A UK business payment account is a dedicated financial account that lets a company send, receive, and manage money separately from personal funds, covering both domestic and international transactions. Knowing how to open a business payment account in the UK means understanding three things: who qualifies, what documents you need, and how the application process actually works. The Financial Services Compensation Scheme (FSCS) protects deposits up to £85,000 per business per authorized provider. That figure matters before you choose where to apply. This guide walks you through every stage, with specific attention to international transactions and the compliance steps that trip up most founders.

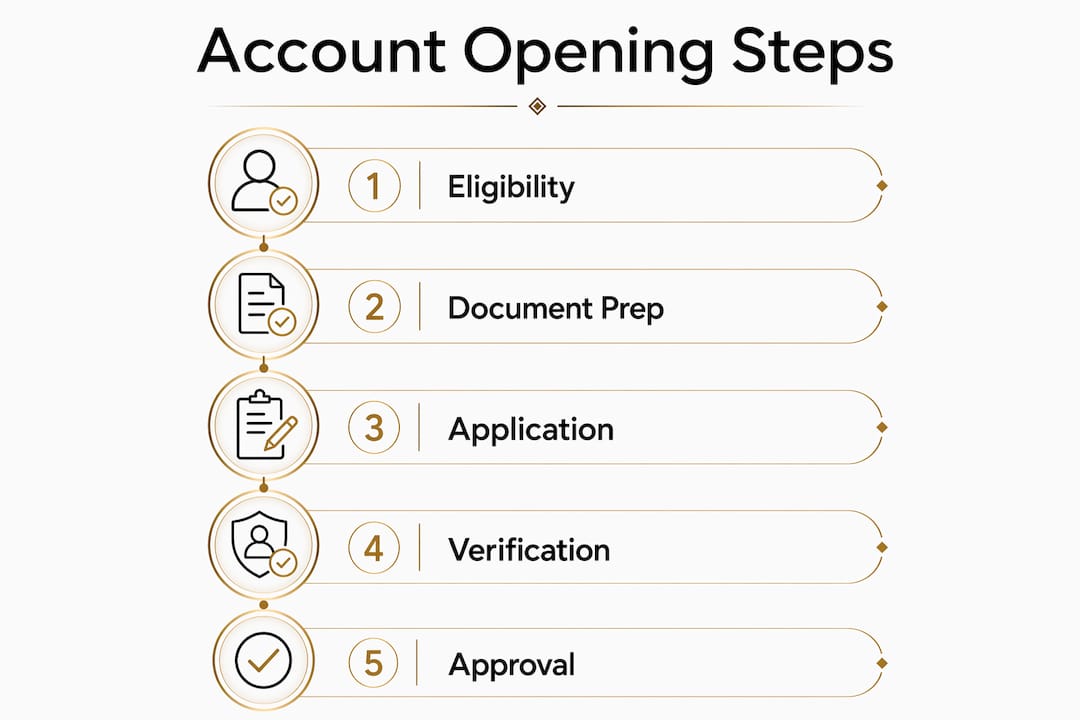

What does it take to open a business payment account in the UK?

Eligibility is the first gate. UK business account eligibility requires you to be 18 or older, a UK resident, and operating as a sole trader, director of a limited company, or partner in a partnership. Limited companies must be registered with Companies House before any bank will consider an application. If your business is based abroad, expect the process to take considerably longer.

The account opening process combines eligibility checks with comprehensive customer due diligence. Banks verify legal business status, ownership structure, and financial context before approving any account. This is not a formality. A business with overseas directors or complex shareholding will face more scrutiny than a straightforward UK sole trader.

Pro Tip: Check your Companies House registration is fully up to date, including the registered address and all director details, before you submit a single document to any bank.

What documents do you need to open a UK business account?

Preparation is the single biggest factor in how fast your account opens. Banks commonly require proof of identity and address, your legal business name, trading start date, a description of business activity, and financial details including turnover and any existing loans.

Limited companies must also provide Companies House documents and a Certificate of Incorporation. Every director on the account needs to supply personal ID and proof of address. For businesses with multiple directors or beneficial owners, this step multiplies quickly.

