A multi-currency business account is a single financial account that lets your company hold, receive, and send funds in multiple currencies without converting every transaction at the moment it arrives. Platforms like Wise Business, Airwallex, and Revolut Business have made this model standard for internationally active companies. The core advantage is control: instead of your bank automatically converting a euro payment into dollars at a rate it chooses, you decide when and whether to convert. For founders and financial managers running cross-border operations, that control directly affects your bottom line.

How does a multi-currency business account work?

The mechanics are straightforward once you understand the structure. A multi-currency account is built around currency sub-accounts, each with its own local banking details.

Here is how the process works in practice:

- Open sub-accounts for each currency you need. Each sub-account carries individual IBANs or routing numbers for that specific currency and country. A UK-based company can hold a USD sub-account with a US routing number, a EUR sub-account with a European IBAN, and a GBP sub-account simultaneously.

- Receive payments in the original currency. A client in Germany pays you in euros. That payment lands in your EUR sub-account without any automatic conversion. You hold the euros until you choose to act.

- Convert on your schedule. When the exchange rate favors you, you convert the balance. Traditional banks convert all incoming funds immediately, often with high fees, removing that decision from your hands entirely.

- Send payments in local currency. You pay a supplier in Japan in yen directly from your JPY sub-account. No double conversion, no surprise fees.

Transactions processed through local payment rails complete in 1–2 days, compared to the 3–5 days typical of international wire transfers. That speed difference matters when you are managing supplier deadlines or client payment cycles.

Pro Tip: Set rate alerts inside your account platform so you convert currency balances only when the market moves in your favor, not out of urgency.

What are the primary benefits of multi-currency business accounts?

The benefits of multi-currency business accounts are most visible when you calculate what you currently lose to fees and friction.

- FX fee savings. Businesses avoid the typical 2–5% hidden FX markup that traditional banks embed in their exchange rates. On $500,000 in annual foreign revenue, that markup costs $10,000–$25,000 per year.

- Simplified payment workflows. Consolidating currency management into one banking relationship eliminates the need for multiple accounts at different banks, reduces manual reconciliation, and cuts accounting errors.

- Better cash flow control. You hold foreign currency balances and convert when rates are favorable, rather than accepting whatever rate your bank applies at the moment of receipt.

- Local credibility in multiple markets. Some fintech platforms provide local currency accounts in 17+ countries, letting you receive payments as a local payee. Clients in France see a French IBAN. Clients in the US see a US bank account. That removes friction at the point of payment.

- Broad use case coverage. E-commerce sellers on Amazon or Etsy, SaaS companies billing in multiple currencies, import/export firms, digital agencies, and consulting firms with international clients all benefit from this structure.

"The ability to hold multiple currencies simultaneously and pay exchange fees only when converting voluntarily is the defining advantage over traditional banking." — Razorpay Business Finance Guide

For UK companies specifically, the multi-currency account benefits extend to managing both EU and US revenue streams post-Brexit without maintaining separate banking relationships in each jurisdiction. That is a structural efficiency most single-currency accounts cannot match.

