A multi-currency business account is a single account that holds balances in multiple currencies simultaneously, letting UK companies receive, hold, and send foreign currency without converting every transaction. For any business trading internationally, whether you import goods from Asia, invoice European clients in euros, or pay US contractors in dollars, a proper UK company multi-currency account setup removes the friction that standard GBP accounts create. Providers like Starling, WorldFirst, and HSBC each approach this differently, and the right choice depends on your currency needs, transaction volume, and compliance profile.

What are the requirements for UK company multi-currency account setup?

Eligibility for a foreign currency business account in the UK is more specific than most owners expect. Most providers, including Starling, require a company limited by shares or an LLP registered at Companies House, with directors and persons with significant control (PSCs) who are UK residents. Sole traders and overseas-registered entities typically face more limited options or outright rejection.

Documentation is where most applications stall. AML regulations require a defined set of documents before any provider can onboard you. According to UK AML requirements, you will need:

- Certificate of incorporation from Companies House

- Beneficial ownership register or confirmation of PSC details

- Government-issued photo ID for all directors and PSCs

- Proof of address for each director and PSC (utility bill or bank statement, dated within three months)

- Business bank statements or annual accounts showing financial history

- A clear description of your business activities and expected transaction patterns

- Source of funds documentation explaining where incoming payments originate

The FCA mandates risk-based customer due diligence, which means higher-risk businesses, such as those operating in multiple high-risk jurisdictions or handling large cash flows, will face enhanced due diligence (EDD). EDD requires more detailed documentation and can extend approval timelines significantly.

Pro Tip: Link your source of funds documentation directly to your expected transfer patterns. Providers who can see a logical connection between your business model and your anticipated payment flows approve applications faster and with fewer follow-up requests.

Review the multi-currency account eligibility checklist before you apply. Having every document ready before you start the application cuts approval time by days.

How do you compare UK multi-currency account providers?

Choosing the right provider for multi-currency accounts for UK businesses comes down to five factors: currency coverage, conversion fees, local payment identifiers, onboarding speed, and daily workflow features.

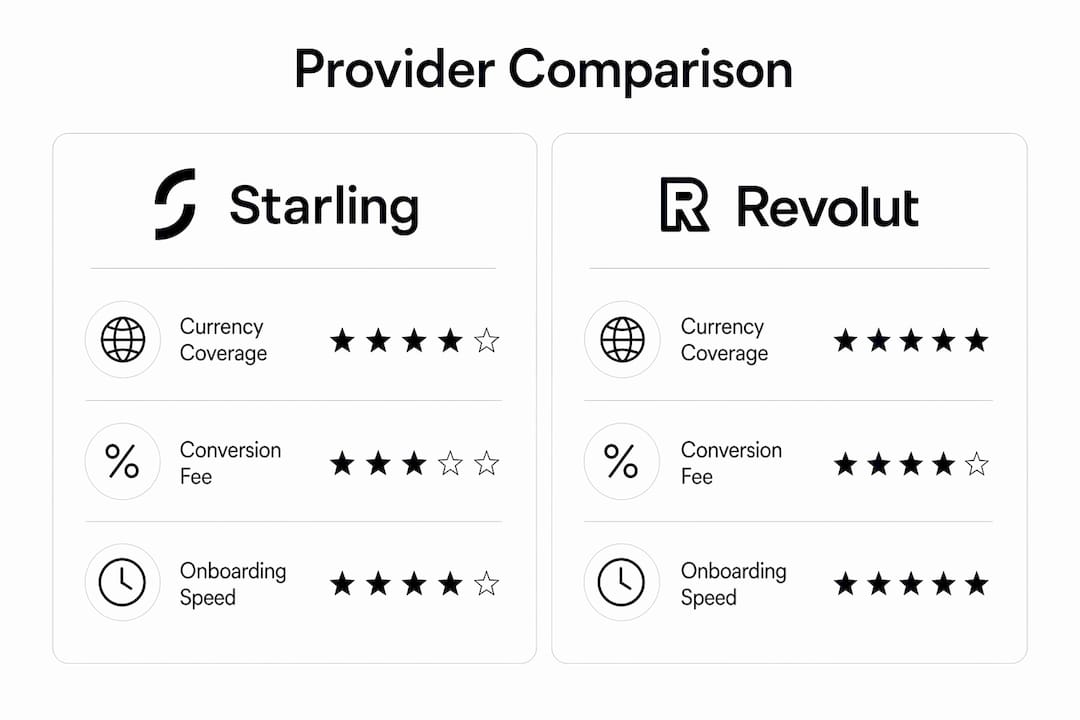

Starling offers 24/7 currency transfers between GBP and other currencies, including weekends, with a 0.4% conversion fee at the real exchange rate. Accounts include local identifiers such as IBANs for European payments and US account numbers for dollar transactions. WorldFirst supports over 100 currencies, making it the stronger choice for businesses trading across multiple emerging markets. HSBC brings the weight of a traditional bank with established correspondent banking relationships, though its onboarding process is slower and more document-intensive.