Here is a summary of what each business type typically needs to provide:

| Document | Sole Trader | Limited Company | Overseas Company |

|---|---|---|---|

| Proof of ID (passport or driving license) | Yes | All directors | All directors |

| Proof of address | Yes | All directors | All directors |

| Certificate of Incorporation | No | Yes | Yes (UK-registered) |

| Companies House filing | No | Yes | Yes |

| Business plan | Sometimes | Sometimes | Yes |

| Turnover and financial history | Yes | Yes | Yes |

| UK-based representative | No | No | Yes |

Overseas companies face the most demanding requirements. Banks require UK company registration, a UK business plan explaining why a UK account is needed, and a UK-based representative authorized to sign the bank mandate. This is not optional. Missing any one of these items stops the application entirely.

Pro Tip: Prepare a one-page summary of your business model, expected transaction volumes, and the countries you trade with. Banks ask for this information anyway. Having it ready signals professionalism and cuts back-and-forth by days.

For a full document checklist organized by business type, the 2026 application checklist covers both UK and international structures in detail.

How do you apply for a UK business payment account, step by step?

The application process has two distinct phases: submission and verification. Opening times vary from days to months depending on documentation readiness and business complexity. Your account is not operational until it is fully funded and activated, not just applied for.

Follow these steps to move through the process efficiently:

- Choose the right account type. Decide between a traditional bank account, a payment institution account, or a specialist B2B platform like Sigmaplatinum. Each has different protection models, fee structures, and onboarding timelines.

- Gather all documents before you start. Incomplete applications are the leading cause of delays. Have every director's ID, proof of address, and company documents ready before you open the application form.

- Complete the application and upload documents. Most providers now accept digital uploads. Scan documents clearly and label files by director name and document type.

- Pass identity and business verification. Banks run Know Your Business (KYB) checks, credit checks, and AML screening. This stage can involve follow-up questions about your business activity and expected payment flows.

- Respond to any additional requests promptly. Slow responses to bank queries are the second most common cause of delays. Set a daily reminder to check for messages during the review period.

- Fund the account and confirm activation. Account operational timelines depend on when the account is funded and fully active, not the submission date. Transfer the minimum opening deposit as soon as the account is approved.

For overseas companies, add two extra steps: appointing a UK-based representative and submitting a business plan that explains your UK trading rationale. These steps add time but are non-negotiable.

| Business type | Typical opening timeline |

|---|---|

| UK sole trader | 1–5 business days |

| UK limited company | 3–10 business days |

| Overseas company | 4–12 weeks |

| Complex ownership structure | 6–16 weeks |

Pro Tip: Ask your provider upfront which team handles overseas or complex applications. Routing your case to the right team from day one can cut weeks off the timeline.

What causes delays, and how do you avoid them?

Delays in UK business account applications follow a predictable pattern. Incomplete or inconsistent documentation is the top cause, followed by enhanced due diligence triggered by overseas ownership, unusual business profiles, or missing source-of-funds explanations.

Enhanced verification for overseas-owned accounts triggers manual reviews that add significant time compared to simple UK-only structures. Banks are not being obstructive. They are meeting their legal obligations under Anti-Money Laundering (AML) regulations.

The most common pitfalls to avoid:

- Mismatched information across documents (for example, different addresses on ID versus Companies House records)

- Missing beneficial owner details for shareholders holding more than 25% of the company

- No explanation of expected transaction volumes, currencies, or counterparty countries

- Vague business descriptions that do not clearly explain what the company does and how it earns revenue

- Failure to explain the source of startup capital or initial deposits

"Banks assess not only company legitimacy but also payment flow patterns to ensure compliance with AML regulations and risk controls." Prepare a clear written summary of who you pay, who pays you, in which currencies, and at what frequency.

Prepare ownership charts and verify all directors' and beneficial owners' identity documents before applying. This single step removes the most common friction point in complex applications.

Pro Tip: If your business has investors or parent companies in multiple countries, draw a simple ownership diagram showing the full chain of control. Banks will ask for this. Providing it upfront removes a common reason for extended review.

How do you use your UK business account for international transactions?

A UK business payment account built for international use needs specific capabilities. UK business accounts typically support Faster Payments, CHAPS, BACS, and international wire transfers, with features for dual authorization controls and integration with accounting software like Xero.

