A foreign currency business account is a specialized bank account that lets your company hold, send, and receive funds in a single foreign currency without converting every transaction back to your domestic currency. The industry also refers to these as FX business accounts or foreign currency deposit accounts. For any business paying overseas suppliers, billing international clients, or managing cross-border payroll, this account type directly reduces conversion costs and exchange rate exposure. Common currencies held include USD, EUR, GBP, CAD, SGD, and JPY, depending on where your trading partners are located.

What is a foreign currency business account and how does it work?

A foreign currency account lets businesses hold, send, and receive funds in one foreign currency, avoiding the cost and friction of constant conversion. The core mechanic is simple: funds arrive in the foreign currency and stay there until you decide to convert or spend them. You control the timing of any conversion, which is the primary operational advantage over a standard domestic business account.

Most providers deliver access through online platforms, mobile apps, or web dashboards. Westpac, CommBank, and fintech platforms like Sigmaplatinum all offer online account management with real-time balance visibility. That means you can monitor your USD or EUR balance from the same interface you use for domestic payments.

Here is how the account functions in two common scenarios:

- Paying a foreign supplier: You hold EUR in your account and pay a German manufacturer directly in EUR. No conversion occurs, and you avoid the spread your bank would otherwise charge.

- Receiving client payments: A US-based client pays your invoice in USD. The funds land in your USD account and sit there until you choose to convert or reinvest them in another USD transaction.

Pro Tip: Time your conversions around favorable rate windows rather than converting automatically on receipt. Holding balances strategically is one of the most underused cost controls in international business banking.

Transaction volume matters here. Businesses with high monthly FX flows benefit most because every avoided conversion saves a percentage of the transaction value. For lower-volume businesses, the account still provides predictability when quoting prices in foreign currency.

What are the benefits and challenges of these accounts?

The primary foreign currency account benefit is cost reduction. Every time you convert currency, your bank or payment provider takes a spread, often 1%–3% of the transaction. Holding funds in the target currency eliminates that cost for transactions within the same currency.

Core benefits include:

- Exchange rate control: You decide when to convert, not your bank. This lets you wait for a favorable rate rather than accepting the spot rate at the moment of payment.

- Cash flow predictability: Holding foreign currency balances means your costs and revenues in that currency are not constantly recalculated in domestic terms.

- Supplier relationships: Paying suppliers in their local currency removes friction and often qualifies you for better pricing since you eliminate their FX risk.

- Reduced fees: Holding funds strategically cuts conversion fees and can reduce wire transfer costs when payments stay within the same currency.

The real challenges are less discussed:

- Depreciation exposure: If the currency you are holding falls in value against your domestic currency, your balance loses purchasing power. This is the flip side of rate control.

- Single-currency limitation: Most foreign currency accounts support one currency per account. A business trading in USD, EUR, and GBP needs three separate accounts, which multiplies admin overhead.

- No cash access: Foreign currency accounts do not support cash deposits or ATM withdrawals. They are designed for electronic business transactions only, not travel or petty cash.

- Minimum balance requirements: Some providers require minimum balances or charge inactivity fees, which ties up working capital.

Pro Tip: Never hold more foreign currency than you expect to deploy within 30–60 days unless you have a specific hedging strategy. Idle balances in a depreciating currency are a silent cost most business owners miss.

