A cross-border payment solution is a financial platform or service that enables businesses to send and receive money across national borders, handling currency conversion, regulatory compliance, and international routing in a single workflow. These solutions replace the fragmented, multi-intermediary process of traditional correspondent banking with purpose-built infrastructure designed for speed, cost control, and transparency. For business owners managing suppliers in Asia, clients in Europe, or contractors across multiple continents, understanding what a cross-border payment solution actually does is the first step toward controlling your international cash flow.

What is a cross-border payment solution and how does it work?

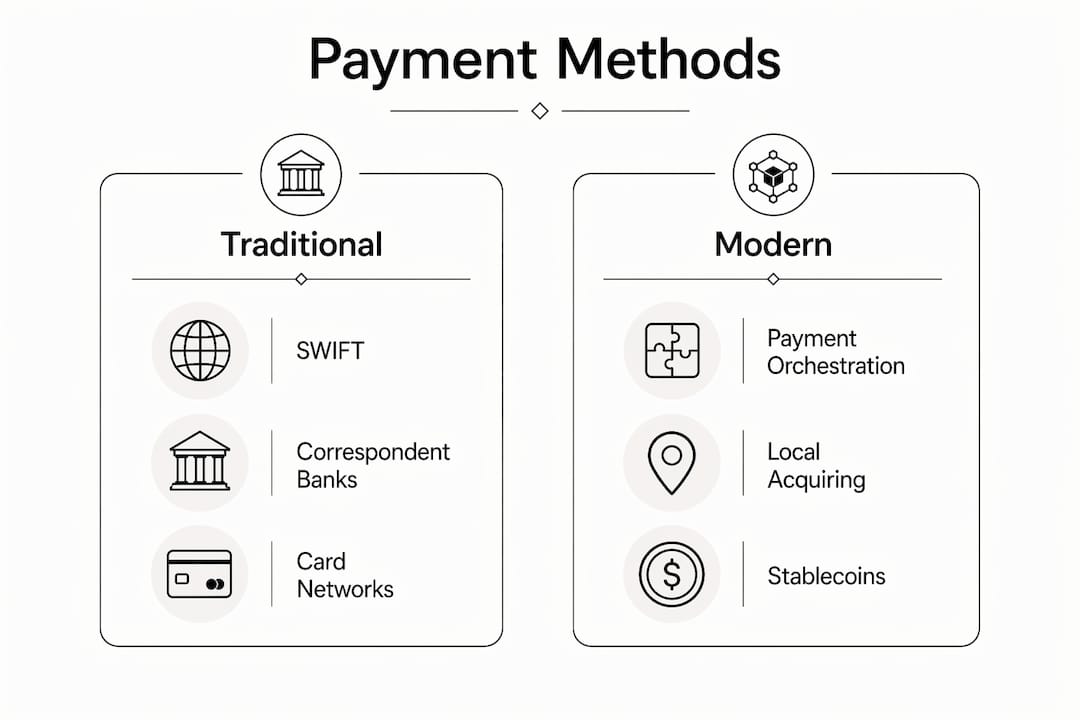

A cross-border payment solution is defined as any system, platform, or account structure that facilitates the transfer of value between a sender in one country and a recipient in another, typically involving currency conversion, international routing, and compliance checks. The industry term for the broader category is international payment infrastructure, which includes everything from SWIFT-based bank transfers to modern payment orchestration layers and stablecoin rails.

Traditional cross-border payments rely on correspondent banking, a network where banks hold accounts with each other (called nostro and vostro accounts) to move funds internationally. This system works, but it creates a well-documented problem: trapped liquidity in nostro accounts means billions in idle capital that banks cannot deploy, and those costs flow directly to business customers as fees and delays. Settlement timelines in legacy SWIFT corridors average one to three business days, with potential delays when multiple intermediaries are involved.

Modern platforms take a different approach. Payment orchestration layers sit above multiple payment rails and route each transaction through the fastest, cheapest, or most compliant path available. A payment from a U.S. company to a Vietnamese supplier might travel through a local payment network in Vietnam rather than bouncing through three correspondent banks. The result is faster settlement and lower fees, without requiring the business to manage each rail separately.

Pro Tip: When evaluating any cross-border payment service, ask specifically how many intermediary banks are involved in your most common payment corridors. Each additional hop adds both cost and delay.

| Method | Settlement Speed | Typical Cost | Key Limitation |

|---|---|---|---|

| SWIFT correspondent banking | 1–3 business days | High, with hidden fees | Multiple intermediaries, trapped liquidity |

| Payment orchestration platforms | Hours to 1 business day | Lower, transparent pricing | Requires platform integration |

| Stablecoin rails | Seconds to minutes, 24/7 | Very low | Regulatory uncertainty in some jurisdictions |

| Local acquiring networks | Near real-time | Low for domestic-appearing transactions | Requires local entity or partner |

What are the main cross-border payment methods?

