Finding a multi-currency business account that supports efficient global payments without unexpected onboarding hurdles is more complicated than expected. Many providers impose steep setup fees, lack transparent pricing, or restrict access with intensive compliance checks that delay approval for legitimate businesses. You can match the right multi-currency business account to your company’s volume, compliance needs, and global payment requirements.

Table of Contents

Sigma Platinum

At a Glance

Application review fee is £99 and the monthly account fee is £69. These specific charges appear alongside partner tariffs that vary by service.

Sigma Platinum accepts business clients only and uses partner powered infrastructure for payments and FX. Approval requires eligibility checks, KYB, and partner review.

Core Features

Sigma Platinum runs business only onboarding with rigorous KYB checks and partner evaluations before accounts activate. The platform supports multi currency payment workflows, FX exchanges, and supplier payments in GBP, EUR, and USD while offering corporate card capabilities.

Services operate through regulated infrastructure partners rather than a direct banking license. That partner model groups payments, FX, and account functions under third party rails.

Key Differentiator

Partner powered infrastructure enables regulated, multi currency financial capabilities with a compliance first approach. That design lets Sigma Platinum deliver cross border payment and FX services without acting as a bank.

Pros

The compliance first onboarding suits companies that must document beneficial owners and business purpose. Partner rails widen the available financial services, which lets the platform combine FX, supplier payments, and corporate card access in one workflow.

The branded client experience helps agencies and consultants present a polished payment interface to customers. Support for GBP, EUR, and USD covers the main corridors most export and SaaS businesses use.

Cons

- Approval depends on strict eligibility and partner review, so acceptance is not guaranteed.

Who It's For

Legitimate international businesses that run cross border operations and need controlled payment workflows will benefit the most. Typical fits include digital agencies, consulting firms, SaaS companies, and import export businesses with international suppliers or customers. The service is not suitable for personal accounts or high risk activities.

Unique Value Proposition

Rigorous KYB checks and partner evaluations shape onboarding and reduce regulatory exposure for clients. That process shortens the time a finance team spends chasing compliance paperwork later. For companies that already run formal compliance, the onboarding front loads risk control and lets payments move under regulated partner rails.

Real World Use Case

A global SaaS company uses Sigma Platinum to collect payments from international customers, convert receipts across currencies, and pay contractors in local currency. The vendor relationship with regulated partners keeps FX and supplier payments routed through formal rails.

Pricing

Pricing varies by service and partner tariffs. The vendor lists an application review fee of £99 and a monthly account fee of £69, with other fees for account maintenance, payments, FX, and card services set by partners.

Website: https://sigmaplatinum.com

Multipass

At a Glance

Multi-currency IBAN accounts in over 70 currencies. Multipass also supplies local UK, US, and EU accounts for domestic-style transfers. The platform targets small and medium-sized enterprises that run regular cross-border payments.

Core Features

Multipass provides multi-currency IBAN accounts, local bank details in key jurisdictions, and fast currency exchange services that work alongside its online portal. The platform pairs account-level services with API integration for automated payouts and reconciliation, and assigns a dedicated personal account manager for onboarding and support. Remote onboarding and multilingual support reduce the need for local branches.

Key Differentiator

Multipass reports it offers fully regulated business accounts across multiple jurisdictions, combined with API-driven banking and a dedicated account manager. That combination aims to let finance teams automate payment workflows while keeping compliance and personal support in the same relationship.

Pros

Multipass reports it is regulated by the FCA and DFSA, which supports trust for companies moving sizable sums across borders. Its international coverage and local account options make domestic-style collections possible in multiple markets, and dedicated managers reduce back-and-forth during onboarding. Transparent, customizable pricing helps businesses match costs to volume, and the API enables batch payments and ledger integration.

Cons

- Pricing for account setup and maintenance varies and can be costly depending on volume and services.

- Premium features like priority onboarding, extra currencies, or account closing can incur additional fees.

- Support for specific offshore or BVI company structures depends on the company and requires direct inquiry.

- Limited physical branch presence means support is largely remote.

