A USD payment account is a financial account that lets entities outside the United States send, receive, and hold U.S. dollars through interconnected banking systems and payment networks. Understanding how USD payment accounts work globally is not optional for finance professionals managing cross-border operations. It is the foundation of every international transaction your business executes. Platforms like Modern Treasury now offer Global USD Accounts serving businesses in 90+ countries, with support for ACH, wire, RTP, FedNow, and stablecoin rails through a single API. The infrastructure behind these accounts runs on correspondent banking, SWIFT messaging, and a set of payment rails that each carry different speeds, costs, and settlement rules.

How USD payment accounts work globally: the core infrastructure

The global USD payment system runs on correspondent banking. This is the industry term for a network of bilateral relationships where banks hold accounts with each other to settle transactions in foreign currencies, including U.S. dollars.

When your business in Singapore pays a supplier in Germany in USD, neither bank likely holds a direct relationship with the other. Instead, each bank maintains a relationship with one or more U.S. correspondent banks. The correspondent banking chain uses specific SWIFT/BIC codes and dedicated accounts per currency to clear and settle each payment leg.

The accounts at the center of this system are called nostro and vostro accounts. A nostro account is your bank's account held at a foreign bank ("our money, held by you"). A vostro account is a foreign bank's account held at your bank ("your money, held by us"). These balances are the actual USD liquidity that moves between institutions without physically transferring funds end to end.

SWIFT is the messaging layer sitting on top of this structure. It does not move money. It sends payment instructions between banks using standardized message formats. As of november 2025, SWIFT migrated to ISO 20022 message formats, specifically pacs.008 and pacs.009, to improve data quality and reconciliation accuracy across the network.

Pro Tip: Every USD wire you send internationally carries a UETR, a Unique End-to-End Transaction Reference assigned by SWIFT gpi. Use it to track payment status in real time rather than waiting for bank confirmations.

- Correspondent banks hold nostro/vostro accounts to provide USD liquidity across borders.

- SWIFT transmits payment instructions, not funds.

- SWIFT gpi adds end-to-end tracking via UETR UUIDs.

- ISO 20022 migration (november 2025) improves data richness in pacs.008/pacs.009 messages.

- Each currency and settlement leg requires its own mapped correspondent route.

How do payment rails affect USD transaction speed and settlement?

The rail your USD payment travels on determines when funds actually settle. This is one of the most misunderstood aspects of international USD accounts, and it has direct consequences for cash flow management.

