Cross-border remittance is defined as the transfer of money across national borders from one person or business to another, typically involving currency conversion and regulatory compliance. The term "remittance" has a specific meaning in international finance: it refers to a sender-initiated payment that crosses jurisdictions, whether for family support, overseas supplier payments, or charitable giving. Understanding what cross-border remittance means matters because the process differs significantly from a domestic bank transfer. Banks, licensed money transfer services, and digital wallets each handle these flows differently, and the costs, speed, and compliance requirements vary by corridor and provider.

What does cross-border remittance mean in practice?

Cross-border remittance is a purpose-driven payment sent across national borders, most commonly used for family support, overseas bill payments, or business transactions. The industry term you will encounter most often is "international remittance," though "cross-border remittance" and "cross-border money transfer" are used interchangeably in fintech and banking contexts. What separates remittances from general bank wires is the intent and workflow. A remittance is always sender-initiated, it crosses at least one national border, and it typically requires currency conversion and compliance checks that a domestic transfer does not.

Remittances are a specific subset of cross-border payments. Remittances are characterized by sender-initiated workflows, multi-jurisdiction settlement, and compliance requirements that span two or more regulatory environments. A business paying a foreign supplier and a worker sending wages home to the Philippines are both executing cross-border remittances, even though the scale and documentation requirements differ substantially.

How does the remittance process work from start to finish?

The remittance process follows a clear sequence, though the details vary by provider and destination corridor.

- Sender initiates the transfer. The sender provides recipient details, the amount, and the destination currency through a bank, a licensed money service business, or a digital platform.

- Identity and compliance checks run. The provider performs identity verification, anti-money laundering (AML) screening, and sanctions checks. These compliance steps are required whenever a transfer crosses jurisdictions to prevent fraud and money laundering.

- Currency conversion occurs. If the sending and receiving currencies differ, the provider converts funds at a rate that includes a margin. This margin is one of the primary cost drivers.

- Routing through payment networks. Funds move through intermediary banks or payment networks. Cross-border payments involve multiple intermediaries, including banks, payment providers, and networks, which adds layers of complexity compared to domestic transfers.

- Final delivery to the recipient. The recipient receives funds via bank deposit, mobile wallet credit, or cash pickup, depending on what the destination corridor supports.

The corridor matters more than most senders realize. A transfer from the United States to Mexico moves through well-established rails with fast settlement. A transfer to a smaller market in sub-Saharan Africa may involve additional correspondent banks and longer clearing times.

Pro Tip: Always confirm the payout method available at the destination before initiating a transfer. A recipient without a bank account cannot receive a bank deposit, and not every provider offers mobile wallet or cash pickup in every country.

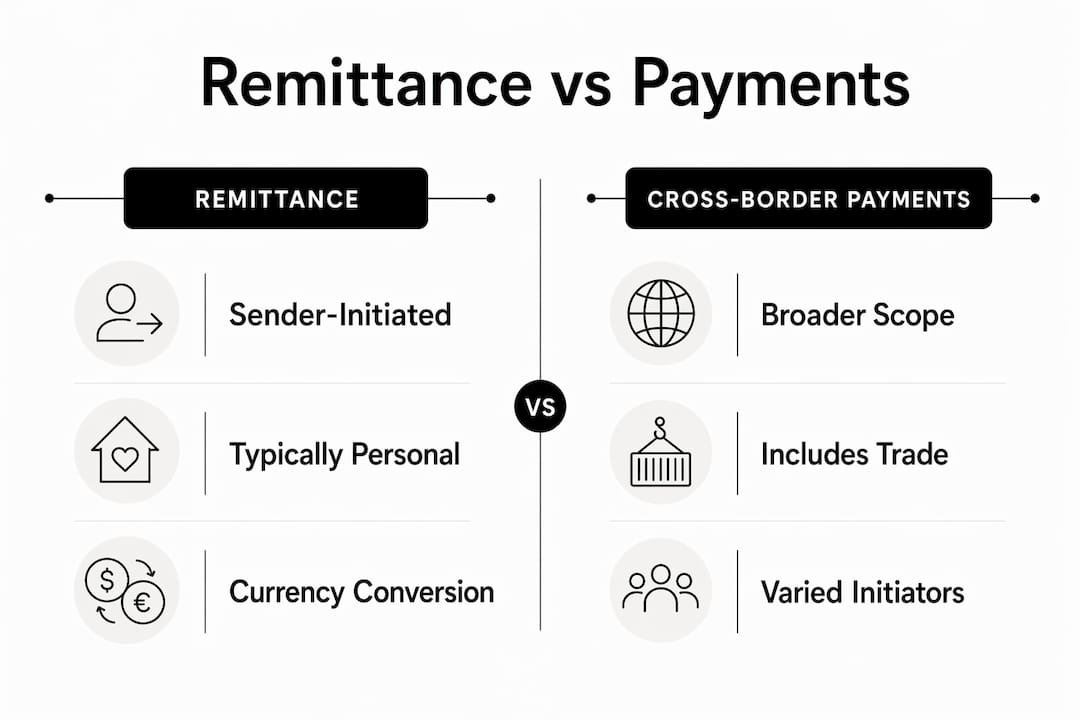

What are the key differences between remittance and cross-border payments?

