A multi-currency payment account is a single financial account that lets businesses receive, hold, convert, and send funds in more than one currency without opening separate bank accounts in each country. Understanding how multi-currency payment accounts function is the first step toward cutting FX costs and gaining real control over cross-border cash flow. These accounts have become the operational backbone for importers, exporters, digital agencies, and consulting firms that deal with clients or suppliers across multiple markets. The industry term for the underlying infrastructure is a "multi-currency business payment account," and it operates through local payment rails, FX conversion engines, and API-connected reporting tools.

How do multi-currency payment accounts function?

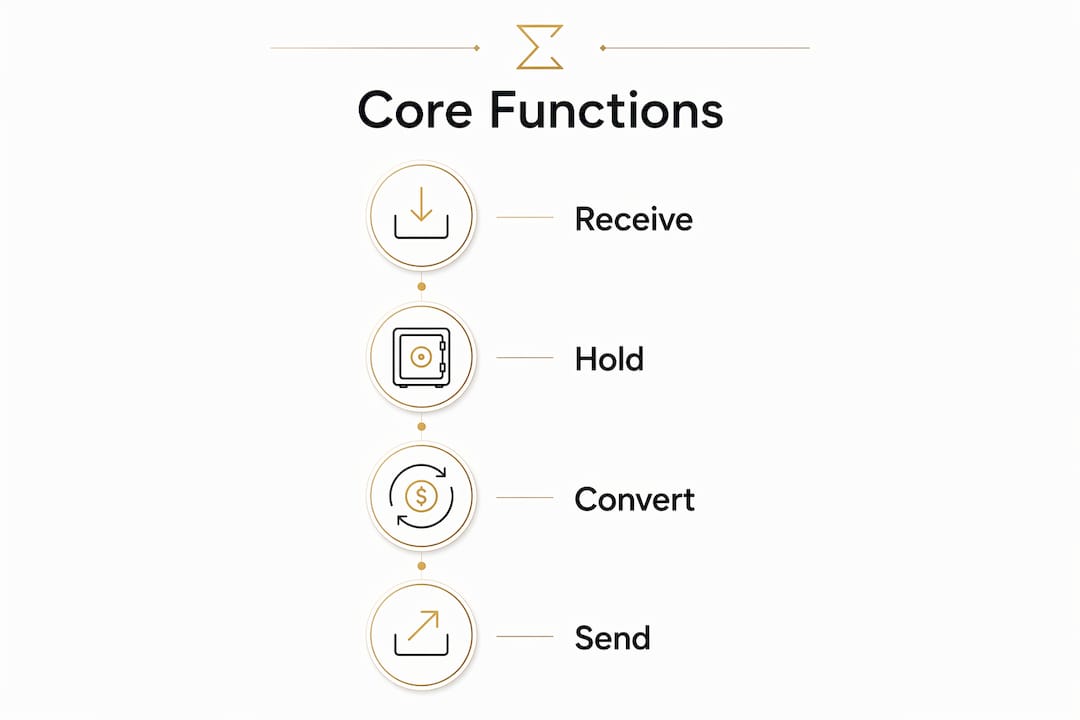

Multi-currency accounts work by giving your business a single platform that handles four core tasks: receiving, holding, converting, and sending funds across currencies.

Receiving payments in local currencies

Providers issue local banking details across multiple countries, including IBANs for European markets and routing numbers for US transactions. This means a client in Germany pays you via a local EUR bank transfer, and a client in the US pays via ACH, with both payments landing in your single account. You avoid the friction of asking overseas clients to wire funds internationally, which reduces payment delays and abandoned invoices. Some platforms now also issue stablecoin deposit addresses, giving you a third rail for receiving digital asset payments.

Holding balances in multiple currencies

Balances in various currencies sit side by side within one interface, so you can see your USD, GBP, and EUR positions at a glance. You decide when to convert each balance, rather than having the platform auto-convert on receipt. This control is the core advantage over a standard business checking account, which forces conversion at the moment of deposit. Leading providers support 25 or more major currencies on a single platform.

Converting currencies at the right moment

Multi-currency accounts let you time FX conversions strategically rather than converting reactively when a payment arrives. Finance leaders treat this as a margin protection tool. If the EUR/USD rate moves in your favor over a two-week period, you convert then, not the day the invoice was paid. Rates are typically tied to interbank or mid-market benchmarks, which are materially better than the retail rates traditional banks charge.