Cross-border payment methods fall into four practical categories, each with distinct trade-offs in cost, speed, and compliance burden.

SWIFT bank transfers remain the most widely used method for B2B international payments. They are universally accepted and work across virtually every country. The downside is cost and opacity. Card-based cross-border payments incur interchange fees, cross-border assessments, FX conversion margins, and correspondent fees totaling two to five percent per transaction for merchants. That figure compounds quickly at volume.

Card networks (Visa, Mastercard) offer speed and familiarity but carry significant fee layers. Local acquiring solves part of this problem by making a transaction appear domestic to the issuing bank, which reduces the risk perception and improves authorization rates. A European e-commerce company processing payments from U.S. customers, for example, sees measurably better approval rates when using a U.S.-based acquirer.

Stablecoin and blockchain rails represent the fastest-growing segment of international payment infrastructure. Stablecoin rails settle value directly on a blockchain, typically within seconds to minutes, operating 24/7 compared to traditional banking hours. This matters enormously for urgent supplier payments or payroll in time-sensitive markets.

Local payment networks such as SEPA in Europe, PIX in Brazil, or UPI in India allow businesses to make payments that behave like domestic transfers within a region. Access typically requires a local IBAN account or a fintech partner with local presence.

Here is a quick breakdown of each method's practical profile:

- SWIFT transfers: Universal reach, 1 to 3 day settlement, high and often opaque fees, best for large infrequent payments

- Card networks: Fast, familiar, 2 to 5% total cost, best for consumer-facing transactions with local acquiring

- Stablecoin rails: Near-instant, 24/7, very low cost, best for tech-forward businesses in corridors with regulatory clarity

- Local payment networks: Domestic-speed settlement, low cost, limited to specific regions, best for businesses with high transaction volume in a single market

How do cross-border solutions manage multi-currency costs?

Multi-currency account management is where modern cross-border payment solutions deliver the most measurable financial benefit. A cross-border B2B payment account structured around IBANs allows businesses to hold funds in 25-plus currencies on a single platform, avoiding constant FX conversions and giving finance teams control over conversion timing.

The practical implication is significant. When a U.S. company receives payment in euros and immediately converts to dollars at the bank's rate, it accepts whatever spread the bank applies at that moment. Holding euros in a multi-currency account and converting when the rate is favorable can reduce FX losses by a meaningful margin over a fiscal year. This is not speculation. Hidden FX spread losses commonly exceed stated transaction fees, adding unpredictability to cost structures that finance teams struggle to forecast.

Pro Tip: Forward contracts lock in an exchange rate for a future payment date. If you know you will pay a supplier in 60 days, a forward contract removes FX volatility from your cost model entirely.

| Cost Component | Traditional Banking | Modern Platform |

|---|---|---|

| FX conversion spread | 1.5–3%, bank-dictated | 0.1–0.5%, transparent and competitive |

| Correspondent bank fees | $15–$50 per transaction, variable | Flat fee or included in subscription |

| Intermediary deductions | Unpredictable, mid-chain | Eliminated via direct rails |

| Payment tracking | Limited or unavailable | Real-time tracking with delivery estimates |

Real-time payment tracking is an underrated operational benefit. Finance teams that can monitor a payment's movement through intermediaries reduce the time spent on payment disputes and reconciliation. Platforms like iBanFirst and Axon both offer tracking dashboards that show exactly where a payment sits at any given moment, which translates directly into fewer support escalations and faster month-end closes.

What challenges do businesses face with cross-border payments?

Cross-border payments cost up to 10 times more than domestic payments due to multiple intermediaries, FX spreads, and regulatory complexity. That cost gap is the most visible challenge, but it is not the only one.

The compliance burden is substantial and growing. Anti-money laundering (AML) checks, Know Your Customer (KYC) verification, and sanctions screening apply at multiple points in a cross-border transaction. A payment from a U.S. company to a supplier in a high-risk jurisdiction may trigger manual review at two or three banks before it clears. Modern orchestration platforms address this by embedding compliance checks at the routing layer, so the business does not manage each requirement separately.

Settlement finality is another frequently misunderstood issue. Settlement finality differs between traditional banking, where reversals within a window are possible, and blockchain-based settlement, which offers immediate irreversibility upon confirmation. For B2B reconciliation, this distinction matters. A payment that appears confirmed in a traditional system can still be reversed, creating accounting complications that blockchain rails eliminate entirely.

