currency accounts for consultants?

The financial case for multi-currency accounts is direct. The most immediate benefit is cost reduction.

- Lower transfer fees. Standard bank wire costs of 3–5% disappear when you receive funds into a local currency sub-account. Your client pays a domestic transfer. You receive the full amount.

- Faster payments. Multi-currency accounts process cross-border payments in 1–2 days versus the 3–5 days typical of traditional bank wires. Faster settlement means better cash flow, which matters when you are managing project expenses against delayed client payments.

- FX conversion control. You hold multiple currency balances and convert only when rates are favorable. Forced conversion at the moment of receipt is one of the most expensive habits in international consulting finance.

- Simplified reconciliation. One account statement covers all currencies. That reduces the administrative work of matching invoices to payments across multiple bank accounts.

- Vendor and contractor payouts. Paying a contractor in their local currency removes the fee burden from their end and makes you easier to work with.

Pro Tip: Set a rate alert in your multi-currency platform for your most common currency pair. Convert in batches when the rate crosses your target rather than converting each invoice individually.

The speed advantage deserves emphasis. A 1–2 day settlement versus 3–5 days is not just a convenience. On a $50,000 consulting project with a 30-day payment term, receiving funds two days earlier meaningfully changes your working capital position.

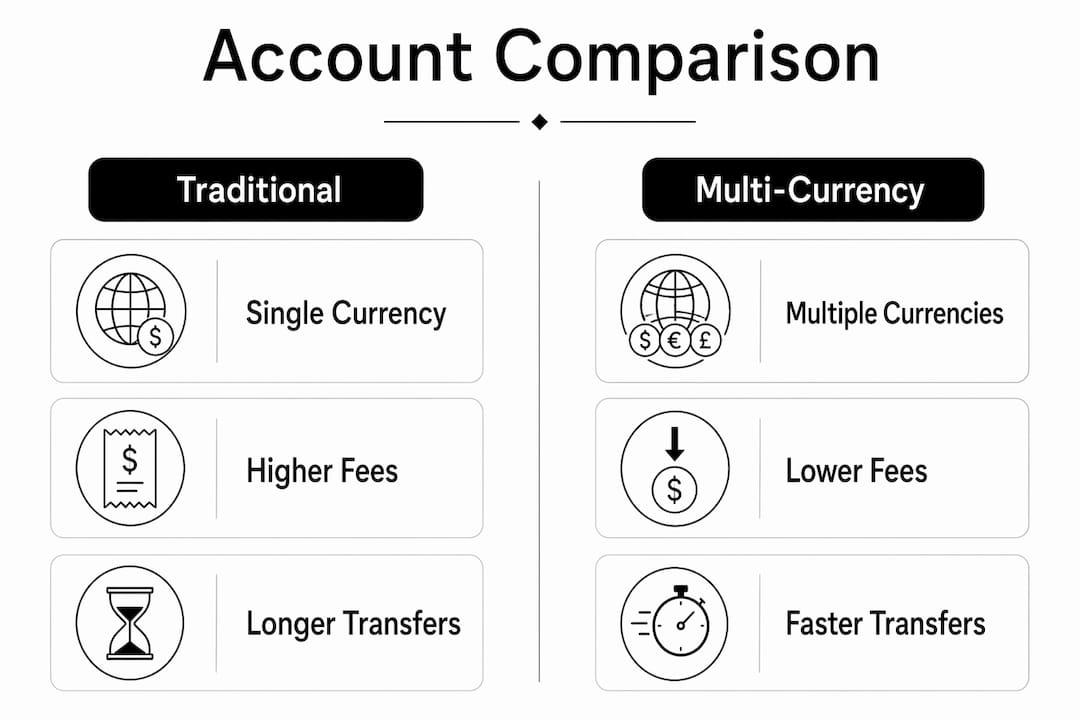

How do multi-currency accounts compare to traditional business bank accounts?

