A multi-currency B2B payment account is defined as a business account that lets you hold, receive, convert, and send multiple currencies from a single platform. For UK and GCC finance managers running cross-border operations, the multi-currency b2b payment account setup process is the single most consequential financial infrastructure decision you will make. Done right, it cuts FX costs, speeds up supplier payments, and eliminates the reconciliation headaches that come with routing every foreign payment through a single domestic account. Platforms like Airwallex, Payoneer, and Thunes have made this infrastructure accessible to businesses well below enterprise scale.

What documents and prerequisites do you need for setup?

The documentation stage is where most applications stall. UK AML onboarding requires specific company documents including a certificate of incorporation, beneficial ownership information for any individual holding 25% or more, director IDs, proof of address, and a clear description of expected payment flows. Each item has a purpose. The beneficial ownership disclosure tells the compliance team who ultimately controls the money. The source-of-funds narrative tells them where it comes from.

For GCC-based businesses, requirements vary by jurisdiction but follow a similar logic. UAE-registered companies typically need a trade license, memorandum of association, Emirates ID copies for directors, and a bank reference letter. Saudi Arabia adds a Commercial Registration certificate and SAMA-related disclosures for regulated entities. The underlying principle across both regions is the same: prove the business is real, prove who owns it, and explain what the money is for.

Onboarding delays most often come from inconsistent beneficial ownership information and missing source-of-funds explanations. A director listed differently across documents, or a vague description of revenue sources, triggers a manual review that can add weeks to the process.

The most reliable way to avoid this is to pre-build a KYB evidence pack before you apply. Assemble all entity legal documents, beneficial ownership details, identification, and source-of-funds narratives in a consistent format. Check that names, addresses, and registration numbers match exactly across every document.

Required documents checklist:

- Certificate of incorporation or equivalent trade license

- Beneficial ownership register (all individuals at 25% or above)

- Government-issued ID for each director and beneficial owner

- Proof of address dated within the last three months

- Business bank statements (typically three to six months)

- Source-of-funds narrative explaining revenue model and expected transaction patterns

- Corporate structure chart if the business has holding companies above it

Pro Tip: Write your source-of-funds narrative as a one-page summary, not a paragraph. List your revenue sources, average transaction sizes, and the countries you pay and receive from. Compliance reviewers process dozens of applications daily. A clear, structured narrative gets approved faster than a dense block of text.

Which payment rails and platforms should you use?

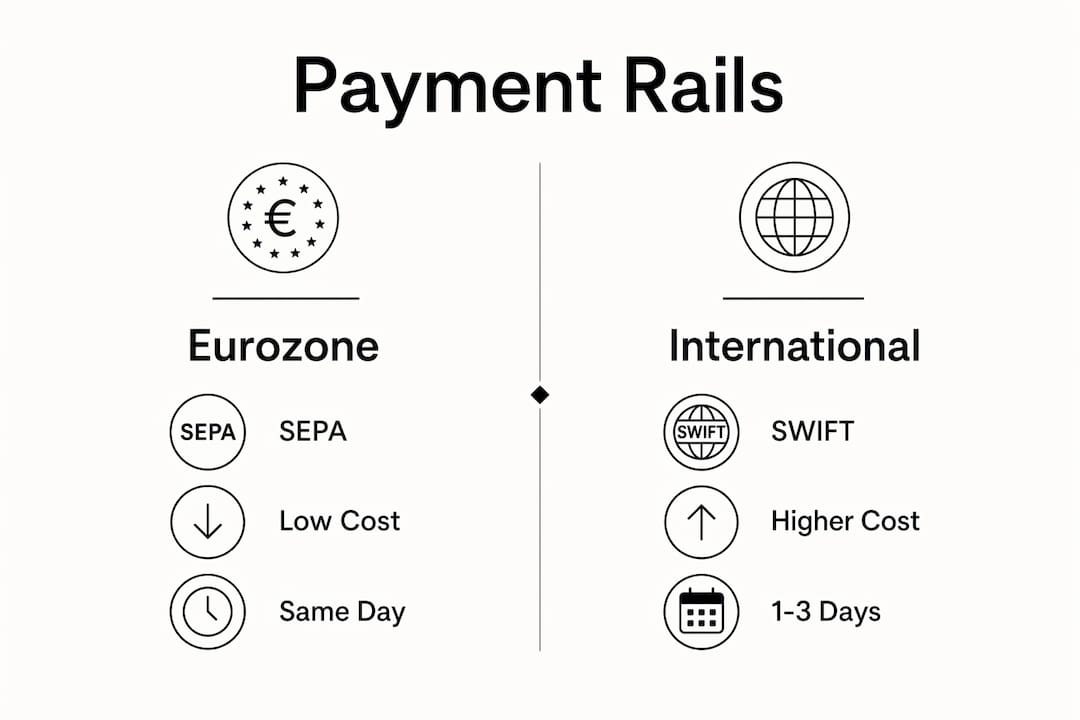

Payment rails are the infrastructure that moves money between accounts. The choice of rail determines cost, speed, and geographic reach. Local rails like SEPA, Faster Payments, and ACH reduce costs and speed up settlement compared to SWIFT, but their coverage is geographically limited. SEPA covers the Eurozone. Faster Payments covers the UK. ACH covers the US. For payments outside these corridors, SWIFT remains the default, though it carries higher fees and slower settlement.

