Receiving international payments as a UK business is defined by two decisions: which account details you share with overseas clients, and which payment method you use to convert incoming funds. Most UK businesses default to their existing bank account, but traditional banks apply FX margins of 2–3% on every conversion, compared to 0.3–0.8% with currency specialists. On £200,000 in annual receipts, that gap costs up to £4,800 per year in fees you never see itemized. The right setup for cross-border payment services in the UK combines accurate banking details, a multi-currency account, and an FCA-authorized platform.

What banking details do UK businesses need to receive international payments?

Every UK business that wants to receive international payments must provide four pieces of information to overseas clients. Missing or incorrect details cause delays, rejected transfers, and short payments that are difficult to trace.

The four required details are:

- IBAN (International Bank Account Number): UK IBANs are 22 characters long and replace the sort code and account number for international transfers. Every UK bank account has one.

- BIC/SWIFT code: This is an 8 or 11-character code that identifies your specific bank. It tells the sending bank exactly where to route the funds.

- Account name: The name must match your registered business name exactly. Even a minor spelling difference can trigger a compliance hold at the receiving bank.

- Bank physical address: US clients in particular often require a full bank branch address because US domestic systems do not use IBAN. Omitting this detail is the single most common reason UK businesses experience delayed payments from American clients.

One additional step most businesses overlook: state the invoice currency explicitly on every invoice. Clear payment instructions that specify currency reduce disputes and processing errors at the client's end. A consulting firm invoicing a German client in euros, for example, should write "EUR" prominently on the invoice rather than leaving the client to assume.

Pro Tip: Create a standard "payment instructions" document in PDF format that includes all four details above. Attach it to every invoice sent to an overseas client. This eliminates back-and-forth emails and speeds up payment.

How can UK businesses reduce costs when receiving international payments?

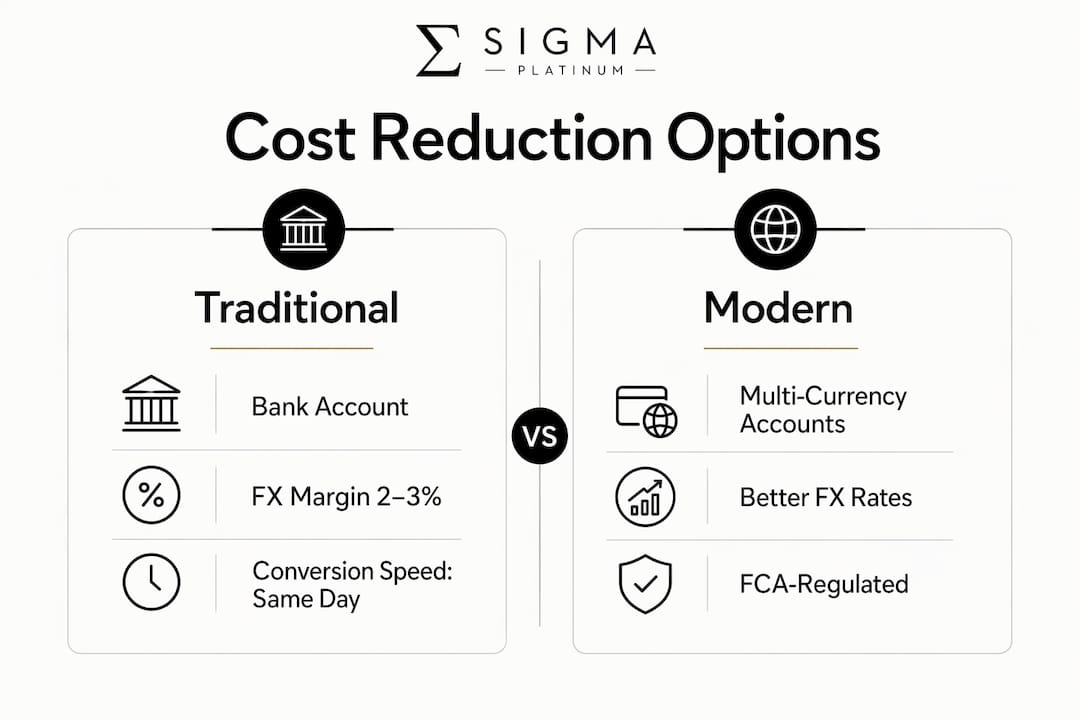

The biggest cost in receiving cross-border payments is not the transfer fee. It is the FX margin applied when your bank converts incoming foreign currency into sterling. Traditional bank accounts automatically convert currency at high margins without explicit client approval. That means you often have no idea how much you lost until you check the final deposit.

