A multi-currency account is a business banking solution that lets exporters hold, receive, send, and convert multiple currencies from a single platform, making export business multi-currency account access the most direct way to cut FX costs and speed up cross-border payments. Traditional bank accounts force you to convert every incoming payment into your domestic currency, triggering conversion fees on both ends. Multi-currency accounts eliminate that double conversion by keeping funds in their original currency until you need them. Platforms like TerraTrade and Embat have built their entire product around this model, and the operational difference for exporters is significant.

What do exporters need to access a multi-currency account?

Export business multi-currency account access starts with meeting a provider's compliance and documentation requirements. Every regulated provider runs Know Your Business (KYB) checks before activating an account. The process is digital at most modern platforms, but the documentation requirements are consistent across the board.

You will typically need to provide:

- Certificate of incorporation and company registration documents

- Proof of business activity, such as trade invoices or contracts with overseas buyers

- Beneficial ownership information for all directors and shareholders above a threshold (usually 25%)

- Bank statements covering at least three to six months of business activity

- Compliance declarations confirming the nature of your international trade flows

Beyond documentation, you need to choose a provider whose currency coverage matches your trade corridors. Multi-currency account features from TerraTrade include wallets for USD, SGD, HKD, and EUR, with invoice proceeds landing automatically in the correct wallet. Embat's global banking platform supports 60+ currencies and executes payments in 150+ countries. The right choice depends on which markets you export to most.

Integration capability is the third requirement most exporters overlook. If you use an ERP system like SAP, Oracle NetSuite, or Microsoft Dynamics, confirm that your chosen provider offers a direct API connection or a compatible integration layer. Accounts that connect to your trade finance facility can automate the entire receivables flow, from invoice issuance to payment landing.

Pro Tip: Before applying, map every currency you receive and every currency you pay suppliers in. Providers charge differently for currencies outside their core network, and a mismatch between your trade corridors and their coverage will cost you more than a traditional bank.

How to set up a multi-currency account for your export business

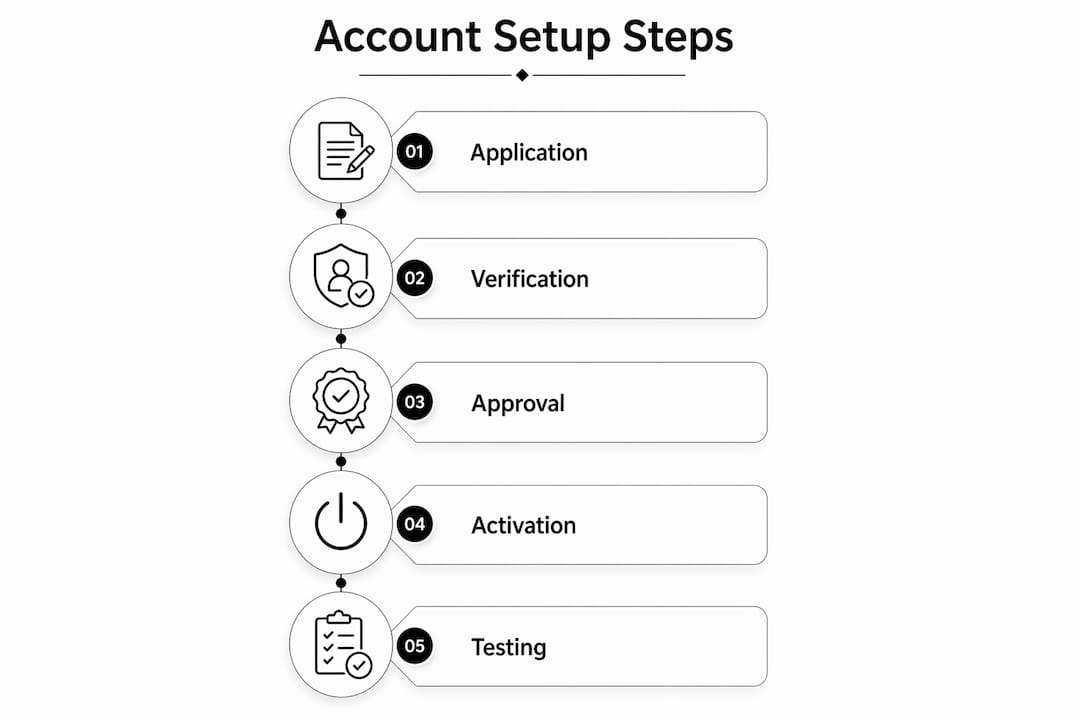

The setup process is faster than most exporters expect. Digital onboarding at platforms like TerraTrade means approvals and wallet activation happen without needing a local entity in each target country. Follow this sequence to avoid the most common delays.