When It May Not Fit

Multipass is not suited for personal banking or individual freelancers. Services for certain offshore companies may be restricted depending on structure and activity, so those firms will need to confirm eligibility directly. Organizations that require many in-person branch visits will find the remote model limiting.

Who It's For

Small and medium-sized enterprises engaged in international commerce will benefit most from Multipass. Finance teams that need multi-currency accounts, API automation, and a named account manager will find the offering practical. Companies expanding into new markets without local banking infrastructure will find its local account options useful.

Real World Use Case

A UK e-commerce business uses Multipass to accept payments in several currencies, convert funds quickly, and pay suppliers abroad. The dedicated account manager set up local receiving accounts and the API automated daily payouts to supplier ledgers. That reduced manual reconciliation and shortened payment cycles.

Pricing

Pricing is bespoke and tied to business size and needs. Initial setup starts from £500, monthly fees start from £100, and transaction fees vary by currency and payment method. Multipass customizes quotes based on expected volume and required features.

Website: https://multipass.co

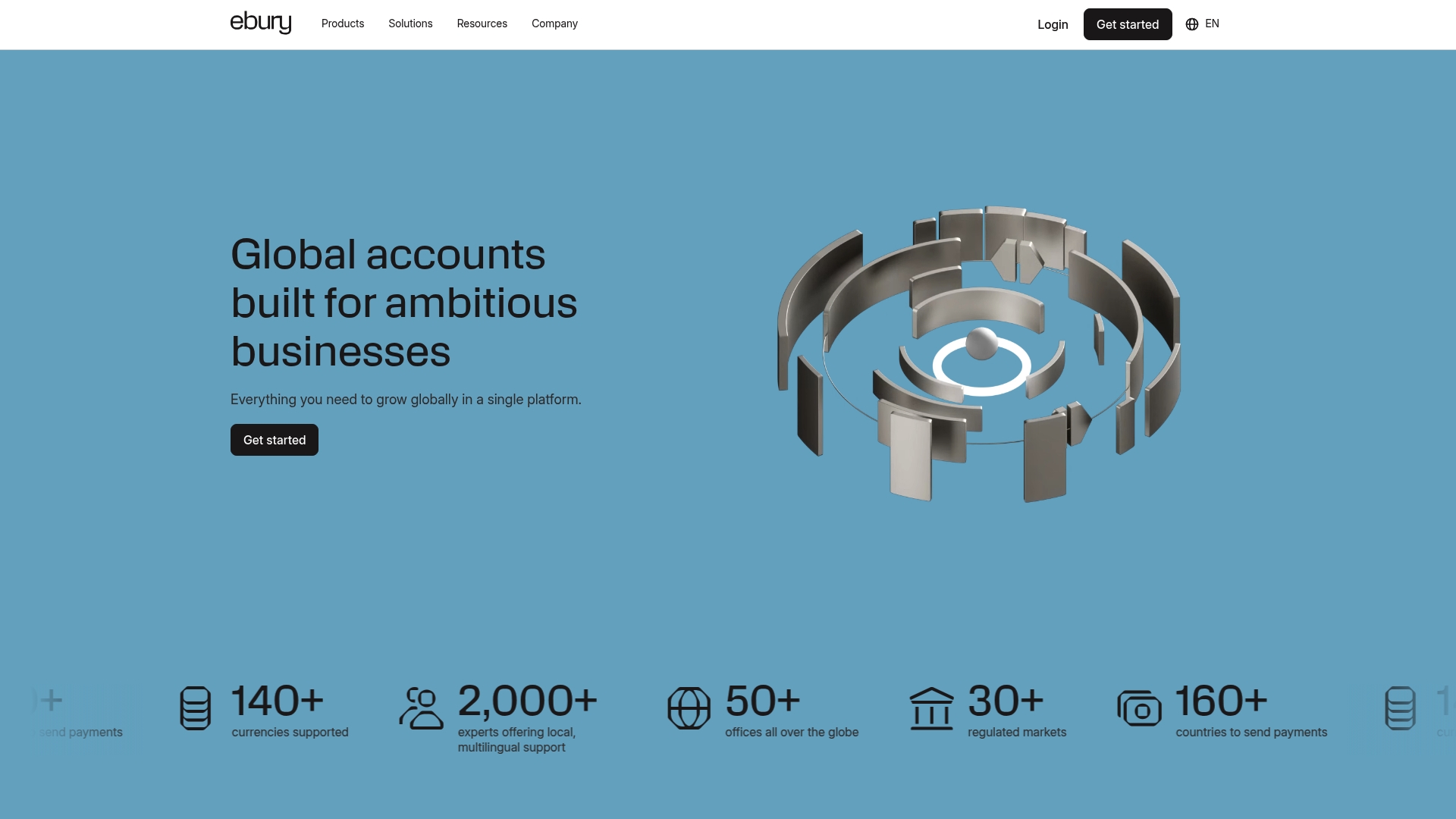

Ebury

At a Glance

Ebury reports support for over 140 currencies and local operations in more than 140 countries. The company also reports local multilingual teams across 50+ offices worldwide. That level of geographic reach positions the platform for companies moving funds and receipts across many jurisdictions.

Core Features

Ebury combines global accounts, international payments, and FX hedging tools into a single platform, and it offers financing and API access for automation. The platform includes spot, forward, options, and non-deliverable forwards for currency risk management. Ebury's marketing materials state credit lines up to 5 million GBP, and APIs cover payments, reconciliation, and cash management workflows.

Key Differentiator

Ebury unites accounts, hedging, payments, and financing under one interface while pairing those capabilities with local teams and enterprise-grade security. That blended model targets firms that need both product depth and in-market support rather than an off-the-shelf payments provider.

Pros

The vendor positions Ebury as a global operator with local presence, which helps when opening local accounts and receiving payments in-market. Integrated hedging and financing reduce the need to stitch multiple vendors together. Strong encryption and regulatory controls support work with regulated counterparties, and flexible APIs make it possible to automate payment and reconciliation workflows for accounting systems and treasury desks.