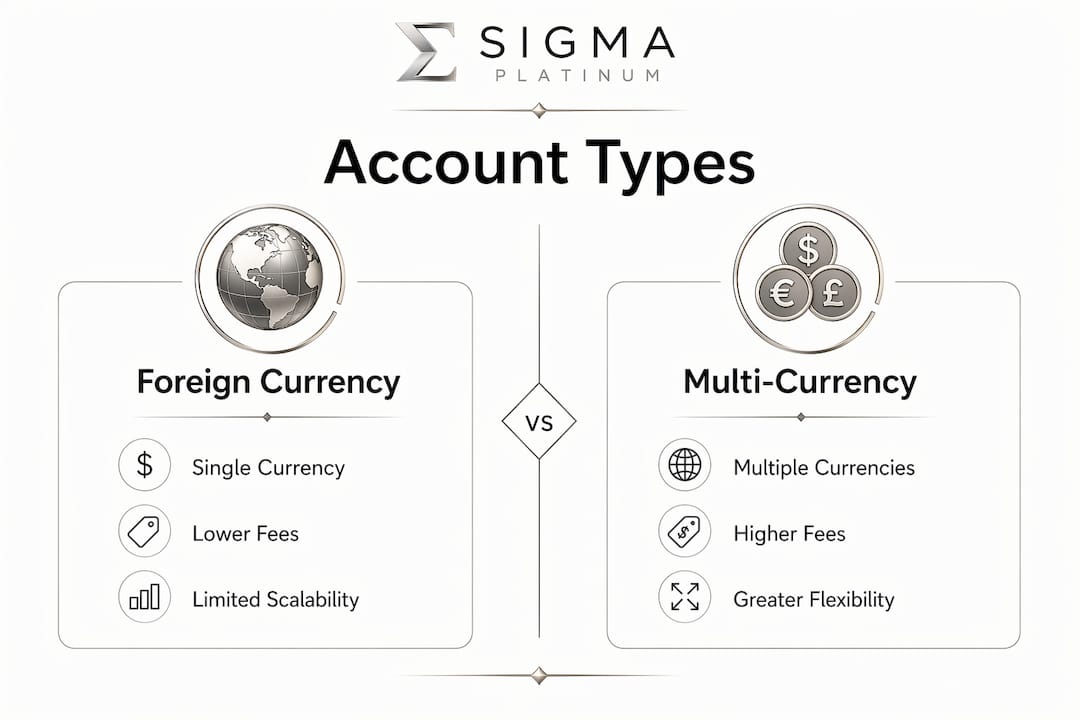

How does a foreign currency account compare to a multi-currency account?

The distinction between these two account types is the most misunderstood concept in foreign currency business banking. A foreign currency account holds one non-domestic currency. A multi-currency account holds multiple currencies within a single account structure, with consolidated visibility and easier conversion between them.

For a business trading in two or three currencies, the difference is manageable. For a business dealing with five or more currencies, the gap in operational efficiency is significant.

| Feature | Foreign Currency Account | Multi-Currency Account |

|---|---|---|

| Currencies supported | One per account | Multiple in one account |

| Conversion control | Manual, timed by business | Built-in, often automated |

| Admin overhead | High for multiple currencies | Low, consolidated dashboard |

| Best for | Focused single-currency trade | Diverse international dealings |

| Scalability | Limited | High |

| Cash flow visibility | Per-account only | Consolidated across currencies |

Multi-currency accounts are more suitable for businesses dealing with several foreign currencies, while single-currency FX accounts work well for businesses with a focused trading relationship in one market. A consulting firm billing exclusively in USD from a non-US base is a perfect candidate for a single foreign currency account. An import/export company sourcing from Asia, Europe, and North America needs a multi-currency structure.

The scalability argument is decisive for growing businesses. Starting with a foreign currency account is reasonable, but planning your upgrade path to a multi-currency setup before you need it saves a disruptive account migration later.

What are the requirements for opening a foreign currency business account?

Opening a foreign currency business account follows a structured process, and preparation shortens the timeline significantly. Online applications for simple business profiles can take as little as 10 minutes, while complex corporate structures may require branch visits and multi-week compliance reviews.

The standard documentation requirements are:

- Business formation documents: Certificate of incorporation, articles of organization, or equivalent depending on your jurisdiction.

- Tax identification number: An EIN in the United States, an ABN or ACN in Australia, or the equivalent identifier for your country.

- Proof of business address: A utility bill, lease agreement, or official correspondence dated within 90 days.

- Beneficial ownership information: Most providers require identification for any individual owning 25% or more of the business.

- Transaction volume disclosure: Providers ask for estimated monthly transaction volumes and the purpose of foreign currency use to satisfy anti-money laundering requirements.

Eligibility varies by business structure. Sole traders, private companies, partnerships, and self-managed funds are typically eligible. Foreign companies are usually reviewed on a case-by-case basis, which means longer timelines and additional documentation.

Currency availability also affects the application process. Popular currencies like USD, EUR, and GBP are available online at most providers. Less common currencies such as SGD or JPY may require a branch visit or a separate application. Check the eligibility requirements for your target currency before starting the process.

How can businesses get the most from foreign currency accounts?

The businesses that extract the most value from foreign currency accounts treat them as active financial tools, not passive holding accounts. The difference shows up in cost savings and cash flow stability over time.

- Monitor exchange rates actively: Set rate alerts through your banking platform or a tool like XE or OANDA. Converting when the rate moves in your favor by even 0.5% on a $100,000 transaction saves $500 with no additional effort.