- Choose your provider. Compare currency coverage, local clearing network reach, fee structures, and ERP integration options. Confirm the provider is regulated in a jurisdiction relevant to your business.

- Submit your application. Complete the digital KYB form and upload all required documents. Incomplete submissions are the single biggest cause of onboarding delays.

- Pass compliance review. The provider's compliance team verifies your business activity and ownership structure. This stage typically takes two to five business days at digital-first platforms.

- Activate your currency wallets. Once approved, activate wallets for each currency you trade in. Each wallet holds a separate balance and has its own account details for receiving payments.

- Fund your account. Transfer an initial balance from your domestic bank account. Some providers require a minimum opening deposit per wallet.

- Connect your integrations. Link your ERP or trade finance system via API. This step enables automated invoice proceeds to land in the correct wallet and triggers supplier payments automatically.

- Set FX approval workflows. Configure rules for when conversions happen and who must approve them. Embat's platform shows FX prices before approval, so your team always knows the cost before committing.

The table below shows what each stage involves and where delays most commonly occur.

| Setup stage | What happens | Common delay cause |

|---|---|---|

| Application submission | KYB form and document upload | Missing beneficial ownership docs |

| Compliance review | Identity and activity verification | Unclear business activity description |

| Wallet activation | Currency accounts created | Requesting unsupported currencies |

| Integration setup | ERP or trade finance API connection | Outdated API credentials from ERP vendor |

| Go-live | First payment received or sent | Incorrect account details shared with buyers |

Pro Tip: Send a small test payment to each new wallet before sharing account details with your buyers. Catching a configuration error on a $50 test is far better than discovering it on a $50,000 invoice.

What are the key benefits of multi-currency accounts for exporters?

The core financial benefit is natural hedging. Holding incoming payments in the original currency and paying suppliers directly in that same currency eliminates the buy-and-sell FX spread entirely. That spread is a cost most exporters pay twice on every transaction without realizing it. Removing it improves working capital without any additional financial instrument.

Speed and cost on outbound payments improve significantly when providers use local clearing networks instead of SWIFT. Routing through local networks removes intermediary banks from the chain, cutting both fees and settlement times. A payment that takes three to five days via SWIFT can settle in hours through a local clearing route.

The operational benefits are equally concrete:

- Consolidated visibility. A single dashboard shows real-time balances across all currency wallets, so your finance team always knows exactly what you hold and in which currency.

- Simplified supplier payments. Pay overseas suppliers in their local currency directly from your wallet, without converting to your domestic currency first.

- Reduced manual work. ERP integration means invoice and payment flows run automatically, cutting the manual transfers that introduce errors and delays.

- Faster receivables. Buyers pay into a local account number in their own country, which is faster and cheaper for them, making you easier to do business with.

"Seasoned treasury teams maintain traditional banks for domestic needs and multi-currency accounts for cross-border trade." — Embat

This split approach is not a workaround. It is the standard operating model for export businesses that have optimized their payment infrastructure. Your domestic bank handles payroll, local taxes, and credit facilities. Your multi-currency account handles everything that crosses a border.

For a broader view of how this applies to foreign currency accounts, the principles of currency segregation and wallet management translate directly to export operations of any size.

What mistakes should export businesses avoid with multi-currency accounts?

The most damaging mistake is treating a multi-currency account as a complete replacement for your primary bank. Multi-currency accounts work best as a complementary layer alongside domestic banking, not as a standalone solution. If your provider experiences a compliance freeze or technical outage, you need a domestic account to keep operations running.

Other common mistakes include:

- Relying on a single provider. Export businesses with high transaction volumes should maintain accounts at two providers. If one has a compliance review that freezes your account, the second keeps payments moving.

- Ignoring FX rate timing. Conversion rates change throughout the day. Scheduling large conversions without checking the rate first can cost more than the fee savings you gained by using a multi-currency account.

- Activating wallets you do not use. Dormant wallets at some providers attract maintenance fees. Only activate currencies you actively trade in.

- Skipping integration testing. An ERP integration that works in a test environment can fail in production if your trade finance facility uses a different data format. Test with real transactions before going live.

- Assuming all providers have equal local clearing reach. A provider that routes USD payments through local ACH networks may still use SWIFT for SGD or HKD. Verify the clearing method for each currency in your trade corridors.