Virtual IBANs add a layer of flexibility that traditional bank accounts cannot match. A virtual IBAN is a unique account number assigned to your business in a specific currency and country. It lets counterparties pay you as if you have a local account in their market, even when you do not. This is particularly useful for UK businesses receiving EUR payments from European clients, or GCC businesses collecting USD from American buyers.

| Rail | Coverage | Typical cost | Settlement speed |

|---|---|---|---|

| SEPA | Eurozone | Low | Same day to 1 business day |

| Faster Payments | United Kingdom | Very low | Near instant |

| ACH | United States | Low | 1–3 business days |

| SWIFT | Global | $15–$45 per transfer | 1–5 business days |

| Local GCC rails | UAE, Saudi Arabia, others | Variable | Same day to 2 business days |

API-first providers offer multi-rail connectivity from a single integration. Routefusion, for example, connects businesses to multiple local rails and SWIFT through one API. This matters for finance teams because it means you do not need separate banking relationships for each currency corridor. You configure routing rules once, and the platform selects the best rail per transaction.

When selecting a platform, prioritize four factors: the currencies and corridors it covers, its fee structure on both FX and transfers, its compliance standing in your jurisdiction, and the quality of its API or dashboard for your team's workflow. A platform with 50 currencies but no GCC coverage is the wrong choice for a Dubai-based importer.

Pro Tip: Ask every platform candidate for a full fee schedule before you apply. FX spread, transfer fees, monthly account fees, and inactivity fees all compound. A platform with a low transfer fee but a wide FX spread can cost more than a platform with a higher transfer fee and a tighter spread, depending on your transaction volume.

How to open and configure a multi-currency B2B payment account

The setup process follows a predictable sequence. Executing each step cleanly is what separates a two-week approval from a two-month one.

-

Prepare your KYB evidence pack. Gather all documents listed in the prerequisites section. Confirm that names and registration numbers are consistent across every document. Save everything in a single organized folder before you begin any application.

-

Select your platform and submit the application. Choose the platform that matches your currency corridors and compliance requirements. Complete the online application form accurately. Upload your KYB evidence pack in the formats the platform specifies. PDF is almost universally accepted. Scanned images in JPEG format are frequently rejected.

-

Complete the compliance interview if required. Many platforms, including those operating under FCA regulation in the UK, conduct a short call or written questionnaire to verify your source-of-funds narrative. Answer directly and consistently with what you submitted in writing.

-

Configure your currency holdings. Once approved, set up the currency wallets you need. Start with the currencies that represent your highest transaction volume. For a UK business trading with the UAE and the US, that typically means GBP, USD, and AED at minimum.

-

Set your FX conversion preferences. Decide whether you want automatic conversion on receipt of funds or manual conversion at a time you choose. Holding multiple currencies eliminates the need for immediate conversion, which improves liquidity management and gives you control over when you take an FX rate.

-

Connect your ERP or accounting system. Most platforms offer native integrations with Xero, QuickBooks, NetSuite, and SAP. Connect your accounting system before you process your first transaction. This makes reconciliation automatic from day one rather than a manual catch-up exercise later.

-

Run a test transaction. Send a small payment to a known counterparty in each currency corridor before processing live business payments. Confirm the funds arrive correctly, the fee matches the schedule, and the transaction appears correctly in your accounting system.

-

Document your internal routing policy. Decide which rail your team uses for each corridor and under what conditions. Write this down. Finance teams that develop internal routing policies based on cost, speed, and compliance avoid the operational inefficiencies that come from ad hoc decisions.

A common onboarding pitfall is submitting documents in the wrong format or with mismatched details. Another is failing to explain a gap in business bank statements, such as a period of low activity during a restructuring. Address these proactively in your source-of-funds narrative rather than waiting for a compliance query.

Best practices for managing a multi-currency payment account

Active management of your currency balances is the difference between a multi-currency account that saves money and one that just adds complexity. Multi-currency accounts reduce FX exposure by letting you hold funds in the currency you received them in and convert only when the rate is favorable. This is the core operational advantage over a single-currency account.

Operational best practices:

- Review your currency balances weekly. Idle balances in low-yield currencies represent an opportunity cost.