| Provider | Currency Coverage | Conversion Fee | Local Identifiers | Onboarding Speed |

|---|---|---|---|---|

| Starling | Major currencies | 0.4% | IBAN, US account number | Fast (days) |

| WorldFirst | 100+ currencies | Varies by currency | IBAN, local rails | Moderate |

| HSBC | Major currencies | Varies | IBAN, SWIFT | Slow (weeks) |

| Revolut Business | 25+ currencies | 0.4%–1% | IBAN, local | Fast (days) |

Exchange rate transparency matters more than the headline fee. A provider advertising "no fees" but applying a 2% spread on every conversion costs you more than one charging 0.4% on the real rate. Always request a sample conversion quote before committing.

Pro Tip: When comparing providers, check which payment rails each account supports. A provider with IBAN and US account numbers covers most international corridors, but if you pay suppliers in Southeast Asia or Latin America, you need local rail access too.

For a detailed feature comparison of leading UK multi-currency accounts, the provider alternatives guide breaks down exchange rate transparency and approval timeframes side by side.

Step-by-step: how to open a multi-currency account for your UK business

The process of setting up a foreign currency account in the UK follows a consistent sequence across most providers. Knowing what comes next prevents delays.

- Prepare your document pack. Gather your certificate of incorporation, PSC register, ID and address proofs for all directors, six months of business bank statements, and a one-page business activity summary. Write the summary in plain language: what you sell, who you sell to, and how payments flow.

- Complete the online application. Most providers, including Starling and Revolut Business, run fully digital applications. You will upload documents, answer questions about expected monthly transaction volumes, and confirm your business structure.

- Pass KYC and CDD screening. The provider runs identity checks, sanctions screening, and a review of your business activity description. This step can take 24 hours for straightforward applications or several weeks for businesses flagged for EDD.

- Respond to follow-up requests promptly. Providers frequently request additional information during review. A 48-hour response window is standard. Delays on your side pause the clock entirely.

- Activate your currency wallets. Once approved, you enable individual currency balances within the account. Starling, for example, lets you activate GBP, EUR, and USD wallets independently.

- Connect your payment workflows. Link your account to your invoicing software, payroll system, or treasury platform. Set conversion preferences: on-demand conversion gives you control over timing, while automatic conversion removes manual steps.

Controlling when currency conversions occur is one of the most underused tools in multi-currency treasury management. Converting on-demand rather than automatically lets you act when exchange rates favor your position, which compounds into meaningful savings over a full financial year.

Multi-currency account setup in the UK does not end at approval. The FCA expects periodic compliance reviews and ongoing transaction monitoring. Treat your account as a living compliance relationship, not a one-time application.

How do UK payment systems affect your multi-currency workflows?

Understanding UK payment rails is not optional when you manage international transactions. Each rail has different speed, limits, and settlement timing, and routing the wrong payment type through the wrong rail costs you time and sometimes money.

The three core UK payment schemes work as follows:

- CHAPS clears same-day on UK working days with no maximum transaction limit. Use it for large treasury transfers, property transactions, or any high-value supplier payment where same-day settlement is non-negotiable.

- Faster Payments clears within seconds, operates 24/7, and carries a £1 million limit per transaction. It is the right rail for urgent supplier payments, payroll runs, and any transfer where speed matters more than size.

- Bacs takes three working days to settle and is best suited for recurring, predictable payments like regular payroll or direct debits where timing is planned in advance.