The clearest way to understand the difference is to look at what each account type does well.

| Feature | Traditional bank account | Multi-currency account |

|---|---|---|

| Hold multiple currencies | No (single currency) | Yes (sub-accounts per currency) |

| Local receiving details abroad | No | Yes (USD, EUR, GBP, and more) |

| FX conversion control | No (bank converts on receipt) | Yes (convert when rates suit you) |

| International payout speed | 3–5 business days | 1–2 business days |

| Integration with payroll/tax systems | Strong | Limited |

| Regulatory familiarity for local tax | High | Low |

Multi-currency accounts work best as an operational upgrade alongside your primary local bank account, not as a replacement. Most consultants keep their domestic bank for payroll, tax payments, and local expenses. The multi-currency account handles FX workflows, international client receipts, and vendor payouts.

A practical example: a management consultant based in Chicago invoices a client in Frankfurt in euros. The Frankfurt client pays a local German bank transfer to the consultant's euro receiving details. The consultant holds the euros, converts to USD when the rate is strong, and transfers to their Chase or Bank of America account for payroll. No international wire fees. No forced conversion at the moment of receipt.

Pro Tip: Never close your domestic bank account when you open a multi-currency account. Local banks remain the right tool for tax payments, payroll, and any transaction that requires a recognized domestic routing number.

For consultants exploring the setup process for multi-currency accounts, the onboarding typically requires business registration documents, proof of address, and a KYB (Know Your Business) review.

What challenges should consultants know before opening a multi-currency account?

Multi-currency accounts solve real problems, but they introduce operational complexity that consultants often underestimate before signing up.

The biggest hidden cost is the reconciliation gap. Multi-currency accounts frequently lack native integration with legacy accounting software. QuickBooks Desktop, for example, does not natively sync with most fintech multi-currency platforms. That means manual CSV uploads, third-party middleware like Zapier, or custom data entry to keep your books accurate.

Compatibility issues between multi-currency accounts and existing financial systems are common. Consultants who do not plan for this before onboarding often spend more time on manual reconciliation than they save on fees.

Other challenges worth knowing:

- Exchange rate risk. Holding a large euro balance while the euro weakens against the dollar costs you money. Conversion control is a benefit, but it requires active attention.

- Currency restrictions. Not every provider supports every currency. If you work with clients in emerging markets, check the supported currency list before committing to a platform.

- Regulatory limitations. Multi-currency accounts are not licensed banks in most jurisdictions. They cannot hold your funds with the same deposit protection as an FDIC-insured account.

- Provider-specific limits. Some platforms cap transaction sizes or require additional verification for large transfers.

Pro Tip: Before onboarding, map every accounting software touchpoint in your current workflow. Identify which steps will require manual intervention and build that time into your monthly close process.

The reconciliation challenge is solvable, but it requires planning. Consultants who treat multi-currency accounts as a plug-and-play replacement for their bank often hit friction within the first quarter.

How to use multi-currency accounts to get paid faster and pay vendors efficiently

The practical workflow for consultants breaks into three areas: getting paid, managing balances, and paying out.

Getting paid like a local

- Request local receiving details from your provider. Most platforms issue you a local account number and routing equivalent for USD, EUR, GBP, and other major currencies. Local receiving details let your international clients pay you as a domestic transfer, removing the international wire process entirely.

- Update your invoice template. Add the relevant local account details for each client's currency. A German client sees your EUR details. A UK client sees your GBP details. This removes friction from their payment process and speeds up receipt.

- Confirm payment terms in the invoice currency. Invoicing in the client's currency removes ambiguity and reduces disputes about exchange rate differences.

Managing currency balances

- Hold balances strategically. Do not convert every receipt immediately. Monitor the rate for your primary currency pair and convert in batches when the rate is favorable. FX conversion control is one of the clearest financial advantages of this account type.

- Set conversion thresholds. Decide in advance at what rate you will convert. This removes emotion from the decision and creates a repeatable process.

Paying vendors and contractors

- Use batch payments for contractor payouts. Batch payment features let you pay multiple contractors in their local currencies in a single transaction run. This saves time and gives contractors cleaner payment records.

- Pay in the recipient's currency. Paying a contractor in their local currency removes the fee burden from their side and avoids the exchange rate markup they would otherwise absorb.