- Integrate with invoicing platforms: Using a foreign currency account with invoicing tools improves payment receipt efficiency and reduces FX fees. Platforms like Xero and QuickBooks support multi-currency invoicing that connects directly to FX accounts.

- Avoid excess idle balances: Hold only what you need for near-term payables in that currency. Excess balances sitting in a depreciating currency erode your margins quietly.

- Coordinate with your domestic account: Use your foreign currency account for foreign transactions and your domestic account for local expenses. Mixing the two creates reconciliation problems and unnecessary conversion costs.

- Review your cross-border payment setup annually: Payment infrastructure changes fast. What was the best setup in 2024 may not be optimal in 2026.

The businesses that treat FX account management as a quarterly review item rather than a set-and-forget function consistently outperform on international transaction costs.

Key takeaways

A foreign currency business account reduces conversion costs and exchange rate exposure, but its value depends entirely on how actively you manage it.

| Point | Details |

|---|---|

| Core function | Hold, send, and receive one foreign currency without forced conversion to domestic funds. |

| Primary benefit | Eliminates conversion fees on transactions within the same currency, saving 1%–3% per transaction. |

| Main limitation | One currency per account means multiple accounts for businesses trading in several currencies. |

| Multi-currency upgrade | Businesses dealing with five or more currencies should consider a multi-currency account for consolidated management. |

| Application readiness | Prepare business formation documents, tax ID, proof of address, and transaction volume estimates before applying. |

Why foreign currency accounts are underused as a strategic tool

Most business owners I talk to treat foreign currency accounts as a convenience feature, something you open because your bank offers it and you have a supplier in Germany. That framing misses the real opportunity.

The businesses getting the most out of these accounts use them as a timing instrument. They watch rate movements, hold balances during unfavorable periods, and convert in batches when the rate improves. Over a year, that discipline on a $500,000 annual FX volume can recover tens of thousands of dollars that would otherwise go to bank spreads.

The other thing I see consistently underestimated is the compliance preparation. Businesses that walk into the application process without their documentation organized lose weeks. The providers doing rigorous KYB checks are not being difficult. They are protecting you from being on the same platform as bad actors. That compliance rigor is a feature, not a barrier.

My honest view on the foreign currency versus multi-currency debate: start with a foreign currency account if you have one primary trading currency. But build your account structure with the assumption that you will need multi-currency capability within 18 months. The businesses that plan for that transition early avoid the disruption of migrating supplier payment details and client billing setups mid-growth.

The fintech platforms entering this space in 2025 and 2026 are also worth watching. The gap between traditional bank FX accounts and fintech multi-currency platforms is closing fast on features, and the cost difference is already significant for high-volume businesses.

— Ahmed

Manage international payments with Sigmaplatinum

Sigmaplatinum is built specifically for international businesses that need more than a standard bank account. The platform gives you access to business payment accounts with multi-currency capabilities, FX workflows, and compliance-focused onboarding through regulated partners.

If you are managing payments across multiple currencies or working with overseas suppliers and clients, Sigmaplatinum removes the operational complexity that slows most businesses down. The onboarding process includes rigorous KYB checks, so you get a secure, verified account structure from day one. Digital agencies, consulting firms, and import/export companies use the platform to cut FX costs and consolidate their international payment operations. Explore business payment account access at Sigmaplatinum and see what your international payment setup should look like.

FAQ

What is a foreign currency business account used for?

A foreign currency business account is used to hold, send, and receive funds in a specific foreign currency without converting every transaction to your domestic currency. Businesses use them to pay overseas suppliers, receive international client payments, and reduce conversion fees.

How long does it take to open a foreign currency business account?

Simple business profiles can open accounts online in 10 minutes, while complex corporate structures may require branch visits and multi-week compliance reviews.

What is the difference between a foreign currency account and a multi-currency account?

A foreign currency account holds one non-domestic currency per account. A multi-currency account holds several currencies in one structure with consolidated management, making it better suited for businesses trading across multiple markets.

Can i withdraw cash from a foreign currency business account?

Foreign currency business accounts do not support cash withdrawals or ATM access. They are designed for electronic business transactions only.

What documents do i need to open a foreign currency business account?

You need business formation documents, a tax identification number such as an EIN or ABN, proof of business address, beneficial ownership information, and estimated transaction volume details.