The operational challenges compound for businesses scaling internationally:

- Trapped liquidity: Traditional correspondent banking systems require banks to pre-position funds in nostro accounts, tying up capital that earns no return

- Banking hours constraints: Traditional settlement systems are constrained by local banking hours, causing delays that stablecoin and digital rails avoid entirely

- Opaque fee structures: Correspondent banks deduct fees mid-chain, so the recipient receives less than the sender intended without clear notification

- Compliance fragmentation: Each jurisdiction has different AML and sanctions requirements, creating a compliance patchwork that manual processes cannot manage at scale

"Payment orchestration layers intelligently route each transaction through the fastest, cheapest, or most compliant rail, mixing traditional banking and stablecoin or digital network rails under one integration." This approach, as documented in Axon's 2026 payment guide, eliminates the binary choice between speed and compliance.

Key takeaways

A cross-border payment solution reduces cost, delay, and compliance risk by replacing correspondent banking with orchestrated, multi-rail infrastructure that gives businesses direct control over currency conversion and settlement timing.

| Point | Details |

|---|---|

| Definition is specific | A cross-border payment solution handles currency conversion, routing, compliance, and settlement in one platform. |

| Correspondent banking has real costs | Trapped liquidity and intermediary fees make traditional SWIFT transfers up to 10 times more expensive than domestic payments. |

| Multi-currency accounts save money | Holding funds in 25-plus currencies lets businesses convert at favorable rates instead of accepting bank-dictated spreads. |

| Settlement finality varies by rail | Blockchain-based rails offer irreversible settlement; traditional banking allows reversals, which complicates B2B reconciliation. |

| Orchestration is the modern standard | Payment orchestration platforms route transactions dynamically, optimizing for cost, speed, and compliance simultaneously. |

What I've learned about choosing cross-border payment infrastructure

Most businesses I've worked with underestimate the true cost of their international payments by a factor of two or three. They see the wire transfer fee on the invoice and stop there. They do not account for the FX spread applied at the bank's discretion, the correspondent fees deducted mid-chain, or the float cost of funds sitting in transit for two days. When you add those up across a year of supplier payments, the number is often shocking.

The businesses that manage international payments well share one characteristic: they treat payment infrastructure as a strategic financial decision, not an administrative one. They evaluate platforms on FX transparency, rail diversity, and compliance automation, not just headline fees. A platform that charges a slightly higher flat fee but offers real-time tracking, forward contracts, and local payment network access will almost always cost less in total than a legacy bank account with a low stated wire fee.

My honest advice on vendor selection: ask any platform to show you the all-in cost for your three most common payment corridors, including FX spread, before you commit. Platforms that cannot or will not provide that number are hiding something. The best providers, including those built on modern international money transfer infrastructure, make this information available upfront because transparency is their competitive advantage.

The future of cross-border payments belongs to orchestration. Businesses that lock themselves into a single bank or single rail are accepting unnecessary constraints. The platforms worth building on are those that route intelligently across multiple rails and let you add corridors as your business grows.

— Ahmed

How Sigmaplatinum supports international business payments

Sigmaplatinum is a B2B fintech platform built specifically for international businesses that need more than a standard bank account to manage cross-border operations.

The platform provides access to multi-currency business accounts with IBAN structures, supporting FX workflows, multi-currency holding, and corporate payment tools through regulated partners. Digital agencies, consulting firms, and import/export companies use Sigmaplatinum to reduce the friction of international payments without building custom banking integrations. The compliance-focused onboarding process, including rigorous KYB checks, means businesses get access to serious payment infrastructure without the delays of traditional bank applications. If you are managing payments across multiple currencies and corridors, Sigmaplatinum is worth evaluating as your primary business payment account.

FAQ

What does cross-border payment settlement mean?

Cross-border payment settlement is the process by which funds are finalized and transferred from the sender's account to the recipient's account across national borders. Settlement timing varies by rail: SWIFT corridors average one to three business days, while blockchain-based rails offer near-instant, irreversible settlement.

What is a cross-border B2B payment account?

A cross-border B2B payment account is a business account, typically structured around IBANs, that allows companies to hold, send, and receive funds in multiple currencies without converting on every transaction. These accounts are designed for businesses with recurring international payment needs, such as supplier payments, contractor payroll, or intercompany transfers.

How do cross-border payments work through payment orchestration?

Payment orchestration platforms route each transaction through the optimal rail, whether SWIFT, a local payment network, or a stablecoin rail, based on cost, speed, and compliance requirements. The business integrates once with the orchestration layer and gains access to multiple rails without managing each separately.

What are the main advantages of cross-border payment solutions over traditional banking?

Modern cross-border payment solutions reduce costs by eliminating intermediary hops, provide transparent FX pricing, offer real-time tracking, and automate compliance checks. Traditional correspondent banking, by contrast, involves multiple fee layers, opaque FX spreads, and settlement delays that compound at scale.

How much do cross-border transactions typically cost?

Cross-border payments cost up to 10 times more than domestic payments due to intermediary fees, FX spreads, and compliance overhead. Card-based international transactions add two to five percent in total fees per transaction, while modern orchestration platforms and local payment networks can reduce this significantly.