The terms "remittance" and "cross-border payment" are often used as synonyms, but they describe different scopes of activity.

Cross-border payments is the broader category. It covers every financial flow that crosses a national border: trade finance, tourism spending, corporate treasury transfers, and remittances. Remittances are a subset of that category, defined by their sender-initiated, person-to-person or person-to-business structure.

| Feature | Cross-border remittance | General cross-border payment |

|---|---|---|

| Initiator | Individual or business sender | Any party, including automated systems |

| Primary purpose | Family support, supplier payment, personal obligation | Trade, tourism, corporate treasury, investment |

| Compliance focus | AML, identity verification, sanctions screening | Varies by type; trade finance adds customs and tax layers |

| Typical providers | Banks, money transfer operators, digital wallets | Banks, card networks, payment processors |

| Settlement speed | Minutes to 2 business days | Minutes to several business days |

The practical implication for businesses is this: if you are paying an overseas supplier or contractor, you are executing a cross-border remittance, not just a "wire transfer." That distinction affects which compliance rules apply, which providers can serve you, and what documentation you need to keep.

Key differences that affect your choice of provider:

- Remittances require explicit sender and recipient identity data at every step.

- General cross-border payments may route through automated clearing houses without individual identity checks.

- Business remittances require structured reference fields for reconciliation, which personal transfers do not.

What costs and challenges should you expect?

Cross-border remittance costs come from three sources: transfer fees, currency conversion margins, and intermediary bank charges. Transfer fees are the most visible. Currency conversion margins are often larger than the stated fee but less obvious because they are embedded in the exchange rate. Intermediary bank charges appear when a payment routes through correspondent banks, and they can be deducted from the principal before the recipient receives funds.

Regulatory complexity adds another layer of cost. Capital controls and local regulatory environments at the destination can delay the final leg of a payment. Research from the IMF shows a 4–8 hour delay at the beneficiary leg associated with financial account restrictions, especially in emerging markets. That delay is not a provider failure. It is a structural feature of markets with capital controls, and no amount of technology on the sending side eliminates it.

Common cost and challenge factors to watch:

- FX margin: Compare the mid-market rate to the rate your provider offers. A 2% margin on a $50,000 transfer costs $1,000.

- Correspondent bank fees: Ask whether fees are deducted from the principal (SHA or BEN charging) or paid by the sender (OUR charging).

- Compliance holds: Unusual transfer amounts or new recipient relationships can trigger manual review, adding 24–48 hours.

- Last-mile restrictions: Destinations with capital controls or limited banking infrastructure create delays that are outside any provider's control.

Pro Tip: For recurring business payments, set up a pre-approved beneficiary list with your provider. Pre-verified recipients clear compliance checks faster and reduce the risk of holds on time-sensitive payments.

What technologies are improving cross-border remittance efficiency?

The biggest structural improvement in cross-border remittance infrastructure is the adoption of ISO 20022. ISO 20022 is a harmonized messaging standard that enables more consistent, structured data in cross-border payments, improving interoperability and processing efficiency. It reduces data fragmentation, enables straight-through processing, and supports the transmission of compliance data alongside payment instructions. Widespread adoption of ISO 20022 is crucial to reduce fragmentation across global payment networks.

Beyond messaging standards, digital platforms are changing how funds reach recipients. Modern digital platforms enable near real-time settlement of remittances, expanding payout options to include mobile wallets and instant card crediting. This matters most in underbanked regions where traditional bank accounts are rare but mobile phone penetration is high.

Current technology improvements shaping the space:

- Mobile wallet payouts: Recipients in markets like Kenya, India, and the Philippines can receive funds directly to M-Pesa, Paytm, or GCash without a bank account.

- Instant card crediting: Some providers credit Visa or Mastercard debit cards within minutes of transfer initiation.

- AML automation: Machine learning models screen transactions against sanctions lists and behavioral patterns faster and more accurately than manual review.

- Fraud detection: Real-time behavioral analytics flag anomalous transfer patterns before funds leave the sending institution.

| Technology | Primary benefit | Impact on remittance |

|---|---|---|

| ISO 20022 messaging | Structured, interoperable data | Faster straight-through processing |

| Mobile wallet integration | Reaches unbanked recipients | Expands delivery options in emerging markets |

| AML automation | Faster compliance screening | Reduces manual review delays |

| Instant card crediting | Near real-time delivery | Improves recipient experience |

For businesses managing cross-border payment infrastructure, understanding which technologies your provider uses directly affects how fast and reliably your payments arrive.

How do individuals and businesses use cross-border remittance effectively?

The use cases for cross-border remittance split clearly between personal and business contexts, and the requirements for each differ.