Cons

- Integration setup can be complex for smaller teams, increasing implementation time and cost.

- Pricing is not transparently published and typically requires direct consultation.

- The platform's broad feature set may overwhelm businesses without dedicated treasury or finance staff.

When It May Not Fit

Small startups with minimal cross-border volume may find the product's setup and operational scope heavier than their needs. Regional pricing and regulatory differences mean some services may not be available uniformly in every market. Companies that need simple single-country accounts rather than multi-currency and hedging tools should look elsewhere.

Who It's For

Mid-sized to large businesses expanding internationally and managing multi-currency cash flows will get the most value. The platform suits exporters, importers, and marketplaces that need local receiving accounts, FX risk controls, and financing. Teams planning to integrate payments and reconciliation via APIs will benefit from Ebury's automation capabilities.

Real World Use Case

A multinational retailer uses Ebury to open local accounts in several target markets, route customer receipts locally, and hedge exposure ahead of seasonal buying windows. The retailer pairs those flows with short-term financing when inventory purchases spike, keeping working capital available during expansion.

Pricing

Pricing is not publicly listed and may vary by country and regulatory environment. Vendors typically require a direct conversation to scope fees for accounts, hedging, payment volumes, and financing. Prospective customers should request a tailored quote during vendor engagement.

Website: https://ebury.com

Mercury

At a Glance

Mercury reports support for more than 40+ currencies across personal and business e-accounts. The platform emphasizes fast online onboarding with document upload, and it offers international transfers via SWIFT, SEPA, and Faster Payments. That combination makes opening an account and moving money across borders quick for small teams.

Core Features

Mercury offers rapid online account opening for both personal and business accounts, including an application flow that accepts document uploads for approval. It supports multi-currency holdings and payments and routes cross-border transfers through SWIFT, SEPA, and Faster Payments. Business accounts remain accessible around the clock, and the interface focuses on payments and currency management rather than broader finance tooling.