- Set FX conversion alerts at target rates rather than converting reactively. Most platforms support rate alerts natively.

- Use smart payment routing to automatically select the best rail by destination, speed, and cost. Multi-rail orchestration consistently produces better outcomes than manual rail selection.

- Audit your FX spreads quarterly. Spreads on the same currency pair can vary significantly between platforms and between transaction sizes.

- Keep your compliance documentation current. Update beneficial ownership records immediately when shareholders change. Outdated records trigger account reviews and can freeze transactions.

Pro Tip: Segment your currency balances by purpose. Keep a separate wallet for supplier payments and a separate one for holding receivables. This makes cash flow forecasting cleaner and prevents you from accidentally converting funds you need for a specific payment.

Multi-currency accounts also serve as platforms for broader financial services including spend management, mass payouts, and working capital tools. Finance managers who treat these accounts as workflow infrastructure rather than just FX tools extract significantly more value from them.

Key Takeaways

A successful multi-currency B2B payment account setup requires clean KYB documentation, the right payment rail selection, and active balance management from day one.

| Point | Details |

|---|---|

| Documentation is the critical path | Pre-build a KYB evidence pack with consistent beneficial ownership and source-of-funds details before applying. |

| Rail selection drives cost and speed | Use local rails like SEPA and Faster Payments where available; reserve SWIFT for corridors with no local alternative. |

| FX control requires active management | Hold currencies rather than converting on receipt to reduce FX costs and improve liquidity. |

| Integration prevents reconciliation debt | Connect your ERP or accounting system before processing the first live transaction. |

| Compliance is ongoing, not one-time | Update beneficial ownership records immediately after any shareholder change to avoid account freezes. |

What I've learned from watching businesses get this wrong

The most common mistake I see is treating the multi-currency account application like a bank account application. It is not. Banks have long-standing relationships with their business clients. Fintech platforms and payment providers are meeting you for the first time, and their compliance teams are under significant regulatory pressure. They cannot give you the benefit of the doubt the way a relationship banker might.

The businesses that get approved quickly are the ones that over-document rather than under-document. They submit a corporate structure chart nobody asked for. They include a one-page business summary alongside the required documents. They answer the source-of-funds question with specifics: "We receive USD payments from US-based SaaS clients via ACH, averaging $15,000 per transaction, 12 times per month." That level of detail removes ambiguity and removes the reason for a compliance query.

The second mistake is choosing a platform based on marketing rather than corridor coverage. A platform that looks impressive in a demo but does not support AED or SAR local rails is a poor fit for a GCC-focused business. Always test the specific corridors you need before committing.

The third mistake is ignoring the account after setup. Multi-currency accounts function as financial platforms with services well beyond currency holding. Finance managers who revisit their platform's feature set every six months consistently find tools they were not using that would reduce costs or manual work. The account you set up today is not the same product it will be in twelve months.

— Ahmed

How Sigmaplatinum supports multi-currency account access for UK and GCC businesses

Sigmaplatinum is built specifically for international businesses that need efficient payment account access without the friction of traditional banking. The platform connects UK and GCC businesses to regulated partners that support multi-currency transactions, FX workflows, and corporate payment tools through a compliance-focused onboarding process that includes rigorous KYB checks.

For digital agencies, consulting firms, and import/export companies, Sigmaplatinum removes the complexity of managing multiple banking relationships across jurisdictions. The no-code model means finance teams get access to business payment account services quickly, without lengthy technical integrations. If you are setting up multi-currency payment infrastructure for cross-border operations, Sigmaplatinum is a direct path to the account access and payment rails your business needs.

FAQ

What documents are required for a multi-currency B2B account?

UK businesses need a certificate of incorporation, beneficial ownership details for all individuals holding 25% or more, director IDs, proof of address, and a source-of-funds narrative. GCC businesses typically add a trade license and relevant regulatory disclosures.

How long does multi-currency account onboarding take?

Onboarding timelines vary by platform and documentation quality. Well-prepared applications with complete KYB evidence packs typically complete compliance review faster than incomplete submissions, which often require multiple follow-up rounds.

What is a virtual IBAN and why does it matter?

A virtual IBAN is a unique account number that lets your business receive payments as if you hold a local account in a specific country and currency. It removes the need for counterparties to use SWIFT for payments they could make locally.

Which payment rail is best for GCC to UK transfers?

SWIFT remains the primary rail for GCC to UK transfers where local alternatives are unavailable. Some platforms offer cross-border payment solutions that route through correspondent banking networks to reduce fees and settlement times on this corridor.

Can a multi-currency account replace a traditional business bank account?

A multi-currency payment account handles international transactions, FX conversion, and multi-rail payments effectively. Most businesses use it alongside a domestic bank account rather than as a full replacement, particularly for local payroll and tax payments.