Comparing your main cost-reduction options

| Method | Typical FX margin | Conversion speed | Best for |

|---|---|---|---|

| Traditional bank account | 2–3% | Same day | Simple, low-volume receipts |

| Currency specialist platform | 0.3–0.8% | 1–2 working days | Regular or high-value receipts |

| Multi-currency account | 0–0.5% (held, not converted) | Instant hold; timed conversion | Businesses with multi-currency outgoings |

| Invoice in sterling | 0% (FX risk shifts to client) | Depends on client's bank | Service businesses with pricing power |

Invoicing in sterling is the simplest way to eliminate FX risk entirely. The client's bank handles the conversion, and you receive exactly what the invoice states. The trade-off is that some overseas clients resist paying in a foreign currency, particularly in markets where the euro or US dollar is the default.

Multi-currency accounts let UK businesses hold funds in euros, US dollars, or other currencies without converting immediately. This is valuable when you also pay overseas suppliers in the same currency. An import/export company receiving euros from French clients and paying Italian suppliers in euros can hold those funds and transfer them directly, bypassing conversion costs on both ends.

FCA-authorized currency specialists provide better FX rates than banks and segregate client funds under regulatory oversight. That segregation matters: if the platform fails, your funds are protected separately from the company's own assets.

Pro Tip: Time your currency conversions around known market events. Central bank rate decisions from the Bank of England, the Federal Reserve, or the European Central Bank regularly move exchange rates by 0.5–1% in a single session. Converting before a major announcement locks in a known rate.

How to set up a multi-currency account for your UK business

A multi-currency business account is a single account that holds balances in multiple currencies simultaneously. You receive euros as euros, dollars as dollars, and convert only when the rate is favorable or when you need sterling for domestic expenses.

Setting one up involves five steps:

- Confirm your business structure. Most platforms require a registered UK limited company or LLP. Sole traders can access some accounts but face more restrictions on supported currencies.

- Complete KYB (Know Your Business) verification. You will need your Companies House registration number, proof of business address, and director ID documents. FCA-authorized platforms apply stricter checks than basic bank accounts, but that rigor protects you.

- Select your required currencies. Identify which currencies your clients pay in most frequently. EUR, USD, and CAD cover the majority of UK business receipts from Europe and North America.

- Set up local receiving details. Many multi-currency platforms issue local account numbers in each currency. A US client can pay your USD account as if it were a domestic US transfer, which reduces their fees and speeds up the transfer.

- Define your conversion rules. Decide whether you want automatic conversion at a set threshold or manual control over every conversion. Manual control costs more time but gives you full visibility over your effective rate.

For businesses with predictable future receipts, forward contracts lock in an exchange rate up to 12 months in advance. If you know a client will pay €50,000 in six months, a forward contract eliminates the risk that sterling strengthens before the payment arrives.

Pro Tip: Check the multi-currency account eligibility checklist before applying to any platform. Incomplete applications trigger manual reviews that can delay account opening by weeks.

The compliance step is non-negotiable. Only use platforms that are authorized or registered with the Financial Conduct Authority (FCA). FCA authorization means the platform must segregate client funds and submit to regular audits. A platform without FCA oversight offers no regulatory protection if something goes wrong.

What are the best practices for tracking and troubleshooting international payments?

Even well-structured international payment setups encounter delays. Knowing how to trace a problem quickly saves time and protects client relationships.

The most useful tool for tracing a delayed transfer is the MT103 reference. MT103 is the standard SWIFT message that carries detailed tracking information for every international wire transfer. Ask your client to provide the MT103 reference number when they initiate the payment. With that reference, your bank or platform can trace exactly where the funds are in the SWIFT network.

Key practices for clean international payment management:

- Build transfer time into your payment terms. SWIFT payments take 1–2 working days under normal conditions, but correspondent bank routing can add another day or two. Set payment terms of "net 5 working days" rather than "net 3" for international clients.

- Keep a payment audit trail. Save every MT103 reference, every confirmation email, and every exchange rate applied. This documentation is critical for tax reporting and for resolving disputes with clients or HMRC.