Key Differentiator

Mercury’s standout feature is its fast online onboarding combined with multi-currency account management from a single interface. That focus lets small businesses get live with cross-border payments quickly while keeping currency conversion and holdings in one place.

Pros

Fast online setup makes account opening practical for founders who need to move quickly, and the document upload flow reduces back-and-forth. Multi-currency support and direct rails for SWIFT, SEPA, and Faster Payments let you send and receive funds using familiar international channels. The digital platform is user-friendly, and customers report competitive currency exchange rates and access to local expert support for international transactions.

Cons

-

Limited product detail: specific banking features beyond account and payments are not clearly documented.

-

No visible APIs or automation: the offering lacks explicit mentions of integrations or developer tools.

-

Mixed support signals: some reviews mention potential delays with customer support.

When It May Not Fit

If you need built-in accounting, invoice automation, or a documented API, Mercury may fall short. Companies that require treasury features, programmable payouts, or deep integrations with accounting systems should plan to pair Mercury with other tools. Enterprises needing a full payments stack with automation will likely need a different vendor.

Who It's For

Small business owners, startups, and entrepreneurs who handle cross-border invoices and need a single place to hold multiple currencies will find Mercury suitable. Freelancers and remote workers receiving payments in several currencies can also benefit from the quick account setup and familiar transfer rails. Businesses expanding into Europe or the UK will value the SEPA and Faster Payments support.

Real World Use Case

A UK startup opens a Mercury business account to accept client payments in euros, pounds, and US dollars. The team uploads verification documents online, then uses SEPA for euro receipts and SWIFT for outside-Europe clients. Mercury handles currency conversion and keeps balances in separate currencies for payments.

Pricing

Not applicable. Mercury’s product listing here is informational only, and no public pricing tiers are provided in the product data. Prospective customers should consult Mercury directly for account fees and exchange margins.

Website: https://mercury.global

Convera

At a Glance

Convera reports a global network covering over 200 countries and 140 currencies. That reach supports multi-currency balances and cross-border payments for businesses that move money across many corridors. The company also advertises advanced FX hedging tools aimed at reducing exchange rate exposure.

Core Features

Convera combines a global payments network with multi-currency hold and management capabilities, real-time payment tracking, and payment automation workflows. The vendor advertises foreign exchange risk management via forward contracts, FX options, and swaps, and it lists security certifications including ISO 27001 and PCI DSS. Those features target treasury teams that need payment rails plus hedging without stitching multiple vendors together.

Key Differentiator

Convera bundles end-to-end cross-border payments infrastructure with direct hedging tools and a broad network. That pairing lets finance teams both move cash and lock exchange rates in one relationship. The approach reduces the number of counterparties treasury must manage for FX and settlement.

Pros

The platform's global coverage and currency depth suit businesses with broad international payment needs. Strong security and compliance claims make it a reasonable choice for education and finance sectors that demand guarded controls. The product also adapts to different company sizes, offering features that fit smaller treasury teams as well as mid-sized and large enterprises.

Cons

- Complexity of the product suite may require expert guidance to configure the right hedging strategy.

- Hedging instruments carry market risk and require treasury staff who understand derivatives.

- Pricing is not publicly disclosed, which suggests custom or enterprise-level pricing rather than transparent self-serve plans.

When It May Not Fit

Teams without an experienced treasury person will struggle to use derivatives effectively. Smaller businesses with low FX volume may find the product suite more than they need. Firms that require straightforward, out-of-the-box pricing or simple single-currency transfers may prefer a lighter-weight provider.

Notable Integrations

- ERP systems: connects to accounting and resource planning software for payment reconciliation.

- Treasury management systems: links to corporate treasury platforms for hedging workflows.

- Accounting platforms: feeds transaction and FX data into general ledger systems.

- Payment gateways: integrates where merchant or gateway connections are required.

Who It's For

Finance teams at mid-sized and large enterprises, educational institutions, and financial organizations that need integrated FX risk tools and global payment rails. Treasury groups that want hedging and settlement in one relationship will find this approach aligned with their workflows.