Personal senders typically send funds to family members abroad for living expenses, education, or medical costs. The documentation requirements are minimal: a government-issued ID and the recipient's account or wallet details. Speed and low fees are the primary selection criteria.

Business senders face a more structured process.

- Identify the payment purpose. Supplier payment, contractor fee, and intercompany transfer each carry different compliance and documentation requirements.

- Gather recipient data. Businesses require structured recipient data and reference fields for reconciliation and regulatory compliance. A missing IBAN or incorrect SWIFT code delays settlement.

- Attach supporting documentation. Invoices, contracts, or purchase orders may be required by the provider or the destination country's central bank.

- Confirm payout method compatibility. Not every destination supports bank-to-bank transfers. Some markets require local payment network routing.

- Reconcile after settlement. Match the amount received against the invoice using the reference fields included in the payment instruction.

Beneficiary-side delays often arise from account validation requirements or regulatory holds at the destination bank. The best mitigation is accurate data at the point of initiation. A wrong digit in an account number does not just slow the payment. It can trigger a return, which adds fees and days to the process.

For businesses managing multiple international payees, a multi-currency account reduces the number of individual conversions and simplifies reconciliation. Holding balances in destination currencies means you convert on your schedule, not under time pressure when a payment is due.

Key Takeaways

Cross-border remittance is a sender-initiated international transfer that requires currency conversion, compliance checks, and corridor-specific routing to deliver funds reliably across national borders.

| Point | Details |

|---|---|

| Core definition | Cross-border remittance is a sender-initiated payment crossing national borders, distinct from general wire transfers. |

| Process sequence | Every transfer follows initiation, compliance screening, currency conversion, routing, and final delivery steps. |

| Cost drivers | FX margins, transfer fees, and correspondent bank charges each reduce the amount the recipient receives. |

| Last-mile delays | Capital controls in destination markets can add 4–8 hours to settlement, regardless of sending-side speed. |

| Technology impact | ISO 20022 adoption and mobile wallet payouts are the two biggest improvements to remittance efficiency in 2026. |

What I have learned from years of watching cross-border payments evolve

The most common mistake I see businesses make is treating cross-border remittance as a simple wire transfer with a currency conversion attached. It is not. The compliance layer is real, the last-mile problem is real, and the cost of getting recipient data wrong is real. A payment that bounces back from a destination bank does not just cost you the return fee. It costs you the trust of the supplier or contractor waiting on the other end.

The second mistake is ignoring the FX margin. Transfer fees are visible and easy to compare. The exchange rate margin is invisible unless you check it against the mid-market rate. On large or frequent transfers, that margin compounds into a significant annual cost. The businesses that manage this well hold balances in destination currencies and convert in advance when rates are favorable.

Technology has genuinely improved the experience. ISO 20022 adoption is making straight-through processing more common, and mobile wallet payouts have opened corridors that were previously difficult to serve reliably. But technology does not eliminate the need to understand the process. The businesses that use these tools best are the ones that understand what is happening at each step, not just the ones with the fastest interface.

My practical advice: map your most frequent payment corridors, understand the last-mile options in each, and choose a provider whose compliance infrastructure matches the complexity of your destinations. Cutting costs by using an underpowered provider in a complex corridor is a false economy.

— Ahmed

Sigmaplatinum: business payment accounts built for international operations

Sigmaplatinum is a B2B fintech platform built for international businesses that need more than a basic bank account. The platform provides business payment account access with multi-currency capabilities, FX workflows, and compliance-focused onboarding through regulated partners. Digital agencies, consulting firms, and import/export companies use Sigmaplatinum to manage cross-border payments without the friction of traditional banking. The KYB process is rigorous, which means the accounts that pass it are set up to handle complex international payment corridors reliably. For businesses looking at B2B cross-border payment setups with real operational demands, Sigmaplatinum is worth a close look.

FAQ

What does cross-border remittance mean?

Cross-border remittance is the transfer of money across national borders from one person or business to another, typically involving currency conversion and compliance checks. It is a sender-initiated payment that crosses at least one international jurisdiction.

How is remittance different from a regular bank transfer?

A remittance crosses national borders and requires identity verification, AML screening, and often currency conversion. A domestic bank transfer operates within a single regulatory environment and skips most of those steps.

What causes delays in cross-border remittance?

The most common causes are compliance holds during AML screening, incorrect recipient data, and capital controls at the destination. Research shows capital controls can add 4–8 hours to the beneficiary leg of a payment in emerging markets.

What is ISO 20022 and why does it matter for remittances?

ISO 20022 is a global financial messaging standard that structures payment data for interoperability across networks. Its adoption reduces processing errors, speeds up compliance screening, and enables straight-through settlement without manual intervention.

What documentation do businesses need for cross-border remittance?

Businesses typically need a government-issued ID, the recipient's full account details (IBAN or local equivalent, SWIFT/BIC code), and supporting documents such as invoices or contracts depending on the destination country's regulatory requirements.