- Communicate proactively. If a payment is late, contact the client with the expected transfer timeline before raising a formal dispute. Most delays are administrative, not intentional.

- Check for short payments. Correspondent banks sometimes deduct their own fees from the transferred amount. If you receive less than invoiced, request a full fee breakdown from your bank before chasing the client.

The most preventable payment problem in international business is the one caused by incomplete instructions. A missing bank address or an incorrect account name does not just delay a payment. It can trigger a compliance review at the correspondent bank that holds funds for five to ten working days. Sending complete, verified payment details with every invoice is the single highest-return habit a UK business can build.

What I've learned about the real cost of default banking for international receipts

Most UK business owners I speak with have never calculated their actual FX cost for the year. They see a transfer fee of £15 or £25 and assume that is the full cost. The FX margin is invisible because it is baked into the exchange rate the bank applies, not listed as a separate line item.

The math is straightforward once you run it. A business receiving £300,000 equivalent in foreign currency annually loses between £6,000 and £9,000 per year at a 2–3% bank margin. A currency specialist at 0.5% costs £1,500 on the same volume. That £4,500 to £7,500 difference is real profit, not a theoretical saving.

The second misconception I see constantly is that multi-currency accounts are complicated to manage. They are not. The setup takes a few days. After that, the account works like any other business account, except you have separate balances per currency and full control over when you convert. For any business with recurring international receipts, the time investment pays back within the first month.

The trend worth watching in 2026 is the expansion of local payment rails. Platforms are increasingly issuing local account numbers in the US, EU, and Australia, so your overseas clients pay domestically and the funds arrive in your multi-currency account without touching the SWIFT network at all. That eliminates correspondent bank fees and cuts transfer times to hours rather than days.

— Ahmed

Sigmaplatinum's business payment account for international receipts

Sigmaplatinum is a B2B fintech platform built specifically for UK and international businesses that need efficient, compliant payment workflows across multiple currencies.

Sigmaplatinum's business payment account gives you access to multi-currency holding, competitive FX rates through regulated partners, and a compliance-first onboarding process that includes full KYB verification. Digital agencies, consulting firms, and import/export companies use Sigmaplatinum to receive funds from overseas clients without the hidden margins that traditional banks apply. The platform operates through a no-code model, so you get up and running quickly without technical complexity. If your business handles recurring cross-border receipts and you want full visibility over every conversion, Sigmaplatinum is worth a direct inquiry.

Key takeaways

UK businesses that use multi-currency accounts and FCA-authorized currency specialists reduce their international payment costs by up to 2.5% per transaction compared to traditional banks.

| Point | Details |

|---|---|

| Provide complete banking details | Always include IBAN, BIC/SWIFT, account name, and bank address on every invoice. |

| Switch from bank FX to specialists | Currency specialists charge 0.3–0.8% FX margins versus 2–3% at traditional banks. |

| Use multi-currency accounts | Hold foreign currency balances and convert only when rates are favorable. |

| Track payments with MT103 | Request the MT103 reference from clients to trace any delayed SWIFT transfer. |

| Build transfer time into terms | Set international payment terms at net 5 working days to account for SWIFT routing. |

FAQ

What details do I need to receive international payments in the UK?

UK businesses need to provide their IBAN, BIC/SWIFT code, registered account name, and bank physical address. US clients in particular require the bank address because US domestic systems do not use IBAN.

How long does an international bank transfer take to arrive in the UK?

SWIFT transfers typically take 1–2 working days, though correspondent bank routing can extend this to 3–4 days. Building extra time into your payment terms prevents disputes over delays.

What is an MT103 and why does it matter?

An MT103 is the standard SWIFT message that tracks an international wire transfer through the banking network. Keeping the MT103 reference from your client lets you trace any delayed or short payment quickly.

Are multi-currency accounts safe for UK businesses?

Multi-currency accounts operated by FCA-authorized platforms are safe because FCA authorization requires segregation of client funds and regular regulatory audits. Always verify FCA registration before opening an account.

Is it cheaper to invoice overseas clients in sterling?

Invoicing in sterling eliminates your FX risk entirely because the client's bank handles the conversion. The trade-off is that some clients prefer to pay in their own currency, so this approach works best when you have pricing power in the relationship.