Most exporters assume international payments must use SWIFT. Modern platforms use local clearing networks to cut costs and speed up settlement, but only for currencies within their network. Knowing which currencies your provider clears locally versus via SWIFT is the difference between a cost-efficient payment and an expensive one.

For exporters checking their eligibility before applying, the multi-currency account eligibility checklist covers the documentation and business criteria most providers require in 2026.

Key Takeaways

Multi-currency accounts give export businesses the most direct path to lower FX costs, faster cross-border payments, and real-time cash flow visibility across all currencies.

| Point | Details |

|---|---|

| Natural hedging saves real money | Hold incoming payments in original currencies and pay suppliers in those same currencies to eliminate double FX conversion costs. |

| Local clearing beats SWIFT | Providers routing through local networks settle payments faster and with fewer intermediary fees than traditional SWIFT transfers. |

| Complement, do not replace, your bank | Keep your domestic bank for local operations and use multi-currency accounts exclusively for cross-border trade flows. |

| Integration is the multiplier | Connecting your multi-currency account to your ERP or trade finance system automates receivables and payables, cutting manual errors. |

| Provider selection determines coverage | Match your provider's local clearing network to your actual trade corridors before committing to any platform. |

What I have learned from watching exporters get this wrong

Export businesses that struggle with multi-currency accounts almost always make the same mistake. They pick a provider based on the marketing page, activate every available wallet, and then discover six months later that their most important trade corridor still routes through SWIFT because the provider's local clearing network does not cover it.

The fix is simple but requires discipline. Before you sign up for anything, list every country you receive payments from and every country you pay suppliers in. Then ask each provider, directly, which of those corridors they clear locally and which they route through SWIFT. That single question will eliminate most of the wrong choices.

The natural hedging benefit is real, but it only works if your buyers actually pay into your multi-currency wallets. I have seen export businesses set up a perfectly configured account and then continue sending buyers their domestic bank details out of habit. The account sits idle. The FX costs continue. The setup was wasted.

Integration with trade finance is where the real efficiency gains live. When your multi-currency account connects to your trade finance facility, invoice proceeds land in the correct wallet automatically, and supplier payments trigger without manual intervention. That is not a feature. That is a fundamental change in how your finance team spends its time.

My honest recommendation: start with two or three currencies that represent your highest transaction volumes. Get those wallets working correctly, test the integration, and confirm the clearing routes. Then expand. Trying to activate everything at once is how you end up with a compliance review that freezes your account at the worst possible moment.

— Ahmed

How Sigmaplatinum supports export business payment needs

Sigmaplatinum is a B2B fintech platform built for international businesses that need efficient payment workflows without the complexity of traditional banking. The platform provides multi-currency business payment accounts through regulated partners, with compliance-focused onboarding that includes rigorous KYB checks and partner evaluations.

Export businesses, consulting firms, and import/export companies use Sigmaplatinum to manage FX workflows and cross-border payments from a single account. The no-code model means your team gets access to essential payment tools quickly, without lengthy technical implementation. For businesses exploring B2B cross-border payment setups, Sigmaplatinum offers a practical starting point with the compliance infrastructure already in place.

FAQ

What is a multi-currency account for export businesses?

A multi-currency account lets exporters hold, receive, and send multiple currencies from a single platform without opening local bank accounts in each country. Platforms like TerraTrade and Embat offer wallets for major trade currencies including USD, EUR, SGD, and HKD.

How does natural hedging work with a multi-currency account?

Natural hedging means holding incoming export payments in the original currency and using that balance to pay suppliers in the same currency, avoiding the buy-and-sell FX spread on both ends. This reduces reliance on formal hedging instruments and cuts conversion costs directly.

Do multi-currency accounts replace traditional business bank accounts?

Multi-currency accounts work as a complementary layer for cross-border trade, not as a replacement for domestic banking. Experienced treasury teams keep their primary bank for local operations and use multi-currency accounts exclusively for international payments.

How long does it take to open a multi-currency account?

Digital onboarding at platforms like TerraTrade typically takes two to five business days after all compliance documents are submitted. Delays most often come from incomplete beneficial ownership documentation or unclear descriptions of business activity.

What is the difference between SWIFT and local clearing for export payments?

SWIFT routes payments through a chain of intermediary banks, adding fees and settlement delays. Local clearing networks route payments directly within a country's domestic system, reducing both cost and settlement time to hours in many corridors.