Real World Use Case

A manufacturer uses Convera to hold multiple currency balances and to execute forward contracts for planned import payments. That setup stabilizes landed costs and reduces month-to-month profit volatility caused by exchange-rate moves.

Pricing

Pricing details are not publicly posted. The product appears geared to negotiated or enterprise pricing rather than fixed, self-serve tiers.

Website: https://convera.com

OFX

At a Glance

OFX reports operations across 170+ countries. The site positions the offering as a single place for business FX, payments, and expense automation. That positioning targets companies that need both cross border payment tools and corporate finance controls.

Core Features

The platform combines international payments and foreign exchange with multi-currency accounts that provide local account details. It includes corporate cards with cashback, automated spend and receipt tracking, AP and bill automation, and multi-entity account management with real time visibility. QuickBooks and Xero appear as supported integrations for accounting reconciliation.

Key Differentiator

OFX focuses on bringing FX, payments, and expense automation together with AI driven approvals and controls. That blend aims to reduce manual approvals and accelerate payables for businesses that handle many cross border transfers. Compared with Sigmaplatinum, OFX emphasizes transaction automation over compliance focused onboarding and KYB workflows.

Pros

The platform groups multiple back office tasks into one offering, which can reduce handoffs between payments, cards, and accounting. The vendor advertises highly rated customer support with 24/7 availability, which helps teams that process urgent international payments. Multi entity visibility and AP automation cut repetitive bookkeeping tasks and speed month end reconciliations.

Cons

- Certain features and integration pages are broken or missing on the public site, which creates friction when researching implementation.

- The platform may be complex for very small or solo operations since several modules assume team based finance workflows.

- Pricing is not published on the site, so you likely need direct contact to get accurate cost details.

When It May Not Fit

If you need complete public documentation and working integration guides before committing, OFX may feel incomplete because of broken or outdated pages. Small single person businesses will probably prefer simpler, fully self served options. If transparent, menu style pricing is a requirement, expect to contact sales rather than find rates online.

Who It's For

OFX fits business owners, finance managers, and expense teams at mid-sized firms that run frequent cross border transactions. You will benefit if your operation needs multi-currency accounts, corporate cards with controls, and automated payables across multiple entities. Companies that require strict onboarding support from a compliance first provider may prefer alternative vendors.

Real World Use Case

A medium-sized import export company uses OFX to centralize cross border payments and hold multiple local currency accounts. The finance team issues corporate cards for purchasing, automates bill payment across subsidiaries, and reduces manual reconciliation with QuickBooks and Xero integrations.

Website: https://ofx.com

Comparison of alternatives

For business clients requiring compliance measures paired with multi-currency transaction support, assessing the available platforms' unique offerings is. Each solution within this review offers distinctive features catering to specific needs, making the choice dependent on business-specific priorities.

Regulatory compliance and onboarding

Sigma Platinum offers rigorous KYB (Know Your Business) checks and a compliance-first onboarding process through its partner infrastructure, prioritizing regulatory adherence. Multipass counters by providing personal account managers to streamline onboarding and maintaining compliance, adding a layer of direct human interaction. For companies seeking a high assurance of compliance with direct support, Multipass offers valuable advantages over Sigma Platinum's more general partner-dependent model.

Multi-currency support and operational features

While Sigma Platinum supports fundamental multi-currency operations and FX services in major currencies (GBP, EUR, and USD), other competitors showcase variations in their offerings. Ebury's extensive support for over 140 currencies caters to multinational operations, making it ideal for globally scaled enterprises. Companies with broader currency needs may find greater flexibility with Ebury, while those focusing on specific trading corridors might prefer Sigma Platinum's curated services.

Best fit

- Businesses prioritizing compliance and partner-controlled infrastructure will benefit from Sigma Platinum's services.

- Companies requiring regulated local accounts across jurisdictions with API-driven automation features may find Multipass a suitable choice.

- Enterprises managing intricate FX risks and needing global financial services combined with in-region support should evaluate Ebury's solutions.