Understanding fund protection is critical before you commit to any provider. The FSCS covers deposits up to £85,000 at authorized banks. Payment institutions and e-money firms operate under a different model called safeguarding, where client funds are held separately but not covered by FSCS. Safeguarding reforms effective may 2026 will change how these protections work, so confirm the current framework with your chosen provider.

For businesses running multi-currency operations, the multi-currency account setup guide covers the eligibility and documentation steps specific to holding and transacting in foreign currencies.

Key practices for managing international payments effectively:

- Document the source of funds for every large inbound transfer before it arrives, not after

- Maintain records of contracts, invoices, and counterparty details for AML compliance

- Use dual authorization for high-value outbound transfers to reduce fraud risk

- Connect your account to accounting software to automate reconciliation across currencies

- Review your account's foreign exchange fee structure before committing to a provider, since FX margins vary widely

Banks assess payment flow patterns as part of ongoing AML compliance, not just at account opening. Keeping clean, consistent records protects you from account restrictions later.

Key Takeaways

Opening a UK business payment account requires meeting eligibility criteria, preparing complete documentation, and actively managing the verification process to avoid delays.

| Point | Details |

|---|---|

| Eligibility comes first | You must be 18+, UK-resident, and registered with Companies House before applying. |

| Documents determine speed | Incomplete or inconsistent paperwork is the leading cause of application delays. |

| Overseas companies face extra steps | A UK representative, UK registration, and a business plan are all required. |

| FSCS covers up to £85,000 | Confirm whether your provider is a bank or payment institution before depositing funds. |

| International use needs planning | Document transaction flows, source of funds, and counterparty details from day one. |

What I've learned about UK business account applications the hard way

Most founders treat the bank application as a box-ticking exercise. That is the wrong frame. Banks are making a risk decision about your business, and the documentation you submit is your argument for why you are a low-risk client.

The businesses I have seen get approved fastest are not the ones with the cleanest balance sheets. They are the ones who explain themselves clearly. A consulting firm with clients in five countries and variable monthly revenue is not inherently risky. But if the bank cannot understand the business model from the documents alone, it will treat the application as high risk by default.

Patience matters more than most founders expect. Complex structures with overseas ownership genuinely take weeks, sometimes months. Fighting the timeline rarely helps. Responding quickly to every bank query, providing more detail than asked for, and staying consistent across every document is what actually moves things forward.

The other thing founders consistently underestimate is the importance of the transaction flow narrative. Banks want to know who sends you money, why, from where, and how often. Writing a clear one-page summary of your expected payment flows before you apply is the single highest-return preparation step I know of.

— Ahmed

Sigmaplatinum: built for international business account access

Founders running cross-border operations often find that traditional banks are not built for their complexity. Sigmaplatinum addresses that gap directly.

Sigmaplatinum is a B2B fintech platform that provides business payment account access for international companies operating in the UK. The platform uses a compliance-focused onboarding process with KYB checks and partner evaluations built in, so you are not navigating those requirements alone. Multi-currency transactions, FX workflows, and corporate payment tools are available through regulated partners. Digital agencies, consulting firms, and import/export companies use Sigmaplatinum to manage payment operations without the friction of traditional bank onboarding. Check your eligibility and start your application at Sigmaplatinum.

FAQ

Who is eligible to open a UK business payment account?

You must be 18 or older, a UK resident, and operating as a sole trader, limited company director, or partnership member. Limited companies must be registered with Companies House before applying.

How long does it take to open a UK business bank account?

Timelines range from one business day for simple sole trader applications to several months for overseas-owned companies with complex structures. The account is not operational until it is funded and fully activated.

What documents do I need to open a business account in the UK?

You need proof of identity and address for all directors, your Certificate of Incorporation, Companies House documents, and a description of your business activity and expected turnover. Overseas companies also need a UK-registered address and a UK-based representative.

Are my funds protected in a UK business payment account?

Deposits at authorized banks are protected up to £85,000 per business under the FSCS. Payment institutions use a safeguarding model instead, which works differently and is subject to regulatory reform in 2026.

Can an overseas company open a UK business payment account?

Yes, but the requirements are more demanding. Overseas companies need UK registration, a UK business plan, contact with inward investment teams, and a UK-based representative authorized to sign the bank mandate.