Choosing the right rail per transaction type is a direct efficiency gain. Routing a £500,000 treasury move through Faster Payments when CHAPS is available introduces unnecessary risk. Routing a £200 supplier payment through CHAPS when Faster Payments would settle it in seconds wastes processing overhead.

| Payment Type | Best Rail | Settlement Time | Limit |

|---|---|---|---|

| Large treasury transfer | CHAPS | Same day | No limit |

| Urgent supplier payment | Faster Payments | Seconds | £1,000,000 |

| Regular payroll | Bacs | 3 working days | No limit |

| International wire | SWIFT/CHAPS | 1–3 days | Varies |

Sanctions screening adds another layer to payment timing. Since 2022, the FCA has identified sanctions compliance weaknesses across regulated firms, primarily from operational failures in screening and alert management. A payment to a counterparty that triggers a sanctions alert will be held until the provider resolves the flag. Build contingency time into any payment workflow involving counterparties in higher-risk jurisdictions. For businesses with complex cross-border flows, the cross-border payment infrastructure guide explains how to map payment types to the right rails for consistent cash flow timing.

Key takeaways

A successful UK company multi-currency account setup requires the right provider, complete documentation, and a payment workflow matched to the correct UK payment rail.

| Point | Details |

|---|---|

| Eligibility is specific | Most providers require a UK-registered Ltd or LLP with UK-resident directors and PSCs. |

| Documentation drives approval speed | Linking source of funds directly to expected transfer patterns reduces verification delays. |

| Provider choice affects FX cost | Compare real-rate conversion fees and local identifiers, not just headline pricing. |

| Payment rail selection matters | Match CHAPS, Faster Payments, or Bacs to each transaction type for reliable cash flow timing. |

| Compliance is ongoing | FCA expects periodic reviews and transaction monitoring well beyond initial onboarding. |

What most guides get wrong about multi-currency accounts

Most articles on this topic treat compliance as a box to check during onboarding. That framing causes real operational problems six months later.

I have seen businesses get approved, activate their currency wallets, and then face transaction holds because their actual payment patterns diverged from what they described in their application. The FCA's expectation of documented periodic reviews is not bureaucratic noise. It reflects the reality that your business changes, and your provider needs to understand those changes before they show up as anomalies in your transaction data.

The second mistake I see consistently is treating FX conversion as an afterthought. Businesses set up automatic conversion because it is easier, then wonder why their margins erode. Controlling conversion timing, even manually reviewing rates once a week, is a treasury discipline that pays for itself. Starling's on-demand conversion model exists precisely because this matters.

Sanctions screening delays are the most disruptive surprise for businesses new to multi-currency accounts. The FCA has flagged sanctions control weaknesses across the industry since 2022. If you pay suppliers in regions with elevated sanctions risk, build a 48-hour buffer into your payment schedule and maintain alternative payment instructions for critical counterparties. That single preparation step prevents the cash flow crises I have watched derail otherwise well-run operations.

— Ahmed

How Sigmaplatinum supports UK companies with multi-currency payments

UK businesses that need efficient international payment workflows without the friction of traditional banking have a direct path through Sigmaplatinum.

Sigmaplatinum is a B2B fintech platform built specifically for international companies that need reliable multi-currency payment account access. The platform connects businesses to regulated partners through a compliance-focused onboarding process that includes rigorous KYB checks and partner evaluations. Digital agencies, consulting firms, and import/export companies use Sigmaplatinum to manage FX workflows and cross-border transactions without the complexity of traditional bank relationships. If you are ready to move past generic banking options and access a business payment account built for international operations, Sigmaplatinum is the place to start.

FAQ

What documents do i need to open a multi-currency business account in the UK?

You need your certificate of incorporation, PSC register, photo ID and proof of address for all directors, business bank statements, and a clear description of your business activities and expected payment flows. Source of funds documentation is required by AML regulations for all UK business account applications.

How long does UK multi-currency account onboarding take?

Standard applications with complete documentation typically take 1–5 business days with providers like Starling or Revolut Business. Applications requiring enhanced due diligence can take several weeks depending on the complexity of your business structure and jurisdictions involved.

What is the difference between CHAPS and faster payments for multi-currency accounts?

CHAPS settles same-day with no transaction limit and is best for large transfers. Faster Payments settles within seconds, operates 24/7, and has a £1 million limit, making it the right choice for urgent payments where speed matters more than transaction size.

Can a non-uk resident director open a UK multi-currency business account?

Most mainstream providers require UK-resident directors and PSCs for standard eligibility. Businesses with non-resident directors typically face additional scrutiny, longer review timelines, or may need to work with specialist providers that accommodate international ownership structures.

Why do multi-currency transactions sometimes get delayed after approval?

Sanctions screening is the most common cause of post-approval transaction holds. The FCA has identified operational weaknesses in sanctions alert management across regulated firms since 2022. Payments to counterparties in higher-risk jurisdictions can trigger holds until the provider resolves the screening alert.