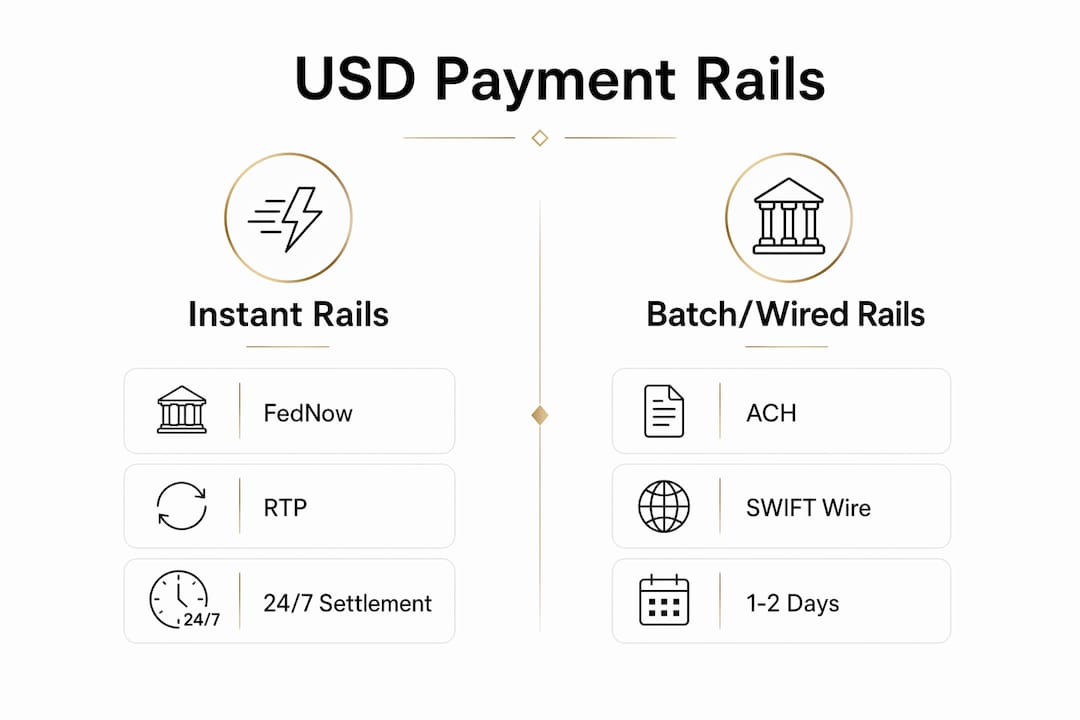

FedNow and RTP are instant payment rails operating 24/7/365 within the United States. Payments on these rails settle within seconds. That speed is a significant operational advantage for businesses that need same-day liquidity confirmation.

ACH payments are batch-processed and typically settle within one to two business days. Standard wire transfers through the Fedwire Funds Service settle on the same business day but only during operating hours. Cross-border wires routed through correspondent banks and SWIFT can take one to five business days, depending on the number of intermediary banks in the chain.

| Payment Rail | Settlement Speed | Availability | Best Use Case |

|---|---|---|---|

| FedNow | Seconds | 24/7/365 | Instant domestic USD payments |

| RTP | Seconds | 24/7/365 | Real-time B2B and consumer payments |

| ACH | 1–2 business days | Business hours | Recurring payroll, vendor payments |

| Fedwire | Same day | Business hours only | Large-value domestic wires |

| SWIFT/Correspondent | 1–5 business days | Varies by bank | International cross-border USD |

Pro Tip: If your business collects USD from international clients, specify FedNow or RTP as the preferred inbound rail when your provider supports it. You get confirmed funds faster and reduce the reconciliation lag that comes with correspondent-routed wires.

Understanding which rail your account uses is key to anticipating availability and payment finality. A platform that only supports ACH and SWIFT cannot give you the same cash flow certainty as one supporting FedNow and RTP alongside traditional rails.

What are the operational challenges of managing global USD accounts?

Managing international USD accounts at scale introduces costs and risks that are easy to underestimate. Cross-border USD payments often incur multiple fees, including correspondent bank lifting charges and FX spreads applied at each conversion point. These fees compound across a multi-hop correspondent chain and reduce the net amount received by your counterparty.

The correspondent banking chain is often overlooked but fundamentally shapes the speed, cost, and complexity of USD international payments. Businesses that do not map their correspondent routes in advance frequently encounter unexpected deductions and delayed settlements.

Operational risk is the other major concern. Reliance on a limited number of USD liquidity providers creates concentration risk. If a single provider experiences a disruption, both fiat rails and stablecoin on/off-ramps can be affected simultaneously. Redundancy at the architecture level is not optional for businesses processing significant USD volumes.

The ISO 20022 migration adds a technical layer to these challenges. New message fields in pacs.008 and pacs.009 require reconciliation systems to be tested and updated. Businesses that have not adapted their accounting workflows may encounter missing reference issues that create audit gaps.

Key operational considerations for finance teams managing global USD accounts:

- Map correspondent routes for each currency pair and settlement leg before going live.

- Audit all fee layers, including lifting fees, FX spreads, and intermediary charges.

- Build redundancy by maintaining relationships with at least two USD liquidity providers.

- Test reconciliation workflows against ISO 20022 pacs.008/pacs.009 message formats.

- Integrate stablecoin workflows as a parallel rail, not a replacement for fiat infrastructure.

How do modern global USD accounts change international transactions?

Modern platforms have restructured how businesses access USD payment infrastructure. Rather than requiring a physical U.S. bank account or a direct correspondent relationship, platforms like Modern Treasury now provide named, routable U.S. accounts to businesses in 90+ countries through a unified API.

These accounts carry real U.S. routing numbers and account numbers. A business in Brazil or the UAE can receive ACH and wire payments as if it held a domestic U.S. bank account. The same account can send payments via multiple rails, including RTP, FedNow, and stablecoin networks, without requiring separate accounts for each rail.

The programmable payment capabilities built into modern platforms change how finance teams operate. Payments can be triggered automatically based on ledger conditions, approval workflows, or external data events. A single ledger tracks all movements across rails, reducing the reconciliation burden that comes with managing multiple bank accounts across jurisdictions.

- Named U.S. accounts: Businesses receive real routing and account numbers usable for ACH and wire collection globally.

- Multi-rail sending: A single account supports ACH, wire, RTP, FedNow, and stablecoin disbursements.

- Embedded compliance: Identity verification and KYB checks are built into onboarding, not bolted on afterward.