Sending payments abroad

Local payment networks and stablecoin rails enable near-instant settlement of international payments, bypassing the SWIFT network's fees and multi-day delays. Modern accounts operate across 75+ countries and 60+ currencies. Sending a payment to a supplier in Singapore costs the same as a domestic transfer, because the platform routes through Singapore's local network rather than an international correspondent bank chain.

Pro Tip: Set up named sub-accounts for each major currency you transact in. This keeps your reporting clean and makes reconciliation far faster at month end.

What are the key advantages of multi-currency accounts?

The financial benefits of multi-currency accounts go well beyond avoiding a few wire transfer fees. The structural advantages reshape how you manage cash across borders.

-

Elimination of foreign transaction fees. Traditional banks charge 1%–3% on every cross-border conversion. A multi-currency account routes payments through local networks, so that fee disappears on most transactions.

-

Strategic FX timing. Pre-funding balances and managing FX exposure proactively, rather than converting reactively, protects profit margins against currency volatility. A consulting firm billing €50,000 per month to European clients can hold EUR until the rate is favorable, then convert to USD in a single transaction.

-

Liquidity consolidation. Centralizing multi-currency funds in one account eliminates the "trapped cash" problem. Businesses that maintain separate local accounts in five countries often find capital locked in accounts with minimum balance requirements or slow transfer windows. One consolidated account moves capital freely.

-

Faster settlement. Stablecoin and local payment network integration cuts settlement from three to five business days down to hours or minutes. For businesses with tight supplier payment terms, faster settlement is a direct competitive advantage.

-

Reduced administrative overhead. Managing one account instead of five means one set of statements, one reconciliation process, and one compliance relationship. Finance teams recover hours every week.

The multi-currency liquidity benefits here are most visible for businesses with monthly cross-border payment volumes above $50,000, where even a 0.5% improvement in FX rates produces meaningful annual savings.

How does technology make multi-currency accounts more powerful?

The operational gap between a modern multi-currency account and a traditional bank account is widest in the technology layer. Automation and integration are what turn a currency-holding tool into a full treasury management system.

API integration with ERP and accounting software

API connectivity with ERP systems and automated reconciliation distinguish multi-currency accounts from fragmented legacy bank management. When your account connects to QuickBooks, Xero, or NetSuite via API, every incoming and outgoing payment posts automatically to the correct ledger entry. Automation reduces manual effort and errors in payment matching and reporting. Finance teams stop spending Monday mornings reconciling weekend transactions by hand.

Real-time reporting and unified cash visibility

A real-time dashboard shows your global cash position across all currencies in one view. You can see that you hold $120,000 USD, €45,000 EUR, and £30,000 GBP without logging into three separate banking portals. This unified view is the foundation for accurate cash flow forecasting. Without it, treasury decisions are based on incomplete data.

Sub-accounts and webhooks for payment matching

Sub-accounts and webhooks allow precise order-to-payment matching. Each customer or project gets a unique sub-account or virtual account number. When payment arrives, a webhook fires and tags the transaction to the correct invoice automatically. This eliminates the "unidentified payment" problem that plagues businesses receiving high volumes of international transfers.

The table below compares the technology capabilities of modern multi-currency accounts against traditional fragmented bank account management.

| Capability | Multi-currency account | Traditional bank accounts |

|---|---|---|

| Reconciliation | Automated via API and webhooks | Manual, statement-based |

| Cash visibility | Real-time, unified dashboard | Fragmented across portals |

| Payment matching | Sub-account and webhook tagging | Manual reference matching |

| ERP integration | Native API connectors | Limited or unavailable |

| Settlement speed | Hours via local rails | 3–5 business days via SWIFT |

Pro Tip: Before choosing a platform, confirm it offers a webhook-based notification system. Without webhooks, automated reconciliation breaks down the moment payment volumes scale.

Who benefits most from multi-currency payment accounts?

Not every business needs a multi-currency account, but the profile of businesses that do is broader than most owners realize. If you transact in more than one currency more than a few times per month, the math almost always favors a dedicated account.

The businesses that gain the most include:

- Exporters and importers who invoice or pay suppliers in foreign currencies and currently absorb bank FX margins on every transaction.