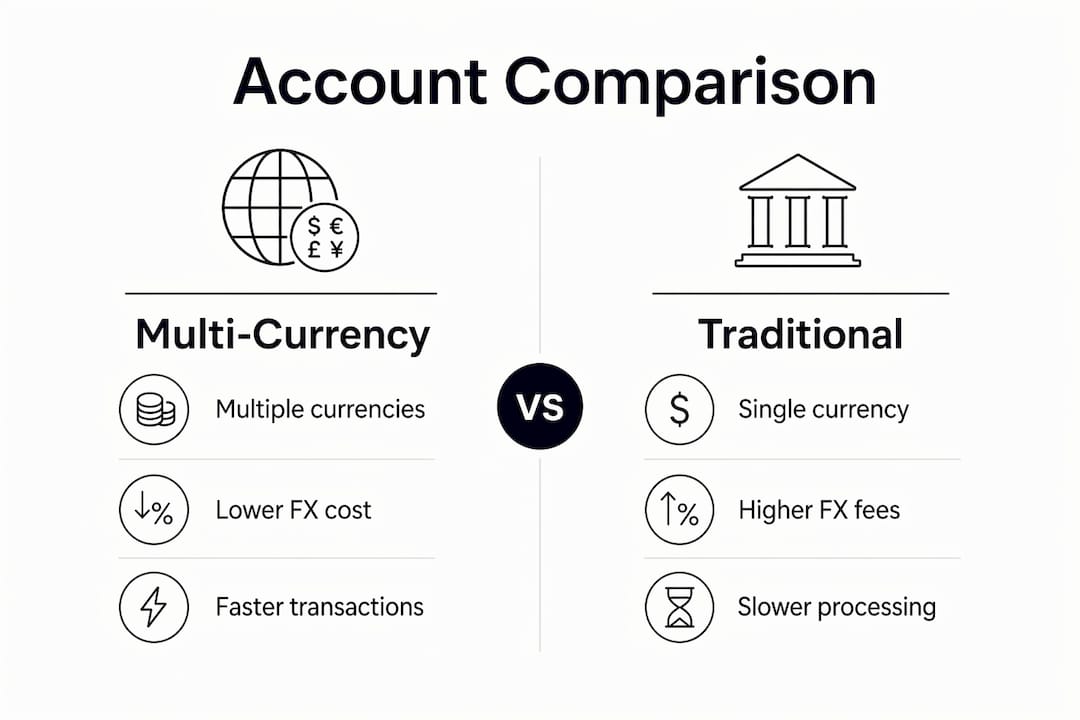

Multi-currency accounts vs. traditional accounts: a direct comparison

Understanding where a multi-currency account outperforms traditional options helps you decide whether the switch is worth it for your business.

| Feature | Multi-Currency Account | Traditional Business Account |

|---|---|---|

| Currency holding | Multiple currencies simultaneously | Single currency only |

| Conversion control | Business decides when to convert | Bank converts automatically on receipt |

| FX fees | Transparent, often near mid-market rate | Embedded markup of 2–5% |

| Local bank details | Available in multiple countries | Domestic only |

| Transfer speed | 1–2 days via local rails | 3–5 days for international wires |

| Account complexity | One account, multiple sub-accounts | Separate accounts per currency needed |

Third-party currency conversion services like OFX offer competitive FX rates but do not provide the full account infrastructure. You cannot receive payments or hold balances the same way. Payment processors like Shopify Payments or Amazon Seller Central do include built-in currency management, which can make a separate multi-currency account redundant if your volume is low and your sales stay within those platforms. Once you operate across multiple channels or need to pay suppliers directly, a dedicated account becomes the cleaner solution.

Pro Tip: Before opening a new account, audit your existing payment processor. If Shopify or Amazon already handles your currency needs at acceptable cost, adding another account creates reconciliation work without proportional benefit.

What factors should you evaluate when choosing a provider?

Choosing the right provider requires matching the account's capabilities to your specific payment flows, not just picking the most recognized brand.

- Currency coverage. Confirm the platform supports every currency you actively use. Some providers cover 30+ currencies; others focus on major pairs only. A business with revenue in Thai baht or Nigerian naira needs to verify coverage before committing.

- Fee transparency. Look for providers that publish their FX spread clearly. A platform advertising "no fees" but applying a 1.5% spread on every conversion is not fee-free.

- Local bank details availability. Verify which countries offer true local account numbers. Receiving a payment "in USD" through a correspondent bank is not the same as having a US routing number and account number.

- Software integration. Reputable multi-currency accounts offer API integrations and compatibility with accounting platforms like Xero, QuickBooks, and NetSuite. If your finance team reconciles in Xero, disconnected account data creates manual work every month.

- Compliance and eligibility. Providers apply KYB (Know Your Business) checks. High-risk industries, newly incorporated companies, or businesses in certain jurisdictions face additional scrutiny. Review eligibility requirements for high-risk firms before applying to avoid wasted time.

- Scalability and support. A startup processing $50,000 per month has different support needs than a firm processing $5 million. Confirm that the provider's support tier matches your transaction volume and complexity.

For businesses operating in the UAE, the multi-currency business account Dubai market has grown significantly, with both local banks and international fintechs competing for corporate clients. The choice between a UAE-licensed bank and a global fintech depends on whether you need a local physical presence or prioritize digital-first workflows.

What are the main risks and how do you manage them?

A multi-currency account reduces costs, but it introduces new operational responsibilities. Here are the primary risks and how to address each one.

- Idle currency balances. Holding large balances in a depreciating currency costs money. Managing multiple currency balances carefully to avoid idle funds is one of the most commonly overlooked operational tasks. Set a review schedule, monthly at minimum, to assess whether held balances should be converted or deployed.