- Programmable payments: Payment triggers based on ledger events reduce manual processing and errors.

- FDIC pass-through insurance: Funds held through regulated partner banks qualify for FDIC pass-through coverage.

"The shift from managing multiple correspondent accounts to operating a single programmatic USD account is the most significant operational change in cross-border finance since SWIFT gpi launched."

For businesses managing B2B cross-border payment setups, this architecture eliminates the need to open local accounts in each market while maintaining full USD transaction capability. The compliance layer, including KYB verification and sanctions screening, runs within the platform rather than requiring separate legal and banking arrangements in each country.

Key Takeaways

USD payment accounts work globally through a combination of correspondent banking relationships, SWIFT messaging, and payment rails that each carry distinct speed and cost profiles.

| Point | Details |

|---|---|

| Correspondent banking is the foundation | Nostro/vostro accounts hold USD liquidity across banks without moving funds end to end. |

| SWIFT sends instructions, not money | SWIFT gpi and ISO 20022 improve tracking and data quality but do not replace correspondent infrastructure. |

| Rail choice determines settlement speed | FedNow and RTP settle in seconds; SWIFT-routed wires take 1–5 business days. |

| Operational risk requires redundancy | Concentration in one USD liquidity provider creates failure risk across both fiat and stablecoin rails. |

| Modern platforms simplify access | Named U.S. accounts with multi-rail support give global businesses domestic USD capabilities without local banking. |

What I have learned managing USD accounts across borders

After working with finance teams across digital agencies, import/export companies, and consulting firms, the pattern I see most often is this: businesses underestimate how much the correspondent chain costs them until they actually map it. A payment that looks like a $15 wire fee at the sending bank can arrive $45 lighter after two intermediary banks take their lifting charges. That gap shows up in reconciliation as a mystery deduction, and it erodes supplier trust fast.

My strongest advice is to treat your USD liquidity provider selection as a risk decision, not just a pricing decision. I have seen businesses grind to a halt because their single provider had a technical outage during a critical payment window. The operational risk in USD treasury for non-U.S. businesses is real, and it is underweighted in most treasury policies.

On the technology side, the ISO 20022 migration is not just a compliance checkbox. The richer data in pacs.008 messages gives your reconciliation team actual reference fields to match against. Businesses that have updated their systems to use SWIFT gpi tracking are resolving payment queries in hours instead of days. That is a genuine operational gain.

My view on stablecoins is practical rather than ideological. They work well as a parallel rail for corridors where correspondent banking is slow or expensive. They do not replace the need for a well-structured fiat USD account. Build the fiat foundation first, then layer stablecoin capability on top where the economics justify it.

— Ahmed

Sigmaplatinum and global USD payment account access

Sigmaplatinum is a B2B fintech platform built specifically for international businesses that need efficient USD payment workflows without the overhead of traditional banking arrangements.

Sigmaplatinum provides access to business payment account solutions designed for digital agencies, consulting firms, and import/export companies operating across borders. The platform supports multi-currency transactions, FX workflows, and multi-rail payment capabilities through regulated partners. Onboarding includes rigorous KYB checks and partner evaluations, so compliance is embedded from day one rather than managed separately. For businesses that need reliable USD account access without building their own correspondent banking relationships, Sigmaplatinum offers a direct path to cross-border payment infrastructure that is already structured for international operations.

FAQ

What is a USD payment account used for internationally?

A USD payment account lets businesses outside the United States send, receive, and hold U.S. dollars through correspondent banking networks and payment rails like ACH, wire, FedNow, and RTP.

How does SWIFT fit into USD international payments?

SWIFT is a messaging network that transmits payment instructions between banks. It does not transfer funds directly. Actual USD movement happens through correspondent bank nostro and vostro account balances.

What is the difference between FedNow and a SWIFT wire?

FedNow settles payments within seconds on a 24/7/365 basis inside the U.S. A SWIFT wire routed through correspondent banks typically takes 1–5 business days and incurs multiple intermediary fees.

Why do cross-border USD payments sometimes arrive short?

Correspondent banks along the payment chain deduct lifting fees at each hop. FX spreads applied during currency conversion add further reductions. Mapping your correspondent route in advance helps you anticipate and account for these deductions.

What is ISO 20022 and why does it matter for USD accounts?

ISO 20022 is the new message format standard for SWIFT payments, adopted in november 2025. It carries richer payment data, including UETR tracking references, which improves reconciliation accuracy and audit capability for USD transactions.