- Digital agencies and SaaS companies with international client bases billing in USD, EUR, or GBP simultaneously.

- Consulting firms that staff projects across multiple countries and need to pay contractors in local currencies without expensive wire fees.

- Import/export companies managing supplier payments in Asia while collecting receivables in Europe or North America.

The impact on international business growth is clearest when you look at FX cost savings compounded over a full year. A business converting $500,000 in foreign currency annually at a 2% bank margin pays $10,000 in hidden fees. A multi-currency account with mid-market rates and local rails cuts that figure dramatically.

Strategic FX management also affects competitiveness. A business that can quote prices in a client's local currency, collect in that currency, and hold the balance until conversion is favorable, wins deals that a competitor quoting only in USD will lose. The setup process for multi-currency B2B accounts is more accessible than most business owners expect, particularly on platforms built for international operations from the ground up.

Key Takeaways

Multi-currency payment accounts reduce cross-border costs and give businesses direct control over FX timing, liquidity, and payment reconciliation within a single platform.

| Point | Details |

|---|---|

| Core function | One account receives, holds, converts, and sends funds in 25+ currencies. |

| FX timing control | Holding balances and converting strategically protects profit margins against rate swings. |

| Liquidity consolidation | Centralizing funds eliminates trapped cash and frees capital locked in multiple local accounts. |

| Technology advantage | API integration and webhooks automate reconciliation and eliminate manual payment matching. |

| Best-fit businesses | Exporters, importers, agencies, and consultants with recurring cross-border payment volumes benefit most. |

The shift I've watched happen in cross-border finance

I've spent years watching businesses manage international payments the hard way. They open a local bank account in Germany, another in Singapore, and a third in the UK. Each account has its own login, its own statement cycle, and its own minimum balance requirement. The CFO spends two days every month reconciling across three portals and still misses payments.

The shift to multi-currency accounts is not just a cost story. It's a control story. The businesses I've seen adopt these platforms don't just save money on FX. They make better treasury decisions because they finally have accurate, real-time data. They stop converting currencies out of panic when a payment arrives and start converting when the rate actually makes sense.

The trend I find most significant is stablecoin integration. A few years ago, stablecoin deposit addresses were a niche feature. Now they're a practical third rail for businesses with counterparties in markets where traditional banking is slow or expensive. That's a structural change in how international payments work, and it's happening faster than most traditional finance teams realize.

My advice to any business owner still running cross-border payments through a standard bank account: the cost you see on the wire fee receipt is not the full cost. The hidden FX margin, the reconciliation hours, and the trapped cash in foreign accounts add up to a number that would make most finance directors uncomfortable. A purpose-built multi-currency account solves all three.

— Ahmed

Sigmaplatinum: built for international business payments

Sigmaplatinum is a B2B fintech platform designed specifically for businesses that operate across borders. It gives you access to multi-currency business payment accounts that support receiving, holding, converting, and sending funds across major currencies, with compliance-focused onboarding that includes rigorous KYB checks.

The platform connects to regulated partners and supports FX workflows, corporate financial tools, and a no-code setup model that gets your account operational without technical complexity. Digital agencies, consulting firms, and import/export companies use Sigmaplatinum to cut FX costs and manage cross-border payments from a single interface. If your business handles international transactions regularly, Sigmaplatinum is worth a direct look.

FAQ

What is a multi-currency payment account?

A multi-currency payment account is a single financial account that lets businesses receive, hold, convert, and send funds in multiple currencies. Leading platforms support 25 or more currencies within one interface.

How do multi-currency accounts reduce costs?

They route payments through local payment networks instead of SWIFT, eliminating international wire fees and offering mid-market FX rates instead of the retail margins traditional banks charge.

Can I control when my currencies get converted?

Yes. Multi-currency accounts hold each currency balance separately, so you decide when to convert. This lets you time conversions to protect margins when exchange rates move in your favor.

What technology integrations do multi-currency accounts support?

Most modern platforms offer API-based ERP integration with systems like QuickBooks, Xero, and NetSuite, plus webhooks for automated payment matching and real-time reporting dashboards.

Which businesses benefit most from multi-currency accounts?

Exporters, importers, digital agencies, SaaS companies, and consulting firms with recurring cross-border payments gain the most. The financial case strengthens as monthly foreign currency transaction volumes increase.