Pro Tip: Use your multi-currency account dashboard as your international finance command center. Review balances weekly, not just when a payment is due. Proactive balance management prevents forced conversions at bad rates.

For consultants managing cross-border payment workflows across multiple client relationships, the dashboard visibility alone justifies the switch from traditional banking for international transactions.

Key takeaways

A multi-currency account for consultants is the most direct way to cut international transfer costs, speed up client payments, and pay vendors in their local currency without opening foreign bank accounts.

| Point | Details |

|---|---|

| Core function | Receive, hold, convert, and send multiple currencies from one account. |

| Cost savings | Avoid the 3–5% fees and hidden markups on traditional international bank wires. |

| Payment speed | Settle cross-border payments in 1–2 days instead of 3–5 days. |

| Use alongside local banks | Keep your domestic account for payroll and taxes; use multi-currency for FX workflows. |

| Plan for reconciliation | Legacy accounting software often requires manual workarounds to sync with multi-currency platforms. |

What I've learned after years of watching consultants get this wrong

Most consultants who open a multi-currency account do it reactively. A client in Germany pays late, the wire fee stings, and they sign up for Wise or Airwallex the same week. That reactive approach works, but it misses the bigger opportunity.

The consultants who get the most value treat their multi-currency account as financial infrastructure, not a one-off fix. They map their entire payment flow before they open the account. They know which currencies they receive, which currencies they pay out, and where their accounting software will need manual input. They set conversion thresholds before the first receipt hits the account.

The reconciliation gap is the part that surprises people most. I have seen consultants save hundreds of dollars in wire fees and then spend equivalent hours manually reconciling transactions because they did not plan for the QuickBooks integration gap. The net gain disappears fast if you do not solve the data flow problem upfront.

My honest recommendation: treat the account selection process like a software evaluation. Test the accounting integration before you commit. Check the supported currency list against your actual client base. Read the fee schedule for conversions, not just for receiving. The right platform for a consultant billing in EUR and GBP is not necessarily the right platform for one billing in SGD and AED.

Multi-currency accounts are genuinely useful tools. They are not magic. The consultants who benefit most are the ones who understand exactly what problem they are solving before they open the account.

— Ahmed

How Sigmaplatinum supports consultants with international payments

Consultants managing international client payments need a payment account built for cross-border workflows, not a retail bank account with international wire access bolted on.

Sigmaplatinum is a B2B fintech platform that gives consulting firms access to multi-currency business payment accounts through regulated partners. The platform supports FX workflows, international payouts, and currency management through a compliance-focused onboarding process that includes KYB checks. Setup is designed to be fast, with no-code access to core payment features. Consulting firms that invoice international clients, pay global contractors, or manage multi-currency cash flow use Sigmaplatinum to handle those workflows without the friction of traditional banking. If you are ready to move beyond wire transfers and manual currency conversion, Sigmaplatinum is worth evaluating.

FAQ

What is a multi-currency account for consultants?

A multi-currency account for consultants is a single business payment account that holds, receives, converts, and sends funds in multiple currencies. It replaces the need for separate foreign bank accounts and reduces international transfer fees significantly.

How do multi-currency accounts save consultants money?

Traditional international bank wires carry fees of 3–5%, including hidden exchange rate markups. Multi-currency accounts let consultants receive funds via local bank transfers in the client's currency, avoiding those fees entirely.

Can a multi-currency account replace my regular business bank account?

No. Multi-currency accounts work best alongside a primary domestic bank account. Keep your local bank for payroll, tax payments, and domestic expenses. Use the multi-currency account for international receipts, FX conversions, and vendor payouts.

What accounting software works with multi-currency accounts?

Many modern platforms integrate with cloud-based tools like QuickBooks Online and Xero. Legacy software like QuickBooks Desktop often requires manual CSV uploads or third-party middleware. Plan your data flow before onboarding to avoid reconciliation problems.

How fast do multi-currency accounts process international payments?

Multi-currency accounts typically process cross-border payments in 1–2 business days. Traditional bank wires take 3–5 business days. That speed difference directly improves cash flow for consultants with active international billing cycles.