- Exchange rate volatility. Waiting for a better rate is a strategy, not a guarantee. Businesses with predictable foreign currency expenses should consider forward contracts or rate alerts to lock in acceptable rates rather than speculating on market movement.

- Fee complexity on currency swaps. Some platforms charge differently for converting between non-USD pairs. Converting euros to yen may route through USD as an intermediate step, applying two conversion fees. Understand your provider's conversion path before executing large transactions.

- Reconciliation across currencies. Multiple sub-accounts mean multiple balance lines in your accounting software. Without clean integration between your account platform and your accounting tool, month-end close becomes significantly more complex. Automate the data feed wherever possible.

Cash flow planning across currencies is not optional. It is the operational discipline that determines whether a multi-currency setup saves money or creates new problems.

Key takeaways

A multi-currency business account saves money and reduces complexity only when you actively manage currency balances, choose a provider matched to your transaction flows, and integrate the account with your existing financial software.

| Point | Details |

|---|---|

| Core definition | A multi-currency account holds, receives, and sends funds in multiple currencies under one account structure. |

| Primary cost benefit | Avoiding the 2–5% FX markup from traditional banks is the single largest financial gain for high-volume international businesses. |

| Provider selection | Match currency coverage, local bank details, and software integrations to your actual payment flows before choosing a platform. |

| Key risk to manage | Idle foreign currency balances and unconverted funds exposed to rate swings are the most common operational pitfalls. |

| When to reconsider | If your payment processor already handles currency management at acceptable cost, a separate account may add complexity without proportional savings. |

What i have learned running international payment workflows

Most founders I speak with open a multi-currency account because they heard it saves money on FX. That is true. But the businesses that extract the most value treat it as a payment infrastructure decision, not just a cost-cutting move.

The mistake I see repeatedly is choosing a provider based on brand recognition rather than fit. Wise Business is excellent for small to mid-size companies with straightforward currency needs. Airwallex is better suited for businesses that need deep API integration and local account numbers across Asia-Pacific markets. Neither is universally superior. The right choice depends on where your money actually flows.

I also think most businesses underestimate the reconciliation burden. Opening sub-accounts in five currencies sounds clean until your finance team is manually matching transactions across five balance lines every month. The cross-border payment infrastructure you choose needs to connect directly to your accounting software, or you will spend more in staff time than you save in FX fees.

The businesses that benefit most are import/export companies, digital agencies billing international clients, and SaaS firms with multi-region revenue. If your international revenue is below 10% of total revenue and concentrated in one currency, the operational overhead may not justify the switch yet. When you cross that threshold, the case becomes clear.

— Ahmed

How Sigmaplatinum supports international payment workflows

Sigmaplatinum is built specifically for international businesses that need more than a standard bank account. The platform provides access to multi-currency business payment accounts through regulated partners, with compliance-focused onboarding that includes rigorous KYB checks. Digital agencies, consulting firms, and import/export companies use Sigmaplatinum to manage FX workflows, receive payments in local currencies, and connect their financial operations without the complexity of managing multiple banking relationships. If you are evaluating your options for holding multiple currencies under one account, Sigmaplatinum's no-code access model gets you operational faster than traditional bank onboarding. Explore the platform at Sigmaplatinum to see which account structures fit your business model.

FAQ

What is a multi-currency business account?

A multi-currency business account is a single account that lets companies hold, receive, and send funds in multiple currencies, each in its own sub-account with local banking details. It gives businesses control over when to convert currency rather than accepting automatic bank conversions.

How many currencies can a multi-currency account hold?

The number varies by provider. Platforms like Airwallex and Wise Business support 30+ currencies, while some regional providers focus on major pairs like USD, EUR, and GBP.

Are multi-currency accounts worth it for small businesses?

They are worth it when a meaningful share of your revenue or expenses involves foreign currencies. If your international transactions are low volume or handled by an existing payment processor, the added complexity may outweigh the savings.

What is the difference between a multi-currency account and a foreign currency account?

A foreign currency account holds one specific foreign currency. A multi-currency account holds several currencies simultaneously under one account structure, each in its own sub-account with separate local banking details.

Do multi-currency accounts work for businesses in dubai?

Yes. The multi-currency business account Dubai market includes both UAE-licensed banks and international fintech platforms. Businesses operating from the UAE use these accounts to manage USD, EUR, AED, and other currencies relevant to their trade corridors. Check multi-jurisdiction account advantages for UAE-specific structuring considerations.