Our pick

For organizations that necessitate a compliance-first approach combined with regulated multi-currency financial infrastructure, Sigma Platinum presents an ideal option. However, businesses prioritizing automation integration, broader currency access, or simpler workflows may find other solutions better tailored to these needs.

For those evaluating multi-currency business accounts and payment platforms, the following comparison highlights key differentiators across leading services:

| Platform | Primary Feature | Key Differentiator | Best For | Pricing | Limitation |

|---|---|---|---|---|---|

| Sigmaplatinum | Multi-currency payment workflows | Partner-powered regulated infrastructure | SMEs with multi-currency operations | £99 setup, £69/month | Strict eligibility requirements |

| Multipass | Multi-currency IBAN accounts | Dedicated account manager with API integration | SMEs expanding internationally | Starting at £500 setup | Premium features may incur additional costs |

| Ebury | Global financial services | Accounts, payments, and FX hedging in one platform | Mid-sized to large multinational businesses | Price not published | May overwhelm smaller businesses |

| Mercury | Rapid online onboarding and SEPA/Faster Payments | Straightforward online setup and currency support | Small businesses and startups | Price not published | Lacks advanced finance and automation features |

| Convera | Global cross-border payments | End-to-end FX tools with payment infrastructure | Treasury teams at financial organizations | Price not published | Complex functionality requires experienced treasury |

| OFX | Multi-currency accounts with expense automation | AP automation and group financial visibility | Mid-sized import-export firms | Price not published | Requires outreach to obtain pricing details |

Challenges in Finding the Right Cross-Border Payment Solutions

Businesses searching for keyfx.co.uk alternatives often face hurdles like strict compliance demands and managing multi-currency transactions efficiently. Companies such as digital agencies, consulting firms, and import/export businesses want payment workflows that reduce regulatory burden while offering broad FX and supplier payment capabilities. Sigmaplatinum meets these needs with a compliance-first onboarding process, including thorough KYB checks and partner evaluations. This approach minimizes delays and helps finance teams focus on growth rather than paperwork.

Sigmaplatinum provides a no-code platform for streamlined multi-currency account management and corporate cards via regulated partners. It supports GBP, EUR, USD corridors commonly used by international businesses. Visit Sigmaplatinum to learn how it fits companies requiring secure and efficient cross-border payment workflows.

Sigmaplatinum offers businesses a tailored solution that cuts complexity and keeps compliance front and center. Consider Sigmaplatinum to handle your FX, supplier payments, and onboarding with less hassle.

FAQ

How does Sigmaplatinum's onboarding process benefit international businesses?

Sigmaplatinum's onboarding process includes rigorous KYB checks and partner evaluations, ensuring compliance for international operations. This approach helps businesses document beneficial owners and business purposes upfront, reducing future compliance paperwork. Companies can expect a more streamlined payment process as a result.

What is the difference between Sigmaplatinum and Multipass?

Multipass is regulated by the FCA and DFSA, making it a strong option for companies needing multi-currency IBAN accounts with local bank details. Sigmaplatinum, on the other hand, focuses on compliance-first onboarding and operates through partner-powered infrastructure for payments and FX services, making it a better fit for businesses requiring rigorous regulatory controls.

Does Sigmaplatinum support multiple currencies for payment workflows?

Yes, Sigmaplatinum supports multi-currency payment workflows, allowing businesses to conduct transactions in GBP, EUR, and USD. This feature is crucial for international businesses and helps simplify their financial operations across different currencies.

Can a digital agency use Sigmaplatinum for supplier payments?

Yes, a digital agency can use Sigmaplatinum for making supplier payments, thanks to its partner-powered infrastructure and capabilities for cross-border transactions. This makes it suitable for agencies managing international suppliers effectively and compliantly.

How does Sigmaplatinum's pricing compare to competitors?

Sigmaplatinum has an application review fee of £99 and a monthly account fee of £69, which are transparent and clear. While other competitors may have bespoke pricing that varies significantly, Sigmaplatinum offers a straightforward fee